I remember the first time I thought about investing in stocks for beginners with little money. I was sitting at my kitchen table, staring at a measly $73 in my savings account, thinking the stock market was some exclusive club reserved for Wall Street professionals and trust fund kids. Boy, was I wrong.

Here’s the truth that nobody tells you: You don’t need thousands of dollars to start building wealth through the stock market. In 2025, the barriers to entry have practically vanished. With just $50—less than what you’d spend on a nice dinner out—you can begin your journey toward financial independence. The democratization of investing has created unprecedented opportunities for everyday people to participate in wealth-building strategies that were once accessible only to the wealthy.

The beauty of investing in stocks for beginners with little money is that it’s not really about the amount you start with. It’s about developing the habits, understanding the fundamentals, and harnessing the power of compound growth over time. Whether you’re a college student, a young professional just starting out, or someone who’s finally ready to take control of their financial future, this guide will show you exactly how to get started—even if your budget is tight.

Key Takeaways

- You can start investing with as little as $50, thanks to fractional shares and commission-free trading platforms available in 2025

- Index funds and ETFs are the smartest choice for beginners because they provide instant diversification and minimize risk compared to individual stocks

- Dollar-cost averaging eliminates timing anxiety by investing small amounts consistently, regardless of market conditions

- The psychological benefits of starting small help you learn your risk tolerance and build confidence before committing larger sums

- Long-term thinking and patience are more important than the size of your initial investment when building sustainable wealth

Why Investing in Stocks for Beginners with Little Money Makes Perfect Sense

The Myth of Needing “Big Money” to Invest

Let’s bust the biggest myth right away: you absolutely do NOT need thousands of dollars to start investing. This outdated belief has kept countless people on the sidelines, watching their cash lose value to inflation while missing out on market growth.

Here’s what’s changed: commission-free trading is now the industry standard. Major online brokers like Robinhood, Fidelity, Charles Schwab, and E*TRADE have eliminated trading fees for stocks and ETFs[1]. This means every dollar you invest goes directly into your portfolio, not into transaction costs that used to eat up small investments.

Even better? Fractional shares have revolutionized small-budget investing. You can now buy a slice of expensive stocks like Amazon or Google for just a few dollars. If a stock costs $3,000 per share, you can invest $50 and own 1/60th of that share. Your returns are proportional to your investment, giving you access to the same growth opportunities as investors with larger portfolios.

The Power of Starting Early (Even Small)

I’ve seen firsthand how small investments can snowball into substantial wealth. The secret ingredient? Compound interest—Albert Einstein allegedly called it “the eighth wonder of the world,” and he wasn’t exaggerating.

Here’s a real-world example: If you invest just $50 per month starting at age 25, assuming an average annual return of 10% (roughly the historical S&P 500 average), you’d have approximately $316,000 by age 65. That’s turning $24,000 of your contributions into over a quarter million dollars through the magic of compounding.

Compare that to someone who waits until age 35 to start with the same $50 monthly investment. They’d end up with about $113,000—less than half the amount, despite only waiting 10 years. Time in the market beats timing the market, every single time.

Learning Your Risk Tolerance Without Breaking the Bank

Starting with small amounts provides an invaluable education that no book or course can match. When you invest real money—even just $50—you’ll experience genuine emotional responses to market fluctuations[3].

Did your stomach drop when your portfolio dipped 5% in a day? That’s important information about your risk tolerance. Did you feel excited when it jumped 3%? Also valuable data. These psychological insights are crucial for developing a sustainable investment strategy that you can stick with through market ups and downs.

Think of your first small investments as tuition for the school of real-world investing. You’re paying a small price to learn lessons that will serve you for decades. Better to discover you’re uncomfortable with volatility when you have $200 at risk than when you have $20,000 invested.

Understanding the Basics: Stock Market Investing for Beginners

What Actually Happens When You Buy a Stock?

When you purchase stock, you’re buying a tiny piece of ownership in a real company. If you buy Apple stock, you literally become a part-owner of Apple—albeit a very small one. As the company grows and becomes more profitable, your slice of ownership typically becomes more valuable.

There are two primary ways you make money from stocks:

- Capital appreciation: The stock price increases, and you sell it for more than you paid

- Dividends: Some companies share their profits with shareholders through regular cash payments

The stock market itself is simply a marketplace where buyers and sellers come together. When more people want to buy a stock than sell it, the price goes up. When more want to sell than buy, the price goes down. Supply and demand in action.

Individual Stocks vs. ETFs vs. Index Funds: What’s Best for Small Budgets?

This is where most beginners make their first critical decision, and I’m going to save you from a common mistake: don’t start by buying individual stocks.

Here’s why: Individual stocks are risky. Even experienced investors struggle to consistently pick winners. If you invest your entire $50 in one company and it tanks, you could lose most of your money. That’s concentration risk, and it’s the enemy of beginner investors[2].

Instead, focus on ETFs (Exchange-Traded Funds) and index funds. These are baskets of many different stocks bundled together. When you buy one share of an S&P 500 index ETF, you’re instantly diversified across 503 of America’s largest companies[1].

The iShares Core S&P 500 ETF (IVV) is a perfect example. With an expense ratio of just 0.03%, it costs you only $3 per year for every $10,000 invested[1]. For a $50 investment, that’s essentially free. You get exposure to Apple, Microsoft, Amazon, Google, and 499 other companies in a single purchase.

| Investment Type | Risk Level | Diversification | Best For |

|---|---|---|---|

| Individual Stocks | High | None (single company) | Experienced investors |

| Sector ETFs | Medium | Moderate (one industry) | Intermediate investors |

| Index Fund ETFs | Low-Medium | High (entire market) | Beginners ✅ |

| Bond ETFs | Low | High | Conservative portfolios |

The Rule of Diversification: Don’t Put All Your Eggs in One Basket

Diversification is your insurance policy against disaster. It’s the principle of spreading your money across different investments so that poor performance in one area doesn’t sink your entire portfolio.

Even with limited funds, you should aim for diversification across:

- Different sectors: Don’t hold 10 tech stocks together[2]. Mix technology with healthcare, consumer goods, financial services, etc.

- Geographic regions: Consider international exposure alongside U.S. stocks

- Asset classes: Eventually add bonds, real estate (through REITs), or other assets

For beginners investing in stocks with little money, the easiest path to diversification is through broad-market index funds. A single S&P 500 ETF gives you instant exposure to technology, healthcare, finance, consumer discretionary, and every other major sector of the economy.

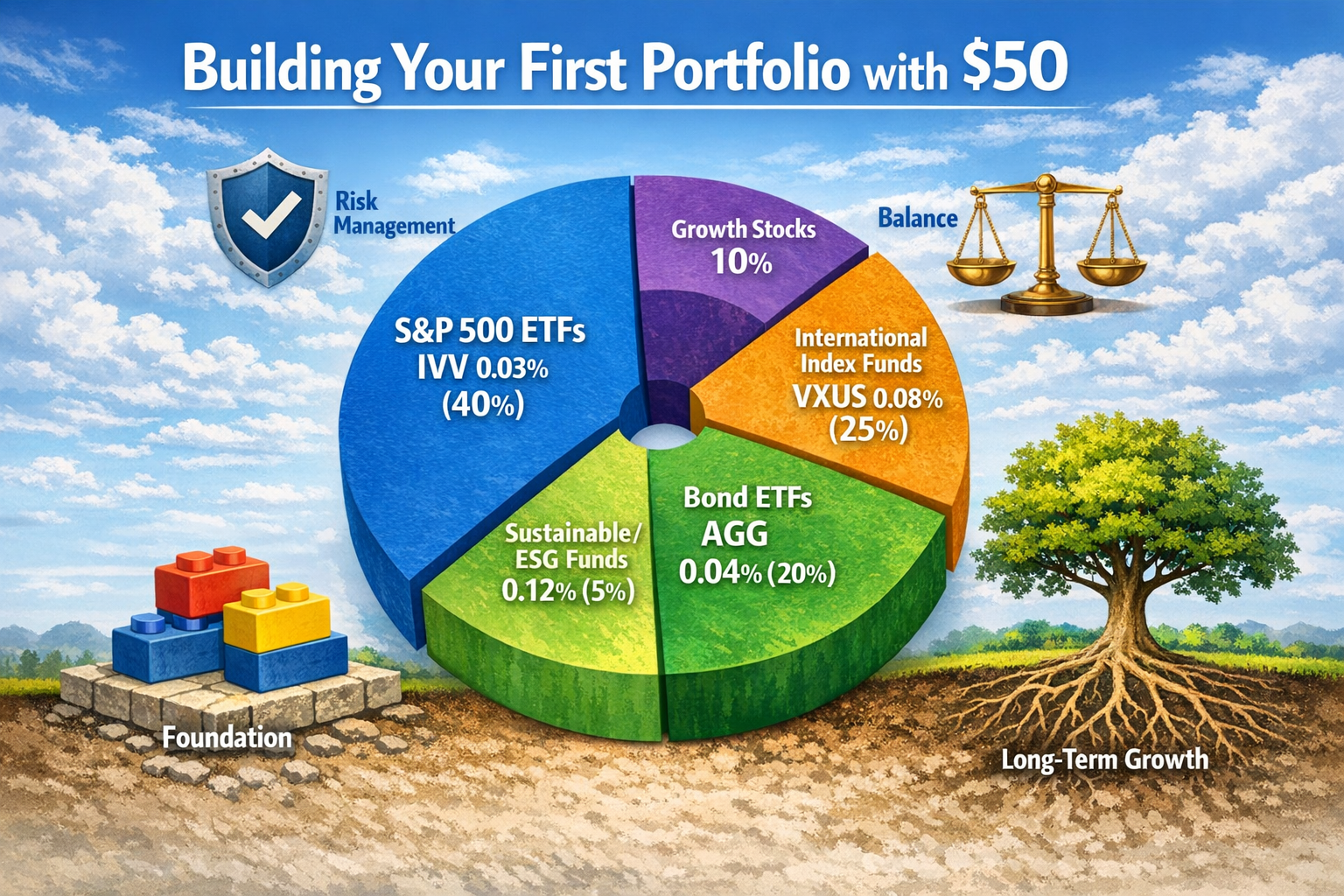

As your portfolio grows, you might add an international index fund (like VXUS) or a bond ETF (like AGG) to further diversify. But when you’re starting with $50, a simple S&P 500 index fund is perfectly adequate.

Step-by-Step Guide: How to Start Investing in Stocks for Beginners with Little Money

Step 1: Choose the Right Investment Platform

Your choice of brokerage platform can make or break your experience as a beginner investor. In 2025, you have excellent options that cater specifically to small-budget investors.

Robinhood stands out for absolute ease of use[1]. The mobile app is intuitive, visually appealing, and designed for beginners. You can start with no minimum deposit, trade commission-free, and access fractional shares. The interface makes investing feel approachable rather than intimidating.

Fidelity and Charles Schwab offer more comprehensive features while still maintaining no minimum deposits and commission-free trading. They provide excellent educational resources, research tools, and customer service. If you want a platform you can grow with as your knowledge expands, these are solid choices.

Key features to look for:

- ✅ No minimum deposit requirement

- ✅ Commission-free stock and ETF trading

- ✅ Fractional share purchasing

- ✅ User-friendly mobile app

- ✅ Educational resources for beginners

- ✅ Strong security measures

I recommend starting with Robinhood if simplicity is your priority, or Fidelity if you want more educational support and research tools. Both are excellent for investing in stocks for beginners with little money.

Step 2: Open and Fund Your Account

Opening a brokerage account takes about 10-15 minutes. You’ll need:

- Your Social Security number or Tax ID

- Government-issued ID (driver’s license or passport)

- Bank account information for funding

- Basic employment information

The process is entirely digital for most platforms. You’ll answer some questions about your investment experience and financial situation (be honest—this helps the platform provide appropriate guidance), agree to terms, and verify your identity.

Funding your account is straightforward. Link your bank account and transfer your initial investment amount. Most platforms process transfers within 1-3 business days, though some offer instant deposits for small amounts.

Pro tip: Start with whatever you can comfortably afford to invest without touching for at least 3-5 years. Even if it’s just $50, that’s a perfect beginning. You can always add more later through regular contributions.

Step 3: Select Your First Investment

This is where beginners often freeze up, paralyzed by choice. Let me make this simple: your first investment should almost certainly be an S&P 500 index ETF[1].

Here are three excellent options:

- IVV (iShares Core S&P 500 ETF) – 0.03% expense ratio

- VOO (Vanguard S&P 500 ETF) – 0.03% expense ratio

- SPY (SPDR S&P 500 ETF Trust) – 0.09% expense ratio

All three track the same index with minimal differences. IVV and VOO are slightly cheaper, but you can’t go wrong with any of them. These funds provide instant diversification across America’s 503 largest companies, representing about 80% of the entire U.S. stock market’s value.

Why S&P 500 ETFs are perfect for beginners:

- Proven long-term performance (averaging ~10% annually over decades)

- Maximum diversification for a single investment

- Extremely low costs

- No need to research individual companies

- Passive management (no constant buying and selling)

Once you’ve selected your ETF, simply search for its ticker symbol (IVV, VOO, or SPY) in your brokerage app, enter the dollar amount you want to invest (fractional shares make any amount work), and click buy. Congratulations—you’re now a stock market investor!

Step 4: Set Up Automatic Contributions (Dollar-Cost Averaging)

Here’s where the real magic happens. Dollar-cost averaging is the strategy of investing a fixed amount of money at regular intervals, regardless of market conditions[2].

Instead of trying to time the market (which even professionals fail at consistently), you invest the same amount every week, month, or paycheck. When prices are high, your fixed investment buys fewer shares. When prices are low, it buys more shares. Over time, this averages out your purchase price and removes emotion from the equation.

Most platforms allow you to set up automatic recurring investments. Here’s what I recommend:

- Decide on a comfortable amount: $25 weekly, $50 bi-weekly, $100 monthly—whatever fits your budget

- Choose a consistent schedule: Align it with your paycheck for easy budgeting

- Set it and forget it: Automation removes the temptation to skip contributions or try timing the market

I personally invest every two weeks, timed with my paycheck. I’ve set up automatic transfers from my checking account to my brokerage, then automatic purchases of my chosen ETFs. It happens without me thinking about it, which is exactly the point.

This approach has a powerful psychological benefit: it makes market downturns feel less scary. When the market drops, you’re not losing money—you’re getting stocks on sale. Your automatic investment buys more shares at lower prices, positioning you for greater gains when the market recovers.

If you’re looking to build better financial habits overall, check out these simple habits that help you stay debt-free for life, which complement your investing journey perfectly.

Smart Strategies for Low-Cost Investment Success

The Index Fund Advantage: Passive Investing That Works

Index fund investing is the tried-and-true passive investing strategy that has created more wealth for ordinary people than perhaps any other approach[2]. The concept is beautifully simple: instead of trying to beat the market, you become the market.

Warren Buffett, one of history’s greatest investors, famously bet $1 million that a simple S&P 500 index fund would outperform a collection of actively managed hedge funds over 10 years. He won easily. The index fund returned 7.1% annually while the hedge funds averaged just 2.2%[1].

Why do index funds consistently win?

- Lower costs: Expense ratios of 0.03% vs. 1-2% for actively managed funds (that difference compounds dramatically over decades)

- No manager risk: You’re not betting on someone’s stock-picking ability

- Tax efficiency: Less buying and selling means fewer taxable events

- Consistent market exposure: You capture the market’s overall growth

For beginners investing in stocks with little money, index funds eliminate the need to research individual companies, time the market, or constantly monitor your portfolio. You’re essentially outsourcing your investment strategy to the collective wisdom of the entire market.

Building Your First Portfolio: The 3-Fund Strategy

As your portfolio grows beyond your initial investment, you might consider expanding beyond a single S&P 500 fund. The 3-fund portfolio is a popular strategy among passive investors that provides global diversification with minimal complexity.

The classic 3-fund portfolio consists of:

- U.S. Stock Market Fund (60-70%): Total market or S&P 500 index

- International Stock Market Fund (20-30%): Developed and emerging markets

- Bond Market Fund (10-20%): For stability and income

Example portfolio with $500 invested:

- $350 in VTI (Total U.S. Stock Market ETF)

- $100 in VXUS (Total International Stock ETF)

- $50 in BND (Total Bond Market ETF)

This simple allocation gives you exposure to thousands of companies across the globe, plus some bonds for stability. As you add money over time, maintain these percentages by investing more in whichever fund has fallen below its target allocation.

Age-based adjustment: A common rule of thumb is to hold your age in bonds. If you’re 25, hold 25% bonds and 75% stocks. If you’re 40, hold 40% bonds and 60% stocks. This gradually reduces risk as you approach retirement.

However, when you’re just starting with $50-100, don’t overcomplicate things. A single S&P 500 index fund is perfectly fine. You can expand to the 3-fund approach once you’ve built up a few thousand dollars.

Avoiding Common Beginner Mistakes

I’ve made plenty of investing mistakes, and I’ve watched countless others make them too. Here are the most common pitfalls and how to avoid them:

❌ Trying to time the market

Waiting for the “perfect” time to invest means you’ll probably never invest. Markets hit all-time highs regularly—that’s what growth looks like. Start investing now and let time do the work.

❌ Panic selling during downturns

Market corrections of 10-20% happen regularly. If you sell when prices drop, you lock in losses and miss the recovery. Remember: you only lose money if you sell. Downturns are buying opportunities, not selling signals.

❌ Chasing hot stocks or trends

That cryptocurrency your cousin won’t stop talking about? The meme stock everyone’s buying? These are speculative gambles, not investments. Stick to your index fund strategy and ignore the noise.

❌ Neglecting to diversify

Even with small amounts, avoid putting everything into a single stock or sector[2]. Broad-market index funds solve this problem automatically.

❌ Paying high fees

Expense ratios above 0.20% are generally too high for passive index funds. Every 1% in fees can reduce your portfolio value by 25-30% over 30 years due to compound effects.

❌ Checking your portfolio too often

Daily price movements are meaningless noise. Check your portfolio quarterly at most. Constant monitoring leads to emotional decision-making and poor returns.

✅ The winning approach: Invest consistently in low-cost index funds, ignore short-term volatility, and let compound growth work its magic over decades. Boring? Yes. Effective? Absolutely.

Risk Management and Tax Considerations

Understanding Investment Risk Levels

Not all investments carry the same risk, and understanding this spectrum is crucial for beginners. Here’s how different investment types rank on the risk scale:

Low Risk:

- Government bonds (Treasury bonds, I-bonds)

- High-yield savings accounts

- Money market funds

- Short-term bond funds

Medium Risk:

- Broad-market index funds (S&P 500, total market)

- Dividend-focused ETFs

- Balanced funds (stocks + bonds)

- Real estate investment trusts (REITs)

High Risk:

- Individual stocks (especially small companies)

- Sector-specific ETFs (technology, biotech, etc.)

- Emerging market funds

- Cryptocurrency and speculative assets

For investing in stocks for beginners with little money, you should focus primarily on medium-risk investments. Broad-market index funds provide the sweet spot of reasonable growth potential without excessive volatility.

Your personal risk tolerance depends on several factors:

- Time horizon: Longer timeline = can handle more risk

- Financial stability: Emergency fund in place = can handle more risk

- Emotional temperament: Comfortable with volatility = can handle more risk

- Investment goals: Retirement in 30 years = more risk; house down payment in 3 years = less risk

A simple risk assessment: If a 20% portfolio decline would cause you to lose sleep or panic sell, you have too much risk. If a 5% decline barely registers, you might be able to handle more aggressive investments.

Tax-Efficient Investing Strategies for Beginners

Taxes can significantly impact your investment returns, but most beginners overlook this critical factor. Here’s what you need to know:

Tax-advantaged accounts should be your priority:

Roth IRA: Contributions are made with after-tax money, but all growth and withdrawals in retirement are completely tax-free. Perfect for beginners who expect to be in a higher tax bracket later. You can contribute up to $7,000 annually in 2025 (or $8,000 if you’re 50+).

Traditional IRA: Contributions may be tax-deductible now, reducing your current taxable income. You pay taxes on withdrawals in retirement. Good if you’re in a high tax bracket now and expect to be in a lower one later.

401(k) through your employer: Similar to Traditional IRA but with higher contribution limits ($23,000 in 2025). Always contribute at least enough to get your full employer match—that’s free money.

Taxable brokerage account: No tax advantages, but complete flexibility. Use this after maxing out tax-advantaged accounts, or if you’re saving for goals before retirement age.

Tax-efficiency tips:

- Hold index funds in taxable accounts (they generate fewer taxable events than actively managed funds)

- Keep dividend-heavy investments in tax-advantaged accounts

- Avoid frequent trading (short-term capital gains are taxed at higher ordinary income rates)

- Use tax-loss harvesting to offset gains with losses

- Hold investments for at least one year to qualify for lower long-term capital gains rates

For most beginners, I recommend starting with a Roth IRA if you’re eligible. The tax-free growth is incredibly powerful over decades, and you can withdraw your contributions (not earnings) anytime without penalty if you need them.

If you’re working on building your emergency fund before investing, these genius savings strategy hacks can help you save faster.

Emergency Funds First: The Foundation of Financial Security

Before we go further, I need to address something crucial: you should have an emergency fund before investing in stocks. This isn’t exciting advice, but it’s essential.

Your emergency fund should cover 3-6 months of essential expenses and be kept in a high-yield savings account (not invested in stocks). This money protects you from having to sell investments at a loss when unexpected expenses arise.

Here’s why this matters: If your car breaks down and you need $800 for repairs, having an emergency fund means you can pay for it without touching your investments. Without that cushion, you might be forced to sell stocks at the worst possible time—potentially during a market downturn—locking in losses and derailing your long-term strategy.

My recommendation: Build at least $1,000 in emergency savings before investing. Then, split additional savings between building your emergency fund to 3-6 months of expenses and starting your investment journey. For example, save $100 per month—put $50 toward emergency savings and $50 toward investments.

Once your emergency fund is fully funded, redirect all that money toward investments. This balanced approach protects you from short-term emergencies while still getting started with long-term wealth building.

Advanced Concepts for Growing Investors

The Rule #1 Investing Strategy: Beyond Index Funds

While I strongly advocate for index fund investing as your foundation, there’s a more advanced approach worth understanding as you gain experience: Rule #1 investing[3].

Developed by investor Phil Town, this strategy focuses on buying wonderful companies at attractive prices. The goal is to achieve average annual returns upwards of 15%—significantly higher than the market average[3].

The four principles of Rule #1 investing:

- Meaning: Invest in companies you understand

- Moat: The company has durable competitive advantages

- Management: Leadership is competent and shareholder-friendly

- Margin of Safety: Buy only when the price is significantly below intrinsic value

This approach requires substantial research and analysis—calculating intrinsic value, analyzing financial statements, understanding competitive dynamics. It’s not for absolute beginners, but it’s a path worth exploring once you’ve built a solid index fund foundation and want to add some individual stock positions.

When to consider individual stock investing:

- You have at least $5,000-10,000 invested in diversified index funds

- You’ve been investing consistently for at least 1-2 years

- You genuinely enjoy researching companies and reading financial reports

- You can devote several hours per month to investment research

- You understand that even great investors pick losing stocks sometimes

Even then, I recommend keeping 70-80% of your portfolio in index funds and using only 20-30% for individual stock picks. This limits your downside while giving you exposure to potentially higher returns.

Sustainable and Ethical Investing Options

More investors—especially younger ones—want their money to align with their values. ESG investing (Environmental, Social, and Governance) and sustainable investing have exploded in popularity and accessibility.

You can now easily invest in funds that:

- Exclude fossil fuel companies

- Focus on renewable energy and clean technology

- Emphasize companies with strong labor practices

- Avoid weapons manufacturers or tobacco companies

- Prioritize corporate governance and ethical leadership

Popular ESG ETFs for beginners:

- ESGU (iShares ESG Aware MSCI USA ETF) – 0.15% expense ratio

- VFTAX (Vanguard FTSE Social Index Fund) – 0.14% expense ratio

- DSI (iShares MSCI KLD 400 Social ETF) – 0.25% expense ratio

The good news: research increasingly shows that ESG investing doesn’t require sacrificing returns. Many ESG funds have matched or outperformed traditional funds in recent years, while allowing investors to support companies aligned with their values.

A word of caution: “Greenwashing” is real. Some funds market themselves as sustainable while holding questionable companies. Research the actual holdings and methodology before investing. Look for funds with clear, transparent criteria and third-party ESG ratings.

For beginners investing in stocks with little money who care about impact, starting with a broad ESG index fund provides both values alignment and diversification.

Leveraging Technology: Investment Tracking and Education Tools

The technology available to investors in 2025 is remarkable—and most of it is free. Here are tools that can enhance your investing journey:

Portfolio tracking apps:

- Personal Capital: Free comprehensive financial dashboard showing all your accounts, asset allocation, and performance

- Mint: Budgeting and investment tracking in one place

- Empower: Investment analysis with retirement planning tools

Educational resources:

- Investopedia: Comprehensive investing encyclopedia with tutorials

- The Motley Fool: Beginner-friendly articles and stock analysis

- Bogleheads Forum: Community of passive investors sharing strategies

- Khan Academy: Free courses on finance and investing fundamentals

Research platforms:

- Yahoo Finance: Free stock quotes, news, and basic financial data

- Seeking Alpha: Analysis and opinions on stocks and ETFs

- FINVIZ: Stock screening and visualization tools

Podcasts for beginners:

- The Money Guy Show: Financial planning and investing basics

- ChooseFI: Financial independence through smart investing

- BiggerPockets Money: Personal finance and wealth building

I spend about 30 minutes per week reading investing content and listening to podcasts during my commute. This consistent education has been invaluable for developing my investment philosophy and staying informed without becoming obsessive.

Pro tip: Be selective about who you listen to. Avoid anyone promising get-rich-quick schemes, guaranteed returns, or “secret” strategies. Focus on educators who emphasize long-term thinking, diversification, and evidence-based approaches.

Real-World Success Stories: Small Investments, Big Results

Case Study 1: The College Student Who Started with $100

Meet Sarah, a college junior who started investing with just $100 from her part-time job. She opened a Robinhood account, bought fractional shares of a S&P 500 ETF, and set up automatic $25 bi-weekly investments.

Sarah’s results after 2 years:

- Total contributions: $1,300

- Portfolio value: $1,547

- Return: 19% (includes market growth and consistent contributions)

What impressed me most about Sarah’s story wasn’t the returns—it was the confidence and financial literacy she developed. She learned to ignore market volatility, understood the power of consistency, and developed a long-term mindset that will serve her for decades.

“The hardest part was starting,” Sarah told me. “I kept thinking $100 wasn’t enough to matter. But once I saw my first $5 in gains, something clicked. I realized I was actually building wealth, not just saving money.”

By starting in college, Sarah gave herself a 40+ year time horizon. If she maintains her $50 monthly contribution with average market returns, she’ll have over $500,000 by retirement—all from starting with $100 and adding $50 per month.

Case Study 2: The Career-Changer Who Invested During Uncertainty

James lost his job during the 2020 pandemic and took a lower-paying position in a new field. With limited income, he could only invest $75 monthly, but he committed to consistency regardless of market conditions.

James’s strategy:

- 70% in VTI (Total Stock Market ETF)

- 20% in VXUS (International Stock ETF)

- 10% in BND (Bond ETF)

Results after 3 years:

- Total contributions: $2,700

- Portfolio value: $3,485

- Return: 29% (benefiting from market recovery and dollar-cost averaging)

James’s experience illustrates a crucial principle: starting during uncertainty or downturns can actually be advantageous. His consistent investments during market volatility meant he bought many shares at lower prices, maximizing his returns during the recovery.

“I was terrified to invest when everything felt unstable,” James shared. “But I kept reading that time in the market beats timing the market. Looking back, starting when I did—even with small amounts—was one of the best financial decisions I’ve made.”

The Compound Growth Projection: Your Potential Future

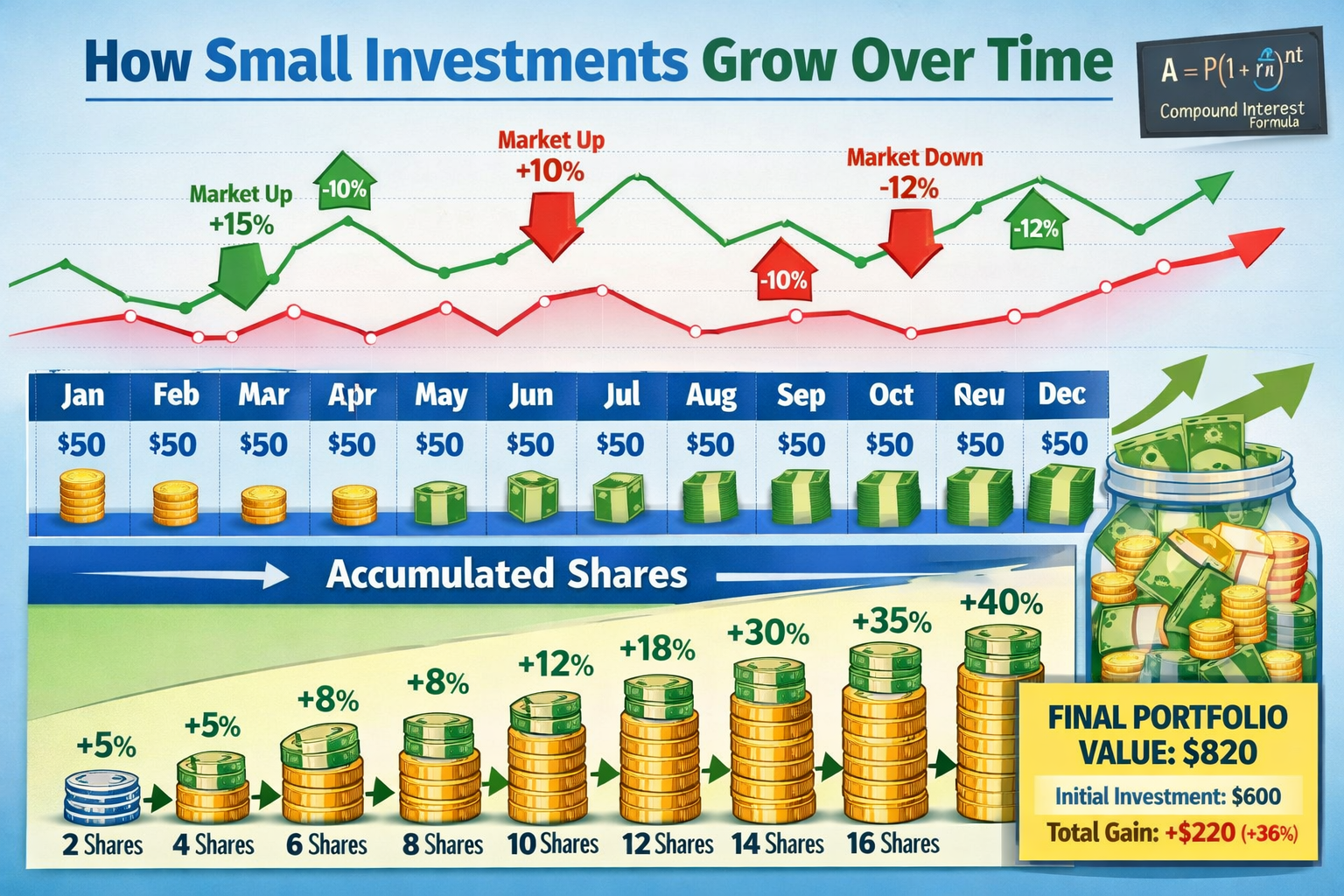

Let’s look at what consistent small investments can become over different time horizons. These projections assume a 10% average annual return (roughly the S&P 500’s historical average):

$50 monthly investment:

- 10 years: $10,246 (contributions: $6,000)

- 20 years: $37,968 (contributions: $12,000)

- 30 years: $109,545 (contributions: $18,000)

- 40 years: $316,204 (contributions: $24,000)

$100 monthly investment:

- 10 years: $20,492 (contributions: $12,000)

- 20 years: $75,937 (contributions: $24,000)

- 30 years: $219,090 (contributions: $36,000)

- 40 years: $632,408 (contributions: $48,000)

$200 monthly investment:

- 10 years: $40,984 (contributions: $24,000)

- 20 years: $151,874 (contributions: $48,000)

- 30 years: $438,180 (contributions: $72,000)

- 40 years: $1,264,816 (contributions: $96,000)

Notice that the 40-year $50/month investor turns $24,000 in contributions into over $316,000—a 13x return. The 40-year $200/month investor becomes a millionaire, contributing less than $100,000 total.

This is the power of starting early with whatever you can afford. The amount you start with matters far less than the time you give your money to grow and the consistency of your contributions.

If you’re currently working on getting out of debt before you can invest more aggressively, this step-by-step plan to become debt-free can help you accelerate that process.

Common Questions About Investing in Stocks for Beginners with Little Money

How much money do I really need to start investing in stocks?

You can start with as little as $1 thanks to fractional shares, though I recommend beginning with at least $50-100 to make the effort feel meaningful[1][3]. Most major brokers have $0 minimum deposits, and commission-free trading means every dollar goes into your investment.

The psychological barrier is often bigger than the financial one. People think they need thousands to start, but that’s simply not true in 2025. Start with whatever you have available after building a small emergency fund.

What’s the difference between stocks and ETFs?

A stock is ownership in a single company. When you buy Apple stock, you own a piece of Apple. An ETF (Exchange-Traded Fund) is a basket of many stocks bundled together. When you buy an S&P 500 ETF, you own tiny pieces of 503 different companies.

For beginners, ETFs are almost always the better choice because they provide instant diversification and reduce risk[1]. Individual stocks can be volatile and risky—even great companies can have bad years.

Is now a good time to invest, or should I wait for a market crash?

This is the most common question I hear, and the answer is always the same: the best time to start investing was yesterday; the second-best time is today.

Trying to time the market is a losing strategy. Even professional investors with teams of analysts can’t consistently predict market movements. Markets hit all-time highs regularly—that’s what growth looks like. If you wait for a crash, you might wait years while missing out on gains.

Dollar-cost averaging solves this problem. By investing consistently regardless of market conditions, you buy at high prices, low prices, and everything in between, averaging out your cost over time.

How do I know if I’m too risk-averse or too aggressive?

A simple test: Imagine your $1,000 portfolio drops to $800 tomorrow (a 20% decline). How would you feel?

- Panic, lose sleep, want to sell immediately: You’re too aggressive; add more bonds or reduce stock allocation

- Uncomfortable but able to hold steady: You’re probably appropriately allocated

- Excited to buy more at lower prices: You might be able to handle more aggressive investments

Your risk tolerance should match your time horizon. If you won’t need the money for 30+ years, you can handle more volatility because you have time to recover from downturns. If you need the money in 3-5 years, you should be more conservative.

What’s the difference between a Roth IRA and a regular brokerage account?

A Roth IRA is a tax-advantaged retirement account. You contribute after-tax money (no immediate tax deduction), but all growth and qualified withdrawals in retirement are completely tax-free. There are contribution limits ($7,000 in 2025) and income limits for eligibility.

A regular brokerage account has no contribution limits, no withdrawal restrictions, and no tax advantages. You pay capital gains taxes on profits when you sell. Use this for goals before retirement age or after maxing out tax-advantaged accounts.

For most beginners, starting with a Roth IRA makes sense if you’re eligible. The tax-free growth over decades is incredibly powerful.

Should I invest in individual stocks or just stick with index funds?

For your first few years of investing, stick with index funds and ETFs[1]. They provide diversification, reduce risk, and require minimal research or monitoring.

Once you have:

- At least $5,000-10,000 in index funds

- 1-2 years of consistent investing experience

- Genuine interest in researching companies

- Time to dedicate to investment analysis

…then you might consider adding some individual stock positions. Even then, keep 70-80% in index funds and use only 20-30% for individual stocks.

How often should I check my investment portfolio?

Quarterly at most. Checking daily or weekly leads to emotional decision-making and poor returns. Market volatility is normal noise—it doesn’t require action.

Set a calendar reminder to review your portfolio every 3 months. Check that your asset allocation is still on target, rebalance if needed, and otherwise leave it alone. This disciplined approach prevents panic selling during downturns and overconfidence during rallies.

What if I need the money before retirement?

If you’re investing in a taxable brokerage account (not an IRA or 401k), you can access your money anytime by selling investments. However, you’ll owe capital gains taxes on any profits.

For a Roth IRA, you can withdraw your contributions (not earnings) anytime without penalty. The earnings must stay until retirement age to avoid penalties and taxes.

General rule: Only invest money you won’t need for at least 3-5 years, ideally longer. This gives you time to ride out market downturns without being forced to sell at a loss.

Taking Action: Your Next Steps to Start Investing Today

You’ve absorbed a lot of information, and you might feel overwhelmed. That’s normal. The key is to take one small step at a time rather than trying to implement everything at once.

Your 7-Day Action Plan

Day 1-2: Choose your platform

Research Robinhood, Fidelity, and Charles Schwab. Read reviews, download apps, and decide which feels most comfortable. Don’t overthink this—all three are excellent for beginners.

Day 3: Open your account

Complete the application process. Have your ID, Social Security number, and bank information ready. This takes 10-15 minutes.

Day 4: Fund your account

Link your bank account and transfer your initial investment. Start with whatever you’re comfortable with—$50, $100, or more.

Day 5: Research your first investment

Look up IVV, VOO, or SPY. Read about the S&P 500 index. Understand what you’re buying.

Day 6: Make your first purchase

Buy your chosen S&P 500 ETF. Use fractional shares to invest your entire amount. Congratulations—you’re now an investor!

Day 7: Set up automatic contributions

Schedule recurring investments. Even $25 bi-weekly or $50 monthly makes a huge difference over time.

Building Your Investment Mindset

Success in investing isn’t primarily about strategy or stock selection—it’s about mindset and behavior. Here are the mental models that separate successful long-term investors from those who give up:

🧠 Think in decades, not days

Your investment horizon should be measured in years and decades. Daily or monthly fluctuations are meaningless noise. Focus on the long-term trend, which has historically been upward.

🧠 Embrace boring consistency

The most successful investors aren’t doing anything exciting. They’re buying index funds, contributing regularly, and ignoring market noise. Boring works.

🧠 View downturns as opportunities

Market crashes are sales on stocks. If your favorite store had a 20% off sale, you’d be excited. Apply the same thinking to market downturns.

🧠 Separate investing from gambling

Investing is buying ownership in productive businesses and holding long-term. Gambling is trying to predict short-term price movements or chasing hot stocks. Know the difference.

🧠 Automate to remove emotion

The best investment decisions are the ones you don’t have to make. Automation removes emotion, prevents procrastination, and ensures consistency.

🧠 Measure progress in years, not dollars

Instead of obsessing over your account balance, track your investing habits. Did you contribute consistently this year? Did you avoid panic selling? Those behaviors matter more than short-term returns.

Continuing Your Education

Investing is a lifelong learning journey. Here’s how to continue developing your knowledge:

📚 Read one investing book per quarter: Start with “The Simple Path to Wealth” by JL Collins or “The Little Book of Common Sense Investing” by John Bogle

🎧 Listen to one investing podcast weekly: Choose educational content over market predictions

📰 Follow market news casually: Stay informed without becoming obsessed

💬 Join an investing community: The Bogleheads forum is excellent for passive investors

📊 Review your strategy annually: Assess what’s working and adjust if needed (but avoid frequent changes)

🎓 Take a free online course: Khan Academy and Coursera offer excellent investing fundamentals courses

Remember: the goal isn’t to become an expert overnight. It’s to continuously improve your understanding while taking consistent action.

The Bigger Picture: Investing as Personal Empowerment

Beyond the financial returns, investing represents something deeper: taking control of your financial future. Every dollar you invest is a vote for your future self, a declaration that you’re building the life you want rather than leaving it to chance.

I’ve seen how investing transforms people’s relationship with money. It shifts the mindset from scarcity to abundance, from consumer to owner, from passive to active. You stop seeing yourself as someone who works for money and start seeing yourself as someone whose money works for them.

This empowerment extends beyond your personal finances. As a shareholder—even a small one—you’re participating in the economy’s growth. You’re funding innovation, job creation, and economic development. Your capital helps companies expand, hire employees, and develop new products.

For many people, especially those from communities historically excluded from wealth-building opportunities, investing in stocks represents economic participation that previous generations couldn’t access. The democratization of investing through commission-free trading and fractional shares has opened doors that were once firmly closed.

Investing is fundamentally optimistic. It’s a bet that the future will be better than the present, that human innovation and productivity will continue creating value. That’s a bet I’m happy to make, and I hope you are too.

Conclusion

Investing in stocks for beginners with little money isn’t just possible in 2025—it’s easier and more accessible than ever before. The barriers that once kept ordinary people out of the stock market have crumbled. Commission-free trading, fractional shares, and intuitive mobile apps have democratized wealth-building in ways that would have seemed impossible just a decade ago.

You don’t need thousands of dollars, an economics degree, or insider knowledge. You need three things: a small amount of money to start, the discipline to invest consistently, and the patience to let compound growth work its magic over time.

Start with $50 in an S&P 500 index fund. Set up automatic contributions of whatever you can afford—even $25 bi-weekly makes a difference. Ignore the daily market noise. Think in decades, not days. Stay the course through market ups and downs. That’s the entire strategy, and it works.

The most common regret I hear from investors isn’t about losses or missed opportunities—it’s about not starting sooner. Don’t let that be your regret. The perfect time to start was ten years ago. The second-best time is right now, today, with whatever amount you have available.

Your future self will thank you for taking this first step. Welcome to the investor community. You’ve got this.

Ready to take action? Open a brokerage account this week. Make your first investment. Set up automatic contributions. Then check out more personal finance strategies at MSBudget to complement your investing journey. The path to financial independence starts with a single step—and you’re already on your way.

References

[1] NerdWallet. (2025). “Best Brokers for Beginning Investors.” Retrieved from industry analysis of major brokerage platforms including Robinhood, Fidelity, and Charles Schwab commission structures and minimum deposit requirements.

[2] Investopedia. (2025). “Index Fund Investing and Diversification Strategies for Beginners.” Analysis of passive investing approaches and portfolio construction methodologies.

[3] Rule #1 Investing. (2025). “How to Start Investing with Little Money.” Phil Town’s investment philosophy and small-capital investing strategies.

[4] The Motley Fool. (2025). “Beginner’s Guide to Stock Market Investing.” Comprehensive overview of investment fundamentals and goal-setting frameworks for new investors.