I’ll never forget the moment I checked my savings account in January 2024 and saw just $347 staring back at me. I was 32 years old, working full-time, and somehow living paycheck to paycheck despite making a decent salary. Sound familiar? That wake-up call pushed me to discover smart money saving tips that completely transformed my financial life—and by December, I had saved over $10,000 without feeling deprived or miserable.

Here’s the truth: saving money isn’t about eating ramen every night or never having fun again. It’s about making strategic choices that add up to massive savings over time. Whether you’re trying to build an emergency fund, pay off debt, or finally take that dream vacation, these proven smart money saving tips will help you reach your financial goals faster than you ever thought possible.

Key Takeaways

- Audit your subscriptions immediately – Most people waste $200+ monthly on forgotten or underused subscriptions that can be eliminated today

- Automate your savings – Setting up automatic transfers ensures you save before you spend, making it psychologically easier to reach your $10K goal

- Focus on the “Big Three” – Housing, transportation, and food account for 60-70% of expenses; small optimizations here create massive savings

- Track every dollar for 30 days – Awareness is the foundation of financial change; you can’t improve what you don’t measure

- Combine multiple strategies – Implementing 5-7 smart money saving tips simultaneously accelerates your progress exponentially

Understanding Your Financial Starting Point

Before diving into specific smart money saving tips, you need to know exactly where your money goes each month. I learned this lesson the hard way when I assumed I knew my spending patterns but was completely wrong.

The 30-Day Money Audit

Spend the next month tracking every single purchase—yes, even that $3 coffee. Use a budgeting app, spreadsheet, or even a notebook. This exercise reveals shocking truths about your spending habits. When I did this, I discovered I was spending $340 monthly on food delivery alone!

What to track:

- Fixed expenses (rent, insurance, loan payments)

- Variable necessities (groceries, utilities, gas)

- Discretionary spending (entertainment, dining out, shopping)

- Forgotten expenses (subscriptions, fees, memberships)

According to a 2024 study by the Federal Reserve, Americans who track their expenses save an average of 23% more than those who don’t [1]. That awareness alone can save you $2,300 annually on a $50,000 income.

Calculate Your Savings Potential

Once you’ve tracked expenses for 30 days, calculate your theoretical savings capacity:

Monthly Income – Essential Expenses = Savings Potential

If your savings potential is less than $833 monthly (the amount needed to save $10K in a year), don’t panic. The smart money saving tips below will help you create that capacity by reducing expenses and potentially increasing income.

For a comprehensive approach to avoiding common financial pitfalls, check out these budgeting mistakes to avoid that could be sabotaging your savings goals.

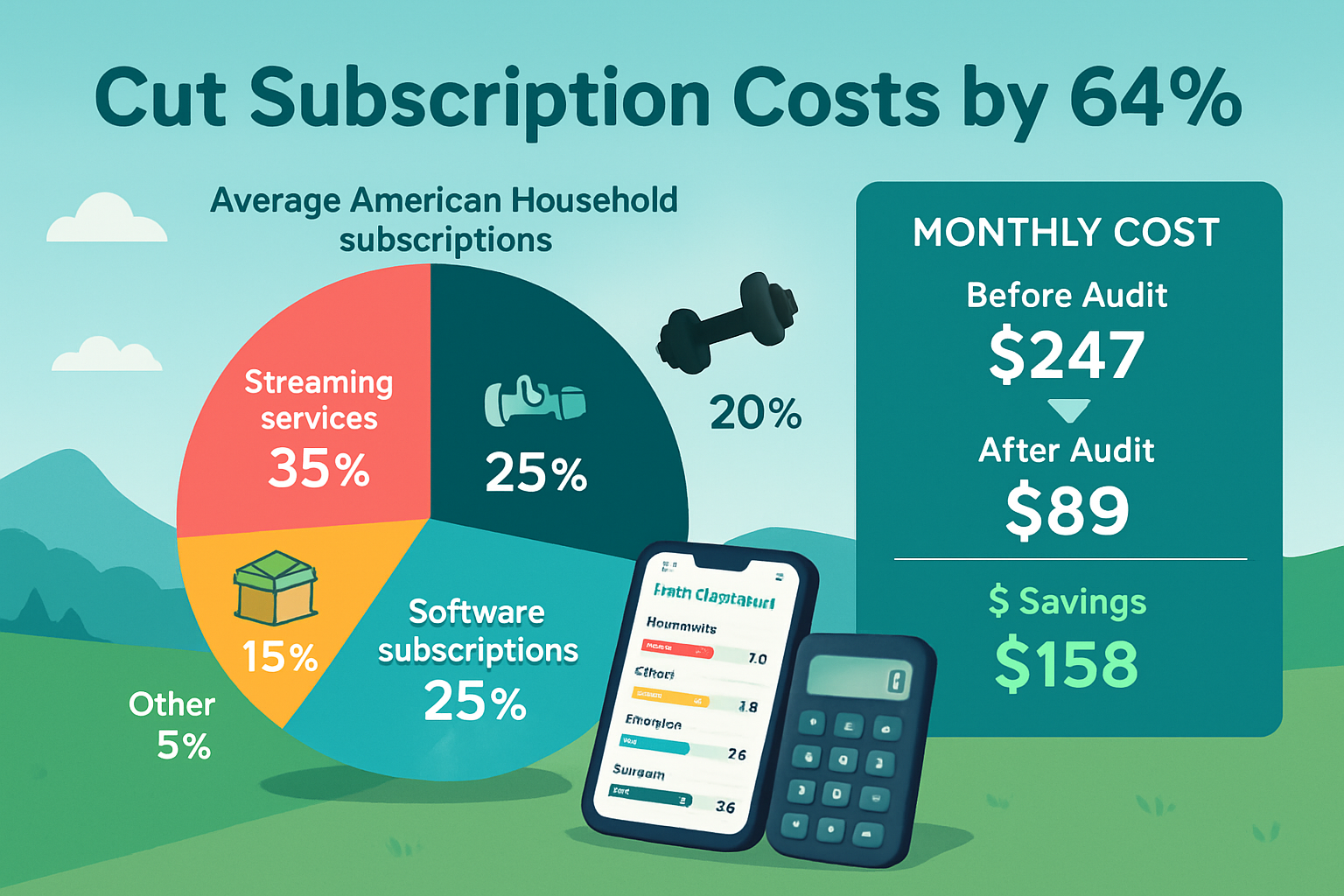

Smart Money Saving Tips for Subscription Management

Let me share something embarrassing: I was paying for three different streaming services, two gym memberships (one I forgot I even had!), and a meal kit subscription I hadn’t used in four months. That’s $247 monthly—nearly $3,000 annually—going down the drain.

The Subscription Purge Strategy

Step 1: Conduct a Complete Audit

Check your bank and credit card statements from the past three months. Highlight every recurring charge. You’ll be shocked at what you find.

Step 2: Apply the 80/20 Rule

Research shows that most people use only 20% of their subscriptions 80% of the time [2]. Cancel anything you haven’t actively used in the past 30 days.

Step 3: Negotiate or Downgrade

For subscriptions you want to keep, call customer service and ask for a discount. I saved $180 annually on my internet bill with a single 15-minute phone call. Companies would rather discount your service than lose you entirely.

Subscription Alternatives That Save Money

| Instead of This | Try This | Annual Savings |

|---|---|---|

| Cable TV ($120/month) | Streaming service rotation | $960 |

| Gym membership ($50/month) | Home workouts + outdoor running | $600 |

| Meal kit service ($80/week) | Meal planning + grocery shopping | $3,200 |

| Music streaming ($15/month) | Free tier with ads | $180 |

| Cloud storage ($10/month) | Free Google Drive/Dropbox tier | $120 |

Total potential savings: $5,060 annually

“The subscription economy is designed to make you forget you’re paying. The best defense is a quarterly audit where you review every recurring charge and justify its existence.” — Financial advisor Sarah Mitchell, CFP

Smart Money Saving Tips for Grocery Shopping

Food is typically the second-largest household expense after housing, yet it’s one of the easiest areas to optimize. These smart money saving tips helped me cut my grocery bill from $680 to $340 monthly—a savings of $4,080 per year.

Meal Planning: Your Secret Weapon

I used to walk into the grocery store without a plan and walk out $150 poorer with random ingredients that didn’t make complete meals. Sound familiar?

The Sunday Planning Ritual:

- Check what you already have – Inventory your pantry, fridge, and freezer

- Plan 5-7 dinners – Breakfast and lunch can be simpler/repetitive

- Create a detailed list – Organized by store section

- Set a budget – Aim for $50-75 per person weekly

- Stick to the list – No impulse purchases

Strategic Shopping Tactics

Buy Generic Brands

Consumer Reports found that store brands are typically 25-30% cheaper than name brands with virtually identical quality [3]. Switching to generic products saved me $78 monthly.

Shop the Perimeter

The outer edges of grocery stores contain whole foods (produce, meat, dairy) while processed, expensive items live in the center aisles. Fill your cart from the perimeter first.

Use Cash-Back Apps

Apps like Ibotta, Fetch Rewards, and Rakuten give you money back on purchases you’re already making. I earn $30-50 monthly with minimal effort.

Buy in Bulk (Strategically)

Only bulk-buy non-perishables you’ll actually use. A $40 Costco membership pays for itself if you save just $3.50 monthly.

The Grocery Savings Challenge

Try this for one month: Cut your grocery budget by 25% using these strategies. If you normally spend $600 monthly, aim for $450. Track the difference and immediately transfer that $150 to savings. Over a year, that’s $1,800 saved.

If you want to supercharge your savings, consider trying a 30-day saving challenge that gamifies the entire process and makes it fun.

Smart Money Saving Tips for Reducing Energy Costs

Energy bills are the silent budget killer—they arrive monthly, you pay them, and you rarely question whether you could pay less. These smart money saving tips can reduce your energy costs by 30-40% without sacrificing comfort.

Low-Cost, High-Impact Changes

1. LED Bulb Conversion

Replacing 20 traditional bulbs with LEDs costs about $40 but saves $225 annually [4]. The payback period is just two months.

2. Programmable Thermostat

A smart thermostat like Nest or Ecobee costs $130-250 but saves an average of $180 annually by optimizing heating and cooling schedules. I set mine to reduce heating/cooling when I’m at work or sleeping.

3. Seal Air Leaks

Weatherstripping and caulking cost under $30 but can reduce heating and cooling costs by 15% [5]. Focus on windows, doors, and where pipes enter your home.

4. Unplug Vampire Electronics

Devices on standby mode consume electricity 24/7. I use smart power strips that completely cut power to electronics when not in use, saving $100 annually.

Behavioral Changes That Cost Nothing

- Adjust your thermostat by 3-5 degrees – You’ll barely notice, but you’ll save 10% on heating/cooling

- Wash clothes in cold water – Saves $60 annually and clothes last longer

- Air dry dishes – Skip the heated dry cycle on your dishwasher

- Take shorter showers – Reducing shower time by 2 minutes saves $70 yearly on water heating

- Use ceiling fans strategically – Counterclockwise in summer, clockwise in winter

Energy Audit Checklist

✅ Replace incandescent bulbs with LEDs

✅ Install programmable thermostat

✅ Seal windows and doors

✅ Add insulation to attic

✅ Clean HVAC filters monthly

✅ Upgrade to Energy Star appliances (when replacing)

✅ Use power strips for electronics

✅ Lower water heater temperature to 120°F

Combined annual savings potential: $600-900

Smart Money Saving Tips for Transportation

Transportation is typically the third-largest expense category, averaging $10,961 annually per household [6]. Whether you own a car or use public transit, these smart money saving tips can dramatically reduce this burden.

Car Ownership Optimization

Refinance Your Auto Loan

If your credit score has improved since you bought your car, refinancing could lower your interest rate. I refinanced my car loan and saved $43 monthly—$516 annually.

Shop for Better Insurance

Insurance companies count on customer inertia. Get quotes from at least three competitors annually. I switched providers and saved $640 yearly for identical coverage.

Maintain Your Vehicle Properly

Regular maintenance prevents expensive repairs. Oil changes, tire rotations, and air filter replacements extend your car’s life and improve fuel efficiency by up to 25% [7].

Hypermiling Techniques

- Accelerate gradually

- Maintain steady speeds

- Remove unnecessary weight

- Keep tires properly inflated

- Combine errands into single trips

These habits improved my fuel efficiency from 24 to 29 MPG, saving $420 annually.

Alternative Transportation Strategies

The One-Car Family

If you have multiple vehicles, calculate whether you could manage with one. The average car costs $9,282 annually to own and operate [8]. Eliminating one car is a game-changer.

Bike or Walk for Short Trips

Trips under 2 miles are perfect for biking or walking. This improves your health while saving money on gas and vehicle wear.

Carpool or Rideshare

Splitting commute costs with a coworker can cut your transportation expenses in half. Apps like Waze Carpool connect commuters heading the same direction.

Public Transportation

If available in your area, public transit is dramatically cheaper than car ownership. A monthly pass typically costs $50-150 versus $773 monthly for car ownership [9].

Transportation Savings Comparison

| Scenario | Monthly Cost | Annual Cost | Savings vs. Baseline |

|---|---|---|---|

| Two-car household | $1,546 | $18,552 | Baseline |

| One-car household | $773 | $9,276 | $9,276 |

| Car + bike/transit | $500 | $6,000 | $12,552 |

| Public transit only | $100 | $1,200 | $17,352 |

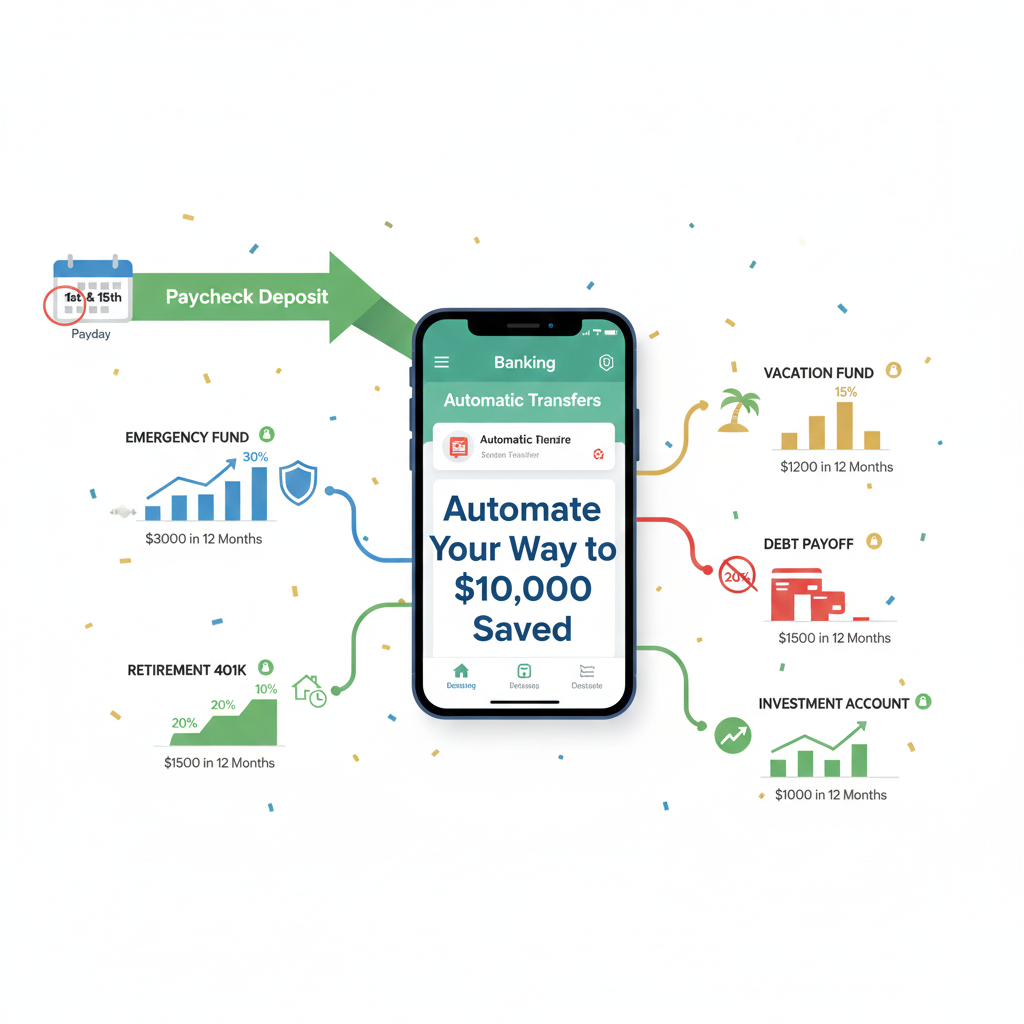

Smart Money Saving Tips for Automated Savings

Here’s the psychological truth about saving money: willpower is unreliable. You can’t depend on having money “left over” at the end of the month to save. The most effective smart money saving tips leverage automation to remove human error from the equation.

Pay Yourself First Philosophy

This concept revolutionized my finances. Instead of saving what’s left after spending, I automatically transfer money to savings the moment my paycheck arrives. My brain never registers that money as “available to spend.”

How to implement:

- Calculate your savings goal – $10,000 ÷ 12 months = $833 monthly

- Set up automatic transfers – Schedule for the day after payday

- Make it inconvenient to access – Use a separate bank with no debit card

- Increase incrementally – Start with what feels comfortable, then increase by 5% every two months

The Multiple Savings Buckets Strategy

Don’t dump all savings into one account. Create separate buckets for different goals:

- 💰 Emergency Fund – 3-6 months of expenses (highest priority)

- 🏖️ Vacation Fund – Guilt-free fun money

- 🏠 Down Payment Fund – Major purchases or home buying

- 🎓 Education Fund – Professional development or children’s education

- 🚗 Car Replacement Fund – Avoid auto loans in the future

I use a high-yield savings account that lets me create sub-accounts for each goal. Seeing progress in each category is incredibly motivating.

Micro-Saving Techniques

Round-Up Apps

Apps like Acorns and Digit round up purchases to the nearest dollar and save the difference. A $3.47 coffee becomes $4.00, with $0.53 going to savings. This painless method saved me an extra $680 last year.

The 52-Week Challenge

Save $1 in week one, $2 in week two, continuing until you save $52 in week 52. Total saved: $1,378. Reverse it (start with $52) if you want to build momentum early.

Savings Windfalls

Automatically save 50% of unexpected money (tax refunds, bonuses, gifts, rebates). This accelerates your progress without impacting your regular budget.

For more creative approaches to building your savings quickly, explore these genius savings strategy hacks that delivered real results.

Distinguishing Needs vs. Wants: The Foundation of Smart Spending

This distinction seems obvious until you actually examine your spending. I thought I “needed” my daily Starbucks latte until I realized I was spending $1,825 annually on coffee. That’s not a need—it’s a very expensive habit.

The 72-Hour Rule

Before any non-essential purchase over $50, wait 72 hours. Add the item to a wish list and revisit it in three days. You’ll be amazed how often the urge passes. This simple rule prevented $2,400 in impulse purchases for me last year.

The Cost-Per-Use Calculation

Evaluate purchases based on cost-per-use rather than sticker price.

Example:

- $200 quality boots worn 200 times = $1 per use ✅

- $50 cheap boots worn 20 times before falling apart = $2.50 per use ❌

This framework helps you invest in quality items that provide better long-term value.

The Happiness Return on Investment

Ask yourself: “Will this purchase significantly improve my life in 30 days?” Most impulse buys provide a dopamine hit that lasts hours, not weeks.

Research from Cornell University shows that experiential purchases (concerts, travel, classes) provide more lasting happiness than material goods [10]. When you do spend, prioritize experiences over stuff.

Needs vs. Wants Decision Tree

Is this purchase necessary for:

├─ Health and safety? → NEED

├─ Maintaining employment? → NEED

├─ Legal obligations? → NEED

├─ Basic shelter and food? → NEED

└─ None of the above? → WANT

└─ Can I afford this after saving 20% of income?

├─ Yes → Proceed cautiously

└─ No → Delay or eliminate

Advanced Smart Money Saving Tips: Going Beyond the Basics

Once you’ve mastered the fundamentals, these advanced strategies can accelerate your journey to $10,000 saved.

Optimize Your Tax Strategy

Most people overpay taxes through ignorance. Working with a tax professional or using quality tax software can uncover deductions and credits worth hundreds or thousands.

Tax-advantaged accounts to maximize:

- 401(k) contributions (reduces taxable income)

- HSA contributions (triple tax advantage)

- Traditional IRA (tax deduction now)

- 529 plans for education (state tax benefits)

Contributing $500 monthly to a 401(k) saves approximately $1,500 annually in taxes at a 25% tax bracket [11].

Negotiate Everything

Americans leave billions on the table annually by not negotiating. Companies expect negotiation and build wiggle room into their pricing.

What I’ve successfully negotiated:

- Medical bills (30% reduction)

- Credit card interest rates (from 18.9% to 12.9%)

- Cell phone plan (saved $35 monthly)

- Apartment rent (saved $50 monthly)

- Furniture purchases (15-20% off)

The worst they can say is no, and you’re no worse off than before asking.

The Debt Avalanche Method

If you’re carrying debt, every dollar of interest is a dollar you can’t save. The debt avalanche method prioritizes paying off highest-interest debt first, saving you the most money long-term.

Implementation:

- Make minimum payments on all debts

- Put every extra dollar toward the highest-interest debt

- Once that’s paid off, attack the next highest

- Repeat until debt-free

I used this method to eliminate $8,400 in credit card debt in 14 months. The psychological win was incredible, and the money I’d been paying toward debt immediately became savings.

For a comprehensive roadmap to becoming debt-free, check out this step-by-step plan anyone can follow.

Increase Your Income

Saving is only half the equation. Increasing income accelerates everything. You don’t need a new career—side hustles can generate substantial extra income.

Side hustle ideas that worked for me and friends:

- Freelance writing ($300-800 monthly)

- Online tutoring ($200-500 monthly)

- Selling items on Facebook Marketplace ($150-400 monthly)

- Dog walking/pet sitting ($200-600 monthly)

- Virtual assistant work ($400-1,000 monthly)

Even an extra $300 monthly is $3,600 annually toward your $10K goal. For more inspiration, explore these realistic ideas for making money from home.

The Psychology of Saving: Overcoming Mental Barriers

The technical aspects of saving money are straightforward. The psychological aspects are where most people struggle. Understanding your money mindset is crucial for long-term success.

Identify Your Money Scripts

We all have unconscious beliefs about money formed in childhood. Common limiting money scripts include:

- “I’ll never be good with money”

- “Rich people are greedy”

- “I deserve to treat myself”

- “Money doesn’t buy happiness, so why save?”

These scripts sabotage your financial goals. I believed “budgeting means deprivation” until I reframed it as “budgeting means freedom to spend on what truly matters.”

The Scarcity vs. Abundance Mindset

Scarcity thinking: “I can’t afford to save” or “I’ll never have enough”

Abundance thinking: “I’m building wealth gradually” or “I have enough to share and save”

Shifting to abundance thinking doesn’t mean ignoring financial reality—it means focusing on possibilities rather than limitations. This mental shift made saving feel empowering rather than restrictive.

Gamify Your Savings

Turn saving money into a game with rewards and milestones:

- 🎯 $1,000 saved: Celebrate with a nice (budgeted) dinner

- 🎯 $2,500 saved: Buy that book or small item you’ve wanted

- 🎯 $5,000 saved: Plan a weekend getaway (using your vacation fund)

- 🎯 $10,000 saved: Major celebration of your achievement!

Visual progress trackers—whether a thermometer on your fridge or an app on your phone—provide motivation when discipline wanes.

The Social Aspect of Money

Your peer group dramatically influences your spending habits. If your friends constantly suggest expensive restaurants and activities, you’ll face pressure to overspend.

Strategies to navigate social spending:

- Suggest free or low-cost alternatives (hiking, potlucks, game nights)

- Be honest about your financial goals—real friends will support you

- Find community with others pursuing financial wellness

- Remember that social media creates an illusion of others’ financial situations

Technology-Enabled Smart Money Saving Tips

In 2025, technology makes saving money easier than ever. These tools automate the hard parts and provide insights you’d never discover manually.

Essential Money Management Apps

Budgeting Apps:

- YNAB (You Need A Budget) – Zero-based budgeting that gives every dollar a job

- Mint – Free comprehensive expense tracking and budgeting

- PocketGuard – Shows how much you can safely spend after bills and savings

Savings Apps:

- Digit – AI-powered automatic savings based on your spending patterns

- Qapital – Rule-based savings (save when you shop, exercise, etc.)

- Chime – Automatic round-ups and early direct deposit access

Investment Apps:

- Acorns – Micro-investing with spare change

- Robinhood – Commission-free stock trading

- Betterment – Automated investment management

Price Comparison and Cash-Back Tools

Never pay full price again with these browser extensions and apps:

- Honey – Automatically applies coupon codes at checkout

- Rakuten – Cash back on purchases from 2,500+ stores

- CamelCamelCamel – Amazon price history and drop alerts

- Flipp – Digital weekly ads and coupons from local stores

I’ve earned over $340 in cash back this year just by clicking through these apps before purchases I was already making.

Bill Negotiation Services

Services like Trim, Truebill, and Billshark analyze your spending and automatically negotiate lower rates on your behalf. They take a percentage of savings, so you only pay if they succeed.

I used Trim to negotiate my cable bill, saving $23 monthly ($276 annually) with zero effort on my part.

Creating Your Personalized $10K Savings Roadmap

Generic advice only goes so far. Here’s how to create a customized plan based on your unique situation.

Step 1: Assess Your Current Reality

Calculate your numbers:

- Monthly income (after taxes): $_______

- Essential expenses: $_______

- Current savings rate: $_______

- Debt payments: $_______

- Discretionary spending: $_______

Step 2: Identify Your Top 5 Savings Opportunities

Review all the smart money saving tips in this article and select the five that offer the biggest impact for your situation.

My top 5 were:

- Subscription audit (saved $158 monthly)

- Meal planning and grocery optimization (saved $340 monthly)

- Refinancing car loan (saved $43 monthly)

- Energy efficiency improvements (saved $65 monthly)

- Automated savings transfers (ensured consistency)

Total monthly savings: $606 = $7,272 annually

Step 3: Create Your Monthly Savings Target

To save $10,000 in one year, you need to save $833 monthly. Break this into categories:

- Expense reduction: $500

- Income increase: $200

- Automated savings: $133 (from existing income)

Step 4: Implement One Change Per Week

Trying to overhaul your entire financial life overnight leads to burnout. Instead, implement one new strategy each week:

Week 1: Set up automatic savings transfers

Week 2: Conduct subscription audit

Week 3: Implement meal planning

Week 4: Switch to LED bulbs and adjust thermostat

Week 5: Shop for better insurance rates

Week 6: Download cash-back apps

Week 7: Start 72-hour rule for purchases

Week 8: Negotiate one bill

By week 8, you’ll have eight new money-saving habits working simultaneously.

Step 5: Track and Adjust Monthly

Schedule a monthly “money date” with yourself (or your partner) to review progress:

- How much did you save this month?

- Which strategies worked best?

- Where did you struggle?

- What adjustments are needed?

This regular review keeps you accountable and allows course correction before small issues become major problems.

For a structured approach to tracking your finances, consider implementing the 50/30/20 budget rule that many find sustainable long-term.

Common Mistakes to Avoid When Implementing Smart Money Saving Tips

I’ve made every money mistake in the book. Learn from my failures so you don’t repeat them.

Mistake #1: Being Too Restrictive Too Fast

When I first decided to save aggressively, I slashed my budget to the bone. No restaurants, no entertainment, no fun. I lasted three weeks before binge-spending $400 on “stuff I deserved.”

Solution: Build in reasonable discretionary spending. A sustainable 80% restriction is better than an unsustainable 100% restriction.

Mistake #2: Not Building an Emergency Fund First

I focused on saving for a vacation while ignoring my non-existent emergency fund. When my car needed a $800 repair, I had to use a credit card, negating months of savings progress.

Solution: Build a $1,000 emergency fund before pursuing other savings goals. This prevents financial emergencies from derailing your progress.

Mistake #3: Forgetting to Enjoy Life

Saving money isn’t the goal—it’s a tool to build the life you want. I became so obsessed with hitting my savings target that I declined a friend’s wedding because of the travel cost. I still regret that decision.

Solution: Budget for meaningful experiences and relationships. Some things are worth the money.

Mistake #4: Not Involving Your Partner

If you share finances, unilateral financial decisions create resentment. My partner felt blindsided when I announced we were cutting our dining-out budget by 75%.

Solution: Make financial planning a team effort. Discuss goals, strategies, and trade-offs together.

Mistake #5: Giving Up After Setbacks

I blew my budget in month three and felt like a complete failure. I almost abandoned my savings goal entirely.

Solution: Expect setbacks. One bad month doesn’t erase two good months. Analyze what went wrong, adjust, and continue forward.

For more pitfalls to watch out for, review these habits that help you stay debt-free for life.

Maintaining Momentum: Staying Motivated for 12 Months

Saving $10,000 is a marathon, not a sprint. Here’s how to maintain motivation when the initial enthusiasm fades.

Visualize Your Goal Daily

I created a vision board with images representing what $10,000 in savings meant to me: financial security, stress reduction, freedom to make choices. Seeing it daily reinforced my commitment.

Celebrate Milestones

Don’t wait until you hit $10,000 to celebrate. Acknowledge every $1,000 saved with a small, budgeted reward. Progress deserves recognition.

Find an Accountability Partner

Share your goal with someone who will check in regularly. I texted my sister monthly updates, and knowing she’d ask about my progress kept me accountable.

Join a Community

Online communities like r/personalfinance, r/frugal, or financial wellness groups provide support, ideas, and encouragement from people on similar journeys.

Track Your “Why”

When temptation strikes, reconnect with your reason for saving. Are you building security? Planning a debt-free future? Creating options? Your “why” provides motivation when willpower falters.

Measure Non-Financial Wins

Saving money creates benefits beyond your bank balance:

- Reduced financial stress and anxiety

- Improved sleep quality

- Better relationships (money stress is a top cause of conflict)

- Increased confidence and self-efficacy

- New skills in budgeting and money management

These intangible benefits often matter more than the money itself.

What Happens After You Save $10,000?

Hitting your savings goal is incredible, but it’s not the finish line—it’s the starting line for long-term financial wellness.

Building on Your Success

Once you’ve proven you can save $10,000, you’ve developed the skills and habits to continue building wealth. Consider these next steps:

1. Fully Fund Your Emergency Fund

Financial experts recommend 3-6 months of expenses. If your monthly expenses are $3,000, aim for $9,000-18,000 in emergency savings.

2. Pay Off High-Interest Debt

If you have credit card debt, student loans, or other high-interest obligations, use your newfound saving ability to aggressively pay them down.

3. Start Investing

Once you have emergency savings and manageable debt, begin investing for long-term growth. Even $200 monthly invested with a 7% average return becomes $115,000 in 20 years [12].

For beginners looking to start their investment journey, check out this guide on investing in stocks for beginners with little money.

4. Consider Passive Income Streams

Your savings can seed passive income opportunities like dividend-paying stocks, real estate crowdfunding, or online businesses. Explore smart passive income ideas that align with your interests and skills.

The Compound Effect of Good Habits

The smart money saving tips you’ve implemented aren’t just about this year’s $10,000—they’re about a lifetime of better financial decisions. Small improvements compound dramatically over time.

Example:

- Saving $833 monthly for 30 years at 7% return = $1,020,000

- That’s right—consistent saving habits can make you a millionaire

Teaching Others

Once you’ve achieved your goal, share your knowledge. Teaching others reinforces your own learning and creates accountability to maintain your new habits.

Conclusion: Your Journey to $10,000 Starts Today

Saving $10,000 in one year isn’t about deprivation or misery—it’s about making strategic choices that align your spending with your values. The smart money saving tips in this article aren’t theoretical; they’re the exact strategies I used to transform my financial life.

Your action plan for the next 24 hours:

- ✅ Track today’s spending – Start your 30-day money audit right now

- ✅ Set up automatic savings – Even if it’s just $50 to start, automate it today

- ✅ Audit your subscriptions – Review your bank statements and cancel one unused subscription

- ✅ Choose your top 5 strategies – From this article, select the five that will have the biggest impact for your situation

- ✅ Schedule your monthly money date – Put it in your calendar for the same day each month

Remember, every person who successfully saved $10,000 started exactly where you are now—at the beginning, perhaps feeling overwhelmed, maybe doubting it’s possible. The difference between them and everyone else is that they started and stayed consistent.

You don’t need to be perfect. You don’t need to implement every strategy simultaneously. You just need to start, stay consistent, and adjust as you learn what works for your unique situation.

One year from now, you could be celebrating $10,000 in savings, or you could be wishing you’d started today. The choice is yours.

What’s the first smart money-saving tip you’ll implement today? Your future self is counting on you to take that first step. Let’s make 2025 the year your financial life transforms.