Let me be honest with you: I used to think people who did “no spend challenges” were either superhuman or secretly miserable. I mean, who voluntarily stops spending money for an entire month? But after scrolling through my credit card statement one January morning in 2024 and realizing I’d spent $847 on things I couldn’t even remember buying, I knew something had to change. That’s when I discovered no spend January—and it completely transformed my relationship with money, even though I’d never successfully stuck to a budget in my life.

If you’re tired of starting each year broke, overwhelmed by holiday spending, or just ready for a financial reset, you’re in the right place. The no-spend challenge isn’t about deprivation or living like a minimalist monk (unless that’s your thing). It’s about breaking the autopilot spending habits that drain your bank account and rediscovering what truly matters to you.

Key Takeaways

- No spend January is a month-long challenge where you only spend money on predetermined essentials, helping you break impulse spending habits and reset your financial mindset

- You don’t need budgeting experience to succeed—the challenge works by creating clear boundaries and heightened awareness around your spending triggers

- Most participants save $500-$2,000 during the month while developing lasting money management skills that extend far beyond January

- The psychological benefits often outweigh the financial ones, including reduced anxiety, increased mindfulness, and a healthier relationship with consumption

- Customization is key—your no-spend challenge should reflect your life circumstances, financial goals, and personal values, not someone else’s rules

What Exactly Is the No-Spend Challenge? (And Why January?)

The no-spend challenge is exactly what it sounds like: a designated period where you commit to spending money only on absolute necessities. Think rent, utilities, groceries, medications, and transportation to work. Everything else—dining out, online shopping, entertainment subscriptions, that “treat yourself” coffee—gets put on pause.

But why January specifically? There’s actually brilliant psychology behind choosing this particular month for your financial reset.

The Perfect Storm for Financial Change

January represents a natural reset point in our brains. We’re already in “new year, new me” mode, which means our motivation is higher and our resistance to change is lower. Plus, most of us are recovering from holiday spending hangovers. According to recent consumer research, the average American spends over $1,000 during the holiday season, with many carrying that debt well into spring [1].

No spend January capitalizes on this post-holiday reality by offering:

✅ A clear starting and ending point (the entire month)

✅ Built-in accountability (millions participate annually)

✅ Immediate relief from holiday debt accumulation

✅ A fresh slate mentality that January naturally provides

✅ Longer winter days that encourage staying home (less temptation)

What Makes It Different from Traditional Budgeting?

Here’s where things get interesting for those of us who’ve failed at budgeting before. Traditional budgeting requires you to track, categorize, and limit spending across multiple categories—it’s like trying to juggle while learning to ride a bike. The no-spend challenge simplifies everything into two categories: essential and non-essential.

This binary approach removes decision fatigue. You’re not debating whether you can afford that $30 sweater within your clothing budget. You’re simply not buying clothes this month, period. For budgeting beginners, this clarity is revolutionary.

The Psychology Behind Why We Overspend (And How No-Spend Breaks the Cycle)

Before we dive into the how-to, let’s talk about why we spend money we don’t have on things we don’t need. Understanding this is crucial because no spend January works by interrupting these deeply ingrained patterns.

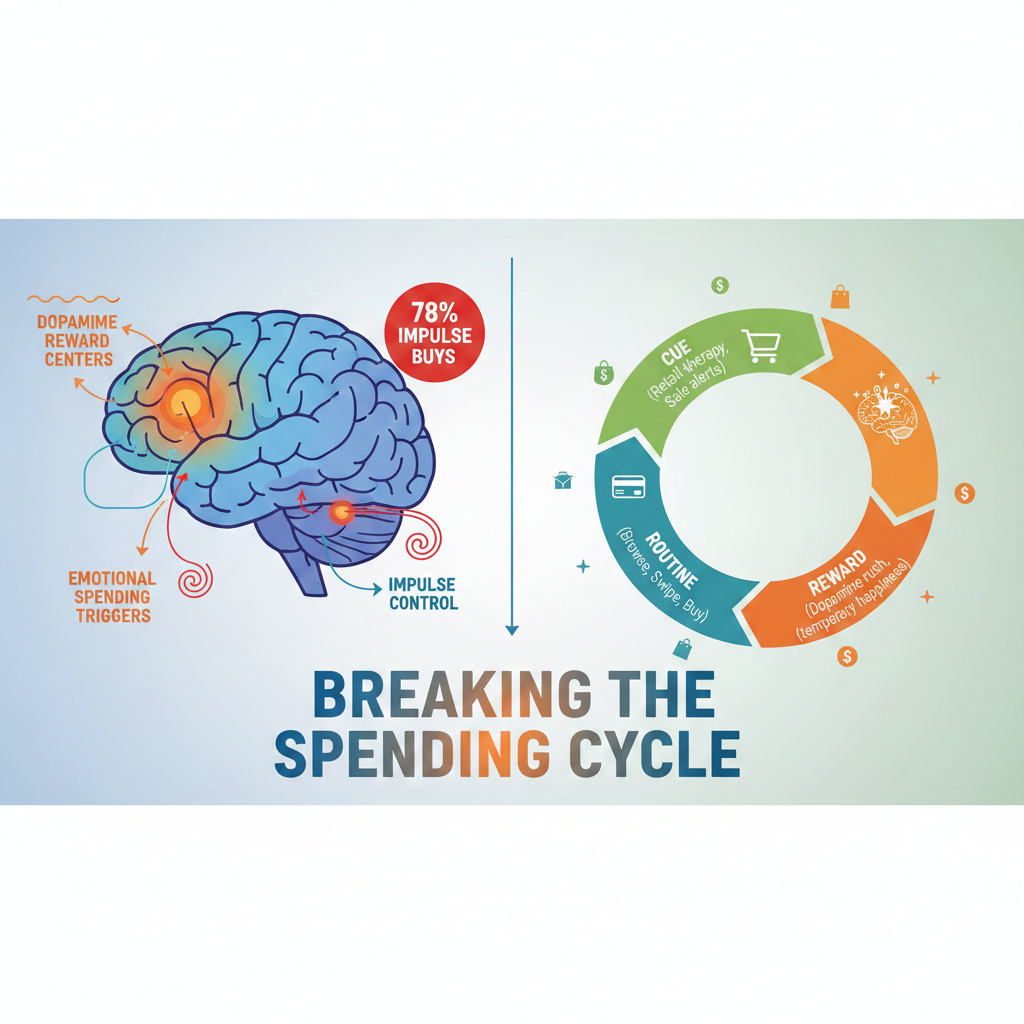

Your Brain on Shopping: The Dopamine Connection

Every time you make a purchase, your brain releases dopamine—the same neurotransmitter involved in addiction. That little rush you feel when clicking “complete purchase” or swiping your card? That’s your brain’s reward system lighting up like a Christmas tree [2].

The problem? Like any reward-based behavior, we build tolerance. That $5 coffee that used to feel special becomes routine. So we escalate—a $50 brunch, a $200 online shopping spree, a $500 weekend getaway. We’re chasing that initial dopamine hit, but it takes more and more spending to achieve it.

The no-spend challenge interrupts this cycle by forcing you to find dopamine elsewhere: completing a challenging workout, finishing a book, organizing your closet, connecting with friends. You’re literally rewiring your brain’s reward pathways.

The Four Spending Triggers Most People Don’t Recognize

Through my own no-spend journey and conversations with dozens of others who’ve completed the challenge, I’ve identified four major spending triggers that operate below our conscious awareness:

1. Emotional Regulation Spending 💔

Bad day at work? Buy something. Feeling lonely? Online shopping. Stressed about money? Ironically, spend money. We use purchases as emotional band-aids, never addressing the actual wound.

2. Identity-Based Consumption 👔

We buy things that reflect who we think we should be rather than who we are. The yoga mat for the person who’ll totally start practicing. The business books for the entrepreneur you aspire to become. These purchases are investments in fantasy versions of ourselves.

3. Social Comparison Spending 📱

Social media has turbocharged this trigger. We see curated highlights of others’ lives and spend money trying to keep up with an illusion. That influencer’s aesthetic apartment, your colleague’s vacation photos, your friend’s new car—each becomes a benchmark we unconsciously try to match.

4. Convenience Creep ⚡

What started as occasional conveniences become non-negotiable necessities. Food delivery, ride-sharing, subscription boxes, premium streaming services—we’ve normalized spending hundreds monthly on things that didn’t exist a decade ago.

The beauty of the no-spend challenge is that it forces these triggers into the light. When you can’t act on them, you have to sit with the uncomfortable feelings they mask. That’s where real transformation happens.

Setting Up Your No Spend January for Success (The Actually Doable Way)

Okay, enough theory. Let’s get practical. If you’ve never budgeted before, the idea of planning a month-long spending freeze might feel overwhelming. But I’m going to walk you through a framework that makes it manageable—even enjoyable.

Step 1: Define Your “Essential” Category (This Is Personal!)

The biggest mistake people make is adopting someone else’s definition of essential. Your essentials should reflect your actual life, responsibilities, and values—not some minimalist ideal.

Start with the non-negotiables:

- Housing (rent/mortgage, utilities, insurance)

- Transportation (car payment, gas, public transit, insurance)

- Food (groceries only—we’ll address this)

- Healthcare (medications, necessary appointments, insurance)

- Childcare or dependent care

- Minimum debt payments

Then consider your personal essentials:

- Do you have a medical condition requiring specific products?

- Are you in therapy or counseling? (Mental health is essential!)

- Do you have work-related expenses you can’t avoid?

- Are there obligations you’ve already committed to?

I learned this the hard way during my first no-spend attempt. I declared everything non-essential, including my therapy appointments. By week two, my mental health had deteriorated so badly that I stress-ate $60 worth of takeout in one weekend. Essential means essential to YOUR wellbeing and functioning, not some arbitrary standard.

Step 2: Create Your “Absolutely Not” List

This is where you get specific about what you’re NOT spending money on. Writing it down makes it real and gives you something to reference when temptation strikes.

Common “absolutely not” categories:

- Dining out, takeout, and food delivery

- Clothing, shoes, and accessories

- Entertainment (movies, concerts, events)

- Hobby supplies and craft materials

- Books, magazines, and digital content

- Personal care beyond basics (salon, spa, cosmetics)

- Home décor and non-essential household items

- Subscription boxes and memberships

- Gifts (communicate this to friends/family early!)

- Alcohol and recreational substances

Pro tip: Don’t just list categories. Write down your specific temptations. Mine included: “No Starbucks runs, no Amazon browsing, no Target ‘just looking’ trips, no online window shopping.” The more specific, the better.

Step 3: Prepare Your Environment (Remove Temptation)

Willpower is overrated and unreliable. Environmental design is where the magic happens. Before January 1st, take these concrete steps:

🗑️ Delete shopping apps from your phone (Amazon, Target, your favorite clothing stores)

📧 Unsubscribe from promotional emails (use a service like Unroll.me to batch this)

💳 Remove saved payment information from websites you frequent

📱 Turn off social media shopping features and unfollow accounts that trigger spending

🏠 Plan your routes to avoid stores and shopping areas

👥 Tell your people what you’re doing (accountability matters)

I also recommend the “30-day list” technique. When you want to buy something non-essential, add it to a list with the date. If you still want it after 30 days (when your challenge ends), consider it then. Spoiler: you’ll forget about 80% of items on this list.

Step 4: Stock Your Pantry and Plan Your Meals

Food is where most no-spend challenges fail. You can’t just “not eat,” so you need a solid strategy. This is particularly important if you’ve never meal-planned before.

Before January starts:

- Take inventory of what you already have (pantry, freezer, fridge)

- Plan simple, repetitive meals using those ingredients

- Make ONE strategic grocery trip for essentials

- Prep grab-and-go options for busy days

- Plan for social situations (bring food to gatherings)

The goal isn’t culinary excellence—it’s sustainability. My January meals were embarrassingly basic: overnight oats, bean-based soups, rice bowls, and pasta variations. But they cost about $150 for the entire month versus my usual $600+ on food.

If you’re looking for more comprehensive guidance on managing your food budget, check out these budgeting strategies that helped me save thousands.

Step 5: Design Your Tracking System

You don’t need a fancy app or complicated spreadsheet. You just need visibility into three things:

- Money saved (what you would have spent minus what you actually spent)

- Temptation moments (when you wanted to buy something but didn’t)

- Emotional patterns (how you felt when spending urges hit)

I used a simple notes app on my phone with daily entries:

January 3

- Wanted coffee at café: $5 saved

- Feeling: Tired and stressed

- Did instead: Made coffee at home, 10-min meditation

- Running total saved: $42

This simple tracking serves multiple purposes. It quantifies your progress, identifies patterns, and provides alternative coping strategies. Plus, watching that “saved” number climb is incredibly motivating.

For those who want more structure, the 30-day saving challenge offers an excellent framework that complements the no-spend approach.

Your Week-by-Week No Spend January Roadmap

Let me walk you through what each week typically looks like, so you know what to expect and how to navigate the inevitable challenges.

Week 1: The Honeymoon Phase (Days 1-7)

What to expect: High motivation, excitement, maybe even euphoria. You’re riding the New Year’s energy, and everything feels possible. The challenge feels almost easy.

Common pitfalls:

- Overconfidence leading to risky situations (browsing online “just to look”)

- Not having backup plans for social invitations

- Underestimating how often you typically spend money

Survival strategies:

- Lean into the excitement but stay vigilant

- Document every “almost spent” moment

- Find free activities to replace paid ones

- Connect with others doing the challenge (online communities are gold)

My week 1 reality: I felt like a financial genius. I smugly made coffee at home, packed lunches, and turned down happy hour invitations. I saved $127 in the first week alone and thought, “Why don’t I do this every month?” (Spoiler: week 2 humbled me significantly.)

Week 2: The Resistance Arrives (Days 8-14)

What to expect: The novelty wears off. You’re tired of eating the same meals. Your friends are going out without you. You really, really want to buy that thing you saw online. This is where most people quit.

Common pitfalls:

- Rationalization (“This is basically essential…”)

- Social FOMO reaching peak levels

- Boredom leading to browsing and temptation

- Emotional spending triggers intensifying

Survival strategies:

- Revisit your WHY (write it down before January starts)

- Find creative free entertainment

- Reach out to accountability partners

- Allow yourself small, free pleasures

- Remember: feelings aren’t emergencies

My week 2 reality: I had a terrible day at work and my brain screamed for retail therapy. I literally sat on my hands for 20 minutes, then called my sister instead of opening Amazon. I cried a little. Then I organized my closet and found $40 in old gift cards. The urge passed. I learned that spending urges peak at about 15 minutes, then diminish.

Week 3: The Adjustment (Days 15-21)

What to expect: Something shifts. You’ve proven you can do this. New habits are forming. You’re discovering free joys you’d forgotten about. The challenge feels less like deprivation and more like liberation.

Common pitfalls:

- Complacency (thinking you’ve “got this” and letting your guard down)

- Mid-month expenses you forgot about (subscriptions, bills)

- Comparison with others who seem to be doing it “better”

Survival strategies:

- Celebrate small wins daily

- Experiment with new free activities

- Journal about what you’re learning

- Start planning how you’ll maintain these habits post-January

My week 3 reality: I actually enjoyed my Saturday morning routine of coffee at home, reading library books, and going for a walk. I didn’t miss the $80 brunch ritual. I’d saved over $300 by this point and felt genuinely proud. I also discovered I could make restaurant-quality meals with YouTube tutorials and ingredients I already had.

Week 4: The Home Stretch (Days 22-31)

What to expect: You can see the finish line. You’re calculating total savings. You’re already thinking about February differently. You might even feel sad about the challenge ending.

Common pitfalls:

- Premature celebration spending (“I’ll just start a day early…”)

- Creating elaborate shopping lists for February 1st

- Not reflecting on lessons learned

Survival strategies:

- Document everything you’ve learned

- Calculate your total savings

- Plan a mindful, intentional first purchase for February

- Decide which habits you’ll keep long-term

- Share your story to inspire others

My week 4 reality: I saved $623 total (not counting the debt I didn’t accumulate). More importantly, I broke my Amazon addiction, discovered I didn’t need 90% of things I thought were essential, and felt genuinely calmer about money. I also learned I could handle uncomfortable emotions without spending my way out of them.

Beyond January: Making Your Financial Reset Permanent

Here’s the truth nobody tells you: no spend January isn’t really about January. It’s about using one intense month to illuminate patterns, build skills, and create momentum for lasting change.

The Habits Worth Keeping (Even When the Challenge Ends)

Not everything from your no-spend month needs to be permanent. Extreme restriction isn’t sustainable or enjoyable long-term. But certain practices are worth integrating into your regular life:

1. The 24-Hour Rule ⏰

Before any non-essential purchase, wait 24 hours. This simple pause eliminates impulse buying and gives your rational brain time to catch up with your emotional brain.

2. One-In-One-Out Policy 🔄

For every new item you bring into your home, something else leaves. This maintains the clarity and space you created during your no-spend month.

3. Weekly Money Dates 📅

Spend 15 minutes every Sunday reviewing your spending, planning the week ahead, and checking in with your financial goals. This prevents the autopilot spending that got you here in the first place.

4. Cash Cushion Building 💰

Take the money you saved during January and start an emergency fund. Even $500-$1,000 dramatically reduces financial stress and prevents future debt accumulation. For more on building financial resilience, explore these habits that help you stay debt-free for life.

5. Mindful Spending Categories 🎯

Instead of “no spend,” shift to “intentional spend.” Allocate money for things that genuinely enhance your life while cutting ruthlessly from categories that don’t.

Creating Your Personalized Post-Challenge Budget (Finally!)

If you’ve never successfully budgeted before, you now have something invaluable: data. Your no-spend month showed you exactly where your money normally goes and what you actually need versus what you habitually buy.

Use this insight to create a simple budget:

Essential Expenses (50-60% of income)

- Housing, utilities, transportation

- Groceries and household necessities

- Healthcare and insurance

- Minimum debt payments

Financial Goals (20-30% of income)

- Emergency fund building

- Debt payoff beyond minimums

- Retirement contributions

- Specific savings goals

Intentional Spending (20-30% of income)

- Dining out (with limits)

- Entertainment and hobbies

- Personal care and wellness

- Gifts and celebrations

The percentages are guidelines, not rules. Your budget should reflect your life, values, and goals. The key is that every dollar has a purpose—you’re telling your money where to go instead of wondering where it went.

If you’re interested in a structured approach, I found the 50/30/20 budget rule incredibly helpful for creating sustainable spending habits.

The Psychological Shift: From Scarcity to Abundance

This might sound counterintuitive, but the most profound benefit of no spend January isn’t the money you save—it’s the mindset shift that happens.

When you prove to yourself that you can be happy, fulfilled, and entertained without spending money, you break the scarcity-consumption cycle. You stop believing that happiness is one purchase away. You recognize that most of what you need, you already have.

This abundance mindset paradoxically makes you better with money. You spend less because you want less. You save more because you’re not filling emotional voids with stuff. You make financial decisions from a place of empowerment rather than desperation.

Signs you’ve achieved this shift:

- You browse stores without feeling compelled to buy

- You can be happy for others’ purchases without comparing

- You feel genuinely content with what you have

- You spend money confidently on things that matter

- You don’t use shopping as emotional regulation

Troubleshooting Common No Spend January Challenges

Let’s address the obstacles that trip people up, especially those new to financial challenges.

“But I Have to Attend a Wedding/Birthday/Event!”

Solution: Communicate early and get creative. Tell the host you’re doing a financial challenge and ask if you can contribute differently—make something homemade, offer to help set up, write a heartfelt letter. Most people are understanding and supportive.

If a gift is non-negotiable, set aside a small “obligation fund” before January starts. Or shop your home—regift something nice you never used, create a photo album from pictures you already have, or offer a service (babysitting, yard work, cooking a meal).

“My Friends Think I’m Being Cheap/Weird”

Solution: The right people will support you. Suggest free alternatives: hiking, game nights at home, potluck dinners, free community events, museum free days. If friends can’t hang out without spending money, that reveals something about the friendship, not about you.

Frame it positively: “I’m doing this financial challenge and I’d love your support. Can we do [free alternative] instead?” Real friends will adjust. Some might even join you.

“I Broke the Challenge—Should I Just Quit?”

Solution: Absolutely not. Perfection isn’t the goal; progress is. If you spend money on something non-essential, acknowledge it, understand why it happened, and continue. The challenge isn’t ruined by one slip.

Ask yourself:

- What triggered this purchase?

- What was I really seeking?

- What could I do differently next time?

- Can I return the item?

Then keep going. A 90% successful no-spend month is infinitely better than quitting on day 10.

“I’m So Bored Without My Usual Activities”

Solution: This is actually the most valuable part of the challenge. Boredom is uncomfortable, so we’ve built lives that eliminate it through consumption. Sitting with boredom allows creativity and self-discovery to emerge.

Free activities that saved my sanity:

- Library books, audiobooks, and movies

- YouTube workout videos and yoga classes

- Hiking and exploring local parks

- Learning new skills (cooking, languages, instruments)

- Connecting with friends and family

- Organizing and decluttering

- Starting a blog, journal, or creative project

- Volunteering in your community

Many people discover hobbies and interests during their no-spend month that become lifelong passions. Boredom is a gift if you let it be.

“My Partner/Family Isn’t On Board”

Solution: You can do a personal no-spend challenge even if others aren’t participating. Focus on your discretionary spending only. Don’t police others or create tension.

Explain your goals clearly: “I’m working on my relationship with money and impulse spending. I’m not asking you to change, but I’d appreciate your support in not tempting me or making me feel bad about this.”

Sometimes seeing your results inspires others to join. Sometimes it doesn’t. Either way, you’re making positive changes for yourself.

Advanced Strategies: Taking Your No-Spend Challenge to the Next Level

Once you’ve got the basics down, these advanced techniques can deepen the impact and insights from your financial reset.

The Spending Audit: Tracking Your “Almost Purchases”

Beyond tracking money saved, document every moment you almost spent money. Note:

- What you wanted to buy

- How much it cost

- What triggered the desire

- How you felt emotionally

- What you did instead

- How long the urge lasted

This creates a psychological profile of your spending patterns. You’ll discover that certain emotions, times of day, or situations consistently trigger spending urges. Armed with this knowledge, you can create specific strategies for your biggest triggers.

The Replacement Ritual Technique

For every spending habit you’re breaking, create a replacement ritual that provides similar emotional benefits without the cost.

Examples:

- Old habit: Starbucks run when stressed → New ritual: 5-minute breathing exercise + homemade special coffee

- Old habit: Online shopping when bored → New ritual: 20-minute walk + call a friend

- Old habit: Restaurant dinner for celebration → New ritual: Fancy home-cooked meal + candles + music

The key is making the replacement genuinely satisfying, not just a lesser substitute. This is how you build sustainable habits rather than white-knuckling through deprivation.

The Values Alignment Exercise

Use your no-spend month to get crystal clear on your values. When you remove spending as an option, you’re forced to ask: What actually matters to me?

Weekly reflection questions:

- What brought me genuine joy this week that cost nothing?

- What did I miss that I thought I’d miss but didn’t?

- What “essential” purchase turned out to be unnecessary?

- If I could only spend money on three categories forever, what would they be?

Your answers reveal your authentic values versus the values advertising and social conditioning have imposed on you. Future spending decisions become easier when aligned with your true values.

The Income Side: Boosting Earnings During No-Spend

While you’re cutting expenses, why not increase income? The combination is powerful. Your no-spend month frees up time previously spent shopping, browsing, and consuming. Redirect that energy toward earning.

Low-barrier income ideas:

- Sell items you’re decluttering (hello, double benefit!)

- Freelance skills you already have

- Online tutoring or coaching

- Pet sitting or house sitting

- Participating in research studies

- Gig economy work (delivery, rideshare)

The money you earn during your no-spend month can jumpstart your emergency fund or accelerate debt payoff. For more ideas, check out these realistic ways to make money from home.

The Science of Habit Formation: Why 31 Days Changes Everything

There’s a reason challenges are typically 30 days long—it’s not arbitrary. Understanding the neuroscience behind habit formation helps you appreciate what’s happening in your brain during no spend January.

The Three Stages of Habit Change

Stage 1: Disruption (Days 1-10)

Your brain is in active resistance. Old neural pathways are firing, expecting the usual rewards (shopping, spending, consuming). You’re using significant willpower to override these patterns. This stage is exhausting but crucial.

Stage 2: Adjustment (Days 11-20)

New neural pathways begin forming. The resistance lessens. Alternative behaviors start feeling more natural. You’re building what neuroscientists call “cognitive flexibility”—the ability to choose different responses to familiar triggers.

Stage 3: Integration (Days 21-31)

New patterns are solidifying. The behaviors that felt forced now feel normal. Your brain’s reward system is recalibrating, finding satisfaction in new sources. This is where lasting change happens [3].

Thirty-one days isn’t enough to make behaviors automatic (that takes 60-90 days), but it’s enough to prove they’re possible and begin the rewiring process. The key is continuing some version of these practices beyond January.

The Compound Effect of Small Decisions

Every time you choose not to spend money on something non-essential, you’re not just saving that specific amount. You’re:

✅ Strengthening your “spending resistance” muscle

✅ Proving to yourself that you can handle discomfort

✅ Breaking the stimulus-response pattern

✅ Creating evidence of your capability

✅ Building financial confidence

These psychological benefits compound. By day 20, saying no to a purchase that would have been impossible to resist on day 1 becomes almost easy. You’re literally becoming a different person—one with greater self-regulation and financial discipline.

Real Stories: How No Spend January Changed Lives

Let me share some transformations I’ve witnessed (names changed for privacy) that illustrate the power of this challenge beyond just the money saved.

Maria’s Story: From $8,000 in Credit Card Debt to Financial Freedom

Maria, a 29-year-old teacher, started no spend January 2024 with $8,000 in credit card debt and zero savings. She was spending $400+ monthly on dining out and $300+ on clothing she rarely wore.

Her January results: $687 saved, but more importantly, she identified that shopping was how she dealt with teaching stress. She replaced retail therapy with evening walks and journaling. By December 2024, she’d paid off all her credit card debt and built a $3,000 emergency fund.

“The no-spend month didn’t just change my bank account,” Maria told me. “It changed how I see myself. I’m not a person who’s ‘bad with money’ anymore. I’m someone who makes conscious choices about what matters.”

James’s Story: Discovering What Actually Makes Him Happy

James, a 35-year-old software engineer, earned six figures but somehow always felt broke. He participated in no spend January on a whim, expecting to hate it.

Instead, he discovered he’d been using expensive hobbies and gadgets to fill time he didn’t know what to do with. During his no-spend month, he reconnected with old friends, started running (free!), and realized he was deeply unsatisfied with his career.

“I was spending money to distract myself from the fact that I was unhappy,” James reflected. “When I couldn’t spend, I had to face that. It was uncomfortable, but it led to me making real changes.” He’s since switched careers, takes a $20,000 pay cut, but reports being significantly happier.

The Collective Impact: What the Data Shows

While individual stories are compelling, the aggregate data on no-spend challenges is equally impressive:

- Average savings: $500-$2,000 per month

- Debt reduction: 23% of participants pay off at least one debt completely

- Behavioral change: 67% report lasting changes to spending habits

- Psychological benefits: 81% report reduced financial anxiety

- Relationship improvement: 44% say it improved their relationship with money and/or their partner [4]

These aren’t just numbers—they represent real people breaking free from consumption cycles and building healthier financial lives.

Your No Spend January Toolkit: Resources and Templates

To set you up for success, here are practical tools you can use immediately.

The Essential vs. Non-Essential Worksheet

Create a simple two-column list before January starts:

| ✅ ESSENTIAL (Allowed) | ❌ NON-ESSENTIAL (Not Allowed) |

|---|---|

| Rent/Mortgage | Dining out/Takeout |

| Utilities | Clothing/Shoes |

| Groceries (list specific budget) | Entertainment/Movies |

| Medications | Hobby supplies |

| Transportation to work | Books/Digital content |

| Childcare | Alcohol |

| Insurance | Gifts |

| Minimum debt payments | Home décor |

| [Your specific essentials] | [Your specific temptations] |

The Daily Check-In Template

Copy this into your notes app or journal:

Date: __________

Money saved today: $______

Running total saved: $______

Temptation moments:

1. Wanted to buy: _____________ Cost: $_____

Feeling: _____________

Did instead: _____________

2. Wanted to buy: _____________ Cost: $_____

Feeling: _____________

Did instead: _____________

Wins today:

-

-

Challenges today:

-

-

Tomorrow's plan:

-

The Meal Planning Template

Breakfast rotation (pick 3-4 options):

- Option 1: _________________

- Option 2: _________________

- Option 3: _________________

Lunch rotation (pick 3-4 options):

- Option 1: _________________

- Option 2: _________________

- Option 3: _________________

Dinner rotation (pick 5-7 options):

- Option 1: _________________

- Option 2: _________________

- Option 3: _________________

- Option 4: _________________

- Option 5: _________________

Snacks available:

Free Entertainment Ideas List

Build your personal list before January starts:

Active/Outdoor:

- Hiking local trails

- Free community fitness classes

- Bike riding

- Park workouts

- Walking tours of your city

Learning/Growth:

- YouTube tutorials (cooking, language, skills)

- Library resources (books, movies, classes)

- Free online courses (Coursera, Khan Academy)

- Podcast exploration

- Skill practice (instrument, art, writing)

Social:

- Game nights at home

- Potluck dinners

- Video calls with distant friends

- Volunteering

- Free community events

Creative:

- Writing/journaling

- Drawing/painting

- Photography walks

- Home organization projects

- Decluttering and selling items

Relaxation:

- Meditation apps (many free versions)

- At-home spa treatments

- Reading

- Baths with items you already own

- Early bedtimes (seriously underrated!)

Avoiding Common Mistakes That Derail No-Spend Challenges

Learn from others’ failures so you don’t repeat them.

Mistake #1: Making It Too Restrictive

The problem: Declaring everything non-essential, including reasonable self-care, medications, or mental health support.

The fix: Be honest about what you truly need to function well. A sustainable challenge is better than a perfect one you abandon on day 5. Your challenge should be challenging but not punishing.

Mistake #2: Not Planning for Social Situations

The problem: Accepting social invitations without a plan, then feeling pressured to spend money or awkward explaining why you can’t.

The fix: Proactively suggest free alternatives when friends reach out. “I’d love to see you! I’m doing this financial challenge, so I can’t do dinner out, but want to come over for a home-cooked meal instead?” Most people are happy to adjust.

Mistake #3: Forgetting About Subscriptions and Auto-Payments

The problem: Subscription services and auto-renewals that hit mid-month, technically breaking your challenge.

The fix: Before January starts, audit all subscriptions. Cancel what you don’t need, and note what will renew during the month. Decide if you’ll allow these (they’re pre-committed) or if you’ll cancel and restart post-challenge.

Mistake #4: Not Having a Plan for the Money You Save

The problem: Saving money during January, then immediately spending it all on February 1st, negating the entire point.

The fix: Decide before January starts where your savings will go. Emergency fund? Debt payoff? Specific savings goal? Transfer the money immediately to that designated account so you’re not tempted to spend it.

For comprehensive guidance on avoiding financial pitfalls, review these budgeting mistakes to avoid.

Mistake #5: Doing It Alone Without Support

The problem: Trying to white-knuckle through the challenge in isolation, with no accountability or encouragement.

The fix: Find your people. Join online communities (Reddit’s r/nobuy, Facebook groups, Instagram hashtags), tell friends and family, or find an accountability partner. Support dramatically increases success rates.

Mistake #6: All-or-Nothing Thinking

The problem: One slip-up leads to “Well, I already failed, might as well quit.”

The fix: Progress over perfection. If you spend money on something non-essential, acknowledge it, learn from it, and continue. A 90% successful no-spend month is still transformative.

February 1st and Beyond: Transitioning Wisely

The end of your no spend January is just as important as the beginning. How you transition back to normal spending determines whether this was a one-month experiment or the start of lasting change.

The First Purchase Rule

Don’t rush out and buy everything you’ve been wanting. Instead, institute the “first purchase rule”: your first discretionary purchase after the challenge should be intentional, meaningful, and aligned with your values.

Questions to ask before buying:

- Do I still want this after 30 days?

- Does this align with my values?

- Will this genuinely improve my life?

- Can I afford this without debt?

- Have I considered alternatives?

This mindful first purchase sets the tone for how you’ll spend going forward.

The 80/20 Approach to Sustainable Spending

You probably don’t want to live in permanent no-spend mode (though some people discover they love it!). Instead, identify the 20% of spending restrictions that gave you 80% of the benefits.

For most people, this includes:

- Continuing to avoid impulse purchases (24-hour rule)

- Maintaining reduced dining out/takeout

- Keeping subscription minimalism

- Preserving some free entertainment habits

- Continuing to meal plan and cook at home

While relaxing:

- Occasional dining out with friends

- Purchasing needs as they arise

- Investing in meaningful experiences

- Buying items that align with values

Creating Your “Spending Permission Slip” Categories

A helpful post-challenge framework is creating categories where you give yourself explicit permission to spend, and others where you maintain restrictions.

Example framework:

Green light (spend freely within reason):

- Experiences with loved ones

- Health and wellness

- Education and skill-building

- Quality items that replace cheap ones

Yellow light (spend mindfully with limits):

- Dining out (set monthly limit)

- Entertainment (budget allocated)

- Clothing (needs only, quality focus)

- Gifts (meaningful, not obligatory)

Red light (continue avoiding):

- Impulse purchases

- Social comparison spending

- Emotional regulation spending

- Convenience spending that doesn’t add value

This framework prevents the pendulum swing from extreme restriction to extreme indulgence.

The Bigger Picture: No Spend January as Financial Self-Care

I want to leave you with a reframe that made all the difference for me: no spend January isn’t about deprivation. It’s about self-care.

We live in a culture that equates spending with self-care. “Treat yourself!” “You deserve it!” “Self-care Sunday!” are often code for buying things. But true self-care is doing what’s best for your long-term wellbeing, even when it’s uncomfortable in the moment.

Financial self-care looks like:

- Building an emergency fund so you can sleep at night

- Breaking debt cycles that create constant stress

- Developing spending discipline that creates freedom

- Aligning money with values that matter to you

- Creating space between impulse and action

- Choosing long-term security over short-term gratification

Your no spend January is an act of profound self-care. You’re investing in future you—the version who has savings, manageable debt, and a healthy relationship with money. That’s worth a month of discomfort.

The Ripple Effects Beyond Your Bank Account

The benefits of this challenge extend far beyond finances:

Environmental impact: Reduced consumption means less waste, fewer resources used, and a smaller carbon footprint. Many participants report developing environmental consciousness during their no-spend month.

Relationship quality: When you can’t default to spending money together, you find creative ways to connect. Many people report deeper friendships and relationships after their challenge.

Mental clarity: The constant barrage of consumer decisions creates decision fatigue. Removing those choices frees up mental energy for things that actually matter.

Life satisfaction: Research consistently shows that experiences and relationships drive happiness, not possessions. Your no-spend month reorients you toward what actually creates wellbeing [5].

Time freedom: Shopping, browsing, and managing stuff takes time. Participants often discover they have 5-10 extra hours per week when they stop consuming.

Your Action Plan: Starting Your No Spend January Journey Today

Even if it’s not January yet, you can start preparing now. In fact, preparation is the key to success.

30 Days Before Your Challenge Starts

- Define your essential vs. non-essential categories

- Audit and cancel unnecessary subscriptions

- Tell friends and family about your plans

- Find an accountability partner or online community

- Create your tracking system

- Stock your pantry and plan meals

- Delete shopping apps and unsubscribe from promotional emails

- Set up automatic transfers for money you’ll save

- Write down your WHY (why are you doing this?)

- Plan free activities for each weekend

7 Days Before Your Challenge Starts

- Do one final grocery shop

- Remove saved payment info from websites

- Prep grab-and-go meals and snacks

- Create your daily check-in template

- Set phone reminders for daily tracking

- Plan your first week’s meals specifically

- Identify your biggest temptations and create strategies

- Set up a separate savings account for money saved

- Review your calendar for potential challenges (events, obligations)

- Do a final mindset reset (this is self-care, not punishment!)

Day 1 of Your Challenge

- Morning: Read your WHY statement

- Set up your tracking for the day

- Take a “before” screenshot of your bank accounts

- Post about your challenge for accountability (if comfortable)

- Prepare your meals for the day

- Remove temptation (avoid stores, shopping areas)

- Evening: Complete your daily check-in

- Celebrate making it through day 1!

Weekly Throughout Your Challenge

- Sunday: Review the week, plan the next week, meal prep

- Mid-week check-in with accountability partner

- Calculate running total of money saved

- Adjust strategies based on what’s working/not working

- Celebrate wins, learn from challenges

- Share insights with your community

- Reflect on emotional patterns and triggers

Conclusion: Your Financial Transformation Starts Now

Here’s what I know for sure after completing multiple no-spend challenges and watching hundreds of others do the same: no spend January works. Not just for saving money (though you’ll definitely do that), but for fundamentally changing how you relate to spending, consumption, and your own self-discipline.

You don’t need to be a budgeting expert. You don’t need perfect willpower. You don’t need to become a minimalist or live like a monk. You just need to commit to 31 days of intentional choices and genuine curiosity about your spending patterns.

The money you save is the least important benefit. The real transformation happens in:

✨ Discovering you’re stronger than you thought

✨ Breaking autopilot spending habits

✨ Finding joy in free experiences

✨ Developing genuine financial confidence

✨ Creating space between impulse and action

✨ Aligning spending with your actual values

✨ Proving that happiness doesn’t require consumption

Your financial reset doesn’t have to wait until next January. You can start a no-spend challenge any month, any time. But there’s something powerful about January—the collective energy of millions doing this together, the natural reset point, the post-holiday motivation.

Your next steps:

- Decide right now that you’re doing this (commitment is everything)

- Define your essentials based on your actual life and needs

- Set up your tracking system (keep it simple!)

- Tell someone about your plan (accountability matters)

- Start preparing your environment for success

- Join a community for support and encouragement

- Begin on January 1st (or the 1st of any month) with confidence

Remember: every person who’s successfully completed this challenge felt the same doubts you’re feeling right now. The difference between them and people who never try is simply this—they started anyway.

You’ve got this. Your future self—the one with savings, reduced debt, and a healthy relationship with money—is cheering you on. The only question is: are you ready to meet them?

Let’s crush this no spend January together. 💪💰