I remember the exact moment I realized I was trapped. Sitting at my kitchen table at 2 AM, surrounded by bills I couldn’t pay, credit card statements that made my stomach turn, and a bank account that laughed at my dreams. Sound familiar? If you’re nodding your head right now, I want you to know something: financial freedom isn’t just for the wealthy or the lucky—it’s achievable for anyone willing to take intentional steps forward, even if you’re drowning in debt right now.

Learning how to achieve financial freedom transformed my life from paycheck-to-paycheck anxiety to genuine peace of mind. And here’s the truth that nobody tells you: it’s not about making six figures or inheriting money. It’s about understanding the psychology of money, making strategic decisions, and building systems that work while you sleep. In this comprehensive guide, I’ll walk you through the exact five-step framework that helped me break free from the debt cycle and build sustainable wealth—and how you can do it too, starting today in 2026.

Key Takeaways

- Financial freedom is a mindset shift first, strategy second—your relationship with money determines your success more than your current income

- The five-step framework (mindset, budget, debt elimination, investing, passive income) works regardless of your starting point, even with significant debt

- Technology and automation are your secret weapons for staying consistent and building wealth without constant willpower

- Passive income streams are no longer optional—they’re essential for true financial independence in the modern economy

- Small, consistent actions compound exponentially—you don’t need perfection, you need persistence

Step 1: Master the Money Mindset That Changes Everything 🧠

Before we dive into spreadsheets and strategies, let’s address the elephant in the room: your brain is literally wired to sabotage your financial success. Neuroscience research shows that our brains developed survival mechanisms for scarcity that actively work against wealth building in modern society[1].

Understanding Your Financial Psychology

The first step in how to achieve financial freedom isn’t opening a savings account—it’s rewiring your money psychology. I spent years wondering why I kept making the same financial mistakes until I discovered that my childhood experiences with money had created subconscious patterns that controlled my adult decisions.

Here’s what shifted for me:

- Scarcity mindset to abundance mindset: Instead of “I can’t afford this,” I started asking “How can I afford this?”

- Shame to curiosity: Rather than avoiding my financial situation, I got genuinely curious about my spending patterns

- Instant gratification to delayed gratification: I trained my brain to value future rewards over immediate pleasure

The Emotional Intelligence Factor

Financial wellness isn’t just about numbers—it’s deeply connected to mental health and emotional regulation. Studies show that financial stress activates the same brain regions as physical pain[2]. This means that avoiding your debt or financial situation is literally your brain trying to protect you from pain.

Practical mindset shifts to implement today:

- Practice financial gratitude daily: Write down three things you appreciate about your current financial situation, even if it’s just “I have a plan now”

- Reframe debt as a teacher: Every debt tells a story about what you valued at that moment—learn from it without judgment

- Visualize your financially free self: Spend 5 minutes daily imagining your life without financial stress in vivid detail

- Challenge limiting beliefs: When you catch yourself thinking “I’m bad with money,” replace it with “I’m learning to manage money effectively”

The connection between money mindset and actual financial outcomes is staggering. Research from financial psychologists shows that people who believe they can improve their financial situation are 3x more likely to actually do so[3].

Step 2: Build Your Financial Foundation with Strategic Budgeting 💰

Now that your mindset is shifting, let’s talk about the tactical foundation of how to achieve financial freedom: a budget that actually works for your life, not against it.

I’ve tried every budgeting method under the sun—zero-based budgeting, envelope systems, the 50/30/20 rule—and here’s what I learned: the best budget is the one you’ll actually stick to. For me, that meant combining technology with behavioral psychology.

The Budget Framework That Works in 2025

Traditional budgeting fails because it requires constant willpower and manual tracking. Instead, I use what I call the “Automated Awareness System”:

| Budget Category | Percentage of Income | Automation Strategy |

|---|---|---|

| Essentials (housing, utilities, food) | 50-60% | Auto-pay from checking account |

| Debt Repayment | 15-25% | Automatic transfer on payday |

| Savings & Investments | 15-20% | Auto-transfer to separate accounts |

| Lifestyle & Discretionary | 10-15% | Prepaid debit card with weekly reload |

The key insight? Automate the important stuff first, then spend what’s left guilt-free. This removes decision fatigue and makes good financial behavior the default.

Technology Tools That Changed My Financial Life

In 2025, there’s absolutely no excuse for manual budget tracking. Here are the tools I use daily:

- Budgeting apps: YNAB (You Need A Budget) or Mint for real-time expense tracking

- Automated savings: Apps like Digit or Qapital that save money based on your spending patterns

- Bill negotiation: Trim or Truebill to automatically lower recurring bills

- Investment automation: Acorns or Betterment for round-up investing

I also recommend checking out these budgeting mistakes to avoid that trip up most people in their first year.

The Zero-Sum Budget Hack

Here’s a game-changer: every dollar needs a job before the month begins. This doesn’t mean you can’t have fun money—it means you intentionally decide where every dollar goes, including entertainment and spontaneous spending.

My monthly budgeting ritual (takes 30 minutes):

- List all income sources for the coming month

- Assign every dollar to a category (including “fun money”)

- Set up automatic transfers for savings and debt payments

- Review last month’s actual spending vs. planned spending

- Adjust categories based on real patterns, not ideal ones

The psychological benefit of this approach is profound: you eliminate the guilt around spending because you’ve already given yourself permission within boundaries.

Step 3: Eliminate Debt Strategically (Your Path to Breathing Room) 🎯

Let’s get real about debt: it’s the single biggest obstacle to financial freedom for most people. I had $47,000 in student loans, $12,000 in credit card debt, and a car payment that made me wince every month. But here’s what I learned: debt elimination isn’t about deprivation—it’s about strategic prioritization.

The Debt Elimination Framework That Actually Works

There are two primary strategies, and the right one depends on your psychology:

1. The Avalanche Method (mathematically optimal)

- Pay minimums on all debts

- Put extra money toward highest interest rate first

- Saves the most money in interest

- Best for people motivated by numbers and efficiency

2. The Snowball Method (psychologically optimal)

- Pay minimums on all debts

- Put extra money toward smallest balance first

- Creates quick wins and momentum

- Best for people who need motivation and visible progress

I used a hybrid approach: snowball for the first three months to build momentum, then switched to avalanche once I had the psychological wins under my belt. You can explore more proven ways to pay down debt faster that combine both strategies.

Income Diversification for Faster Debt Payoff

Here’s the uncomfortable truth: you can’t budget your way out of a massive income problem. If your debt is substantial relative to your income, you need to focus on earning more, not just spending less.

Side income strategies that worked for me in 2025:

- Freelancing my existing skills: Made an extra $800/month doing graphic design on weekends

- Selling unused items: Generated $2,400 in the first 90 days from stuff I didn’t need

- Gig economy work: Drove for rideshare during peak hours (Friday/Saturday nights) for $400-600/month

- Online tutoring: Taught English online for $25/hour, 5 hours per week

For more ideas, check out these realistic ideas for making money from home that don’t require special skills or massive time investments.

The Debt-Free Timeline Reality Check

Most financial gurus promise you can be debt-free in 12 months. For some people with moderate debt and good incomes, that’s realistic. For others, it’s a setup for failure and shame.

My realistic timeline approach:

- Calculate total debt ÷ realistic monthly payment = actual timeline

- Add 20% buffer for life happening (because it will)

- Celebrate every 25% milestone, not just the finish line

- Adjust as income increases or expenses change

I was able to become debt-free in 12 months by following a structured plan, but your timeline might be different—and that’s completely okay. The goal is progress, not perfection.

Protecting Your Credit While Paying Off Debt

Here’s something crucial: how you pay off debt matters almost as much as paying it off. Your credit score impacts everything from apartment rentals to job opportunities to insurance rates.

Credit protection strategies:

- Never miss minimum payments (set up auto-pay)

- Keep credit utilization below 30% on all cards

- Don’t close old credit cards (age of credit matters)

- Monitor your credit score monthly with free tools

- Dispute any errors immediately

Learn more about things that hurt your credit score that most people don’t realize, and discover proven ways to raise your credit score fast while paying down debt.

Step 4: Build Wealth Through Smart, Simple Investing 📈

Once you’ve got your budget dialed in and you’re making progress on debt, it’s time to talk about the step that actually builds lasting wealth: investing. This is where how to achieve financial freedom shifts from defense (managing money) to offense (growing money).

I used to think investing was only for rich people or finance bros who understood complex charts. That limiting belief cost me years of compound growth. The truth? Investing in 2025 is more accessible, affordable, and automated than ever before.

Investment Fundamentals for Beginners

Let me break down investing in the simplest possible terms:

Investing = putting money into assets that grow in value over time

That’s it. You’re not gambling, you’re not timing the market, you’re simply participating in the long-term growth of the economy.

The three core investment vehicles for beginners:

- Index Funds/ETFs: Baskets of stocks that track the overall market (my favorite: VTSAX, VOO, or VTI)

- Retirement Accounts: 401(k)s and IRAs that give you tax advantages for long-term saving

- Real Estate: Starting with REITs (real estate investment trusts) before physical property

The Investment Timeline Strategy

Here’s the framework I use to decide where to invest based on when I’ll need the money:

| Timeline | Investment Type | Expected Return | Risk Level |

|---|---|---|---|

| 0-2 years | High-yield savings account | 4-5% | Very Low |

| 2-5 years | Bond funds, CDs | 5-7% | Low |

| 5-10 years | Balanced index funds (60/40 stocks/bonds) | 7-9% | Moderate |

| 10+ years | Stock index funds | 10-12% | Higher (but time smooths volatility) |

The psychological game-changer for me was understanding that market volatility is only scary if you need the money soon. When you’re investing for 20+ years, market dips are actually buying opportunities.

Starting to Invest with Little Money

You don’t need $10,000 to start investing. In 2025, you can literally start with $5. Here’s my recommended progression:

Phase 1: The First $1,000

- Open a Roth IRA with Fidelity, Vanguard, or Charles Schwab

- Invest in a target-date retirement fund (they automatically adjust risk as you age)

- Set up automatic $50-100 monthly contributions

Phase 2: Building to $10,000

- Increase contributions as you pay off debt

- Start learning about individual index funds

- Consider employer 401(k) match (it’s literally free money)

Phase 3: Diversification ($10,000+)

- Spread across multiple index funds

- Add international exposure (VXUS or similar)

- Consider small allocation to bonds for stability

For those just starting out, I highly recommend this guide on investing in stocks for beginners with little money that breaks down the exact steps.

The Compound Interest Miracle

This is where investing gets exciting. Compound interest is literally the only financial magic that exists. Let me show you with real numbers:

- Scenario A: Invest $200/month starting at age 25, stop at 35 (total: $24,000 invested)

- Scenario B: Invest $200/month starting at age 35, continue until 65 (total: $72,000 invested)

At age 65, assuming 10% average annual returns:

- Scenario A: $580,000+

- Scenario B: $380,000+

Starting early with less money beats starting late with more money. Every single time. The key is time in the market, not timing the market.

Avoiding Common Investment Mistakes

I made every rookie mistake in the book. Here’s what NOT to do:

❌ Don’t: Try to pick individual stocks unless you genuinely enjoy research and can stomach volatility

✅ Do: Stick with broad index funds that own thousands of companies

❌ Don’t: Panic sell when the market drops

✅ Do: View market dips as sales on future wealth

❌ Don’t: Keep all your investments in one account or asset type

✅ Do: Diversify across account types (taxable, Roth, traditional) and asset classes

❌ Don’t: Pay high fees for actively managed funds

✅ Do: Choose low-cost index funds (under 0.20% expense ratio)

Step 5: Create Passive Income Streams (The Ultimate Freedom) 💸

Here’s where we shift from traditional wealth building to genuine financial independence. Passive income is money you earn without trading your time directly for dollars. This is the final piece of how to achieve financial freedom that most people never reach—and it’s the difference between being financially comfortable and being truly free.

What Actually Counts as Passive Income?

Let’s get clear on definitions because there’s a lot of BS in the passive income space. True passive income requires upfront work but then generates ongoing revenue with minimal maintenance.

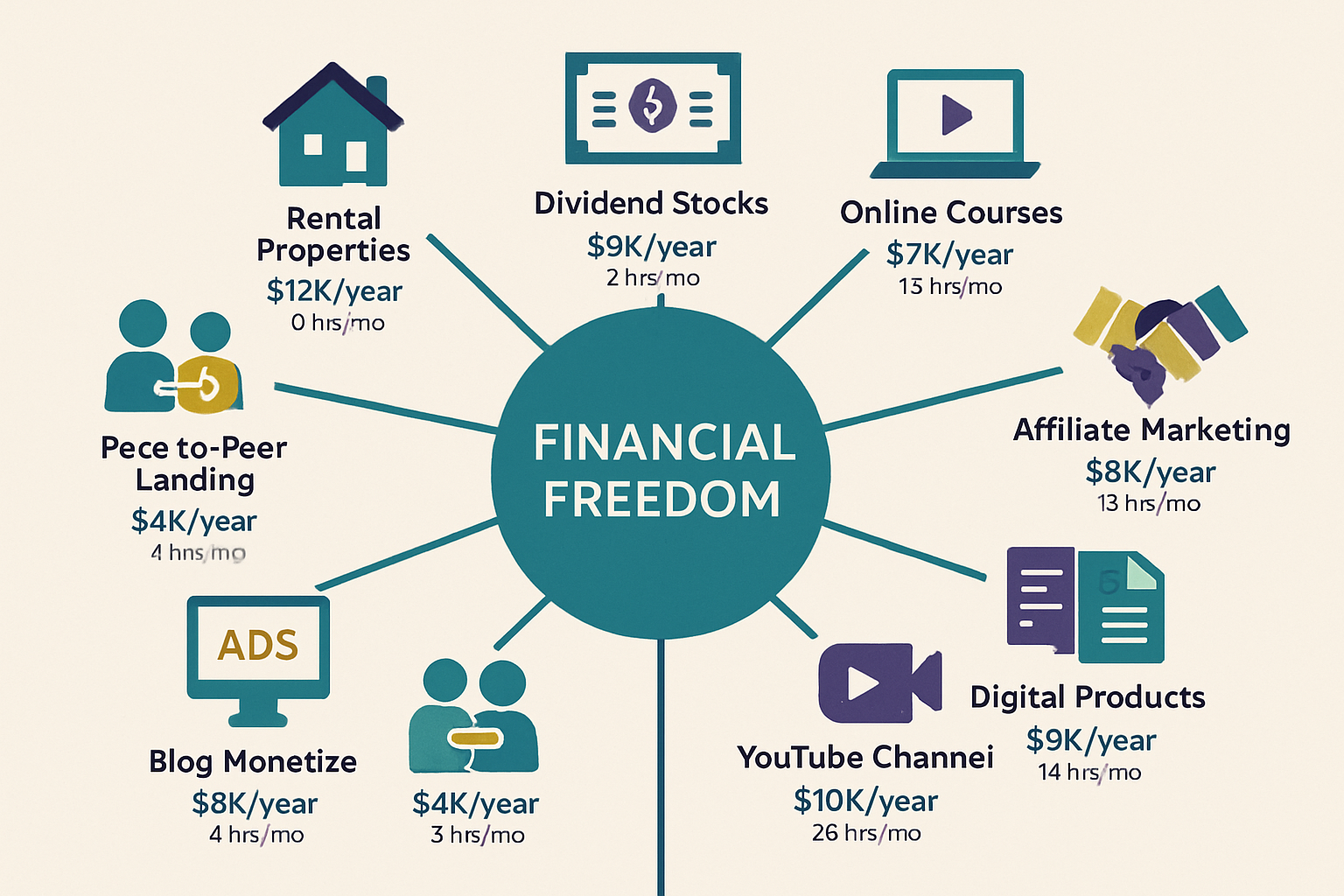

Legitimate passive income streams:

- Dividend-paying investments: Stocks and funds that pay you quarterly just for owning them

- Rental property income: Real estate that generates monthly cash flow (after expenses)

- Digital products: Ebooks, courses, templates you create once and sell repeatedly

- Affiliate marketing: Earning commissions by recommending products you genuinely use

- YouTube ad revenue: Videos that continue earning long after you publish them

- Blog monetization: Content that ranks in search engines and generates ad/affiliate income

- Peer-to-peer lending: Earning interest by lending money through platforms

- Royalties: From books, music, photography, or other creative work

For a comprehensive breakdown, check out these passive income ideas that work in 2026 with realistic earning expectations.

My Passive Income Journey (Real Numbers)

I’m going to be completely transparent about my passive income progression:

Year 1: $127/month (mostly from dividend stocks and one small digital product)

Year 2: $843/month (added affiliate marketing and YouTube channel)

Year 3: $2,400/month (blog started ranking, dividend portfolio grew, created online course)

Year 4: $5,100/month (rental property, multiple income streams compounding)

Notice it’s not “quit your job in 90 days” territory. Real passive income builds slowly, then compounds rapidly. The key is starting multiple small streams that grow over time.

The Passive Income Starter Blueprint

If you’re starting from zero, here’s my recommended progression:

Phase 1: Foundation (Months 1-6)

- Build dividend stock portfolio with $100-500/month investments

- Start documenting your financial freedom journey (blog, YouTube, or social media)

- Identify 2-3 products/services you genuinely use and love for affiliate marketing

Phase 2: Creation (Months 6-12)

- Create your first digital product (template, guide, or mini-course) based on your expertise

- Grow your content platform consistently (2-3 posts/videos per week)

- Reinvest early passive income into growing the streams

Phase 3: Scaling (Year 2+)

- Automate and systematize successful streams

- Add new streams strategically (don’t spread too thin)

- Consider real estate or business ownership for larger passive income

The Income Diversification Principle

Here’s a critical insight: true financial freedom comes from multiple income sources, not one big one. If you lose your job but have 4-5 passive income streams generating $500-1,000 each, you’re far more financially resilient than someone making $150k from one source.

My current income diversification (as of 2025):

- 40% – Primary employment

- 25% – Dividend investments

- 15% – Digital products and courses

- 10% – Affiliate marketing

- 10% – Rental property cash flow

This diversification means no single income loss would devastate my financial situation. That’s the real definition of financial security.

Realistic Timeline Expectations

The passive income gurus won’t tell you this, but I will: most passive income streams take 12-24 months to generate meaningful money. The exception is dividend investing, which starts paying immediately but requires substantial capital to be significant.

Realistic passive income timelines:

- Dividend stocks: Immediate small payments, grows with capital invested

- Rental property: 3-6 months to acquire and stabilize, then ongoing

- Blog/YouTube: 12-18 months to build audience and start earning

- Digital products: 3-6 months to create and launch, then ongoing sales

- Affiliate marketing: 6-12 months to build trust and audience

The compound effect happens when you start multiple streams with staggered timelines. While stream #1 is in month 18 and generating well, streams #2 and #3 are in months 6 and 12, building momentum.

The Financial Freedom Lifestyle: What It Actually Looks Like 🌟

Let me paint you a picture of what financial freedom actually feels like, because I think there’s a lot of misconception about this.

Financial freedom doesn’t mean:

- Never working again (unless you want that)

- Buying whatever you want without thinking

- Living on a beach drinking cocktails 24/7 (though you could)

- Having millions in the bank

Financial freedom actually means:

- Choosing work you find meaningful, not just work that pays bills

- Making spending decisions based on values, not scarcity

- Having options when life throws curveballs

- Sleeping peacefully without money anxiety

- The ability to say “no” to things that don’t serve you

For me, financial freedom meant leaving a toxic job without panic, taking a month off to travel without debt, and choosing to work part-time on projects I’m passionate about. It’s not about the money itself—it’s about the choices money enables.

The Lifestyle Optimization Strategy

Once you’re on the path to financial freedom, lifestyle optimization becomes crucial. This means intentionally designing a life that’s both financially sustainable and genuinely fulfilling.

Questions I ask myself quarterly:

- What am I spending money on that doesn’t actually bring me joy?

- What experiences or purchases would genuinely improve my quality of life?

- Am I working toward someone else’s definition of success or my own?

- How can I increase income without sacrificing health or relationships?

- What would I do if money weren’t a factor? (Then figure out how to make that financially viable)

This kind of intentional reflection prevents lifestyle inflation and keeps you aligned with your actual values, not society’s expectations.

Building Generational Wealth

One aspect of financial freedom that doesn’t get enough attention: the ability to change your family’s financial trajectory for generations. This isn’t just about leaving an inheritance—it’s about teaching financial literacy, creating opportunities, and breaking cycles of financial stress.

Ways I’m building generational wealth:

- Teaching nieces and nephews about money through age-appropriate conversations

- Creating trust funds with automatic investing for future generations

- Documenting financial lessons learned so family members can benefit

- Building businesses and assets that can be passed down

- Investing in education (mine and others’) as the ultimate wealth multiplier

The psychological shift from “I need to survive” to “I can create lasting impact” is profound. That’s when financial freedom becomes financial legacy.

Overcoming the Psychological Barriers to Financial Freedom 🚧

Let’s address the mental roadblocks that stop most people from achieving financial freedom, even when they know exactly what to do.

The Perfectionism Trap

I see this constantly: people wait for the “perfect” time to start budgeting, investing, or building passive income. They think they need to understand everything before they begin. This is procrastination disguised as preparation.

The truth? You’ll never feel completely ready. I started investing before I fully understood P/E ratios. I launched my first digital product before I knew proper marketing. Imperfect action beats perfect planning every single time.

How to overcome perfectionism:

- Set a deadline for research, then act (I use the “72-hour rule”: research for 72 hours max, then decide)

- Embrace “version 1.0” thinking—everything can be improved later

- Reframe mistakes as data collection, not failures

- Start with small, low-risk experiments

The Comparison Paralysis

Social media makes this worse. You see someone your age who’s already “financially free” and feel like you’re behind. Here’s what I learned: comparison is the thief of joy and the killer of progress.

Everyone’s starting point is different. Someone who inherited money, graduated debt-free, or got lucky with early Bitcoin isn’t on your timeline. Your only competition is who you were yesterday.

I use these simple habits that help you stay debt-free for life to focus on my own progress rather than comparing myself to others.

The Scarcity Hangover

Even after you start making financial progress, old scarcity patterns can linger. I call this the “scarcity hangover”—when you’re objectively doing well financially but still feel anxious about money.

Signs of scarcity hangover:

- Difficulty spending money on yourself even when budgeted

- Constant fear that financial success is temporary

- Inability to celebrate financial wins

- Hoarding money beyond reasonable emergency funds

Healing scarcity mindset:

- Work with a financial therapist or money coach

- Practice intentional “joy spending” within budget

- Celebrate every financial milestone, no matter how small

- Develop trust in your systems and abilities

Your 30-Day Financial Freedom Kickstart Plan 📅

Theory is useless without action. Here’s your concrete 30-day plan to start your financial freedom journey today:

Week 1: Awareness and Assessment

- Day 1-2: Track every single expense (use an app or notebook)

- Day 3: Calculate your total net worth (assets minus liabilities)

- Day 4: List all debts with interest rates and minimum payments

- Day 5: Identify your money mindset patterns (journaling exercise)

- Day 6: Research budgeting apps and choose one

- Day 7: Review week and set one specific financial goal

Week 2: Foundation Building

- Day 8-9: Create your first budget using chosen method

- Day 10: Set up automatic bill payments

- Day 11: Open high-yield savings account for emergency fund

- Day 12: Set up automatic transfer to savings ($25-100 to start)

- Day 13: Research investment accounts (Roth IRA options)

- Day 14: Review and adjust budget based on first week of tracking

Try the 30-day saving challenge to build momentum, or explore these savings strategy hacks that helped me save $3,000 in 90 days.

Week 3: Debt and Income Strategy

- Day 15: Choose debt payoff method (avalanche or snowball)

- Day 16: Create debt payoff timeline and milestones

- Day 17: Brainstorm 10 ways to increase income

- Day 18: Choose one side income idea to test

- Day 19: Spend 2 hours on side income setup

- Day 20: Review credit report for errors

- Day 21: Celebrate progress and adjust plan as needed

Week 4: Investment and Passive Income Launch

- Day 22: Open investment account (Roth IRA or brokerage)

- Day 23: Make first investment ($50-500 in index fund)

- Day 24: Set up automatic monthly investment contribution

- Day 25: Choose one passive income stream to develop

- Day 26: Create 90-day action plan for passive income stream

- Day 27: Take first action on passive income (create outline, research, etc.)

- Day 28: Review entire month’s progress

- Day 29: Adjust budget and systems based on real data

- Day 30: Set goals for next 90 days and celebrate wins!

This plan is designed to build momentum through small, consistent actions. You’re not trying to transform your entire financial life in 30 days—you’re building the foundation and habits that will carry you forward.

Common Questions About Achieving Financial Freedom

How long does it take to achieve financial freedom?

There’s no universal timeline because it depends on your starting point, income, expenses, and definition of “financial freedom.” For some, it’s 5 years; for others, 20+ years. The average person following a structured plan can achieve significant financial independence in 7-12 years. The key is starting now, not waiting for perfect conditions.

Can I achieve financial freedom with a low income?

Absolutely, though it requires more creativity and typically takes longer. Focus on: (1) increasing income through skills development and side hustles, (2) keeping expenses extremely lean, (3) investing even small amounts consistently, and (4) building passive income streams. Many people have achieved financial freedom starting from minimum wage by being intentional and patient.

Should I invest while I still have debt?

It depends on the interest rates. High-interest debt (above 7-8%) should generally be paid off before investing heavily. However, you should always contribute enough to get employer 401(k) match (it’s free money) and build a small emergency fund first. For low-interest debt (under 5%), investing while paying it off can make mathematical sense.

What’s the difference between financial freedom and financial independence?

These terms are often used interchangeably, but I see them as a spectrum. Financial independence means your passive income covers your basic living expenses—you don’t need a job to survive. Financial freedom goes further—it means having enough that you can make choices based purely on what you want, not what you need financially.

How much money do I need to be financially free?

A common guideline is the “25x rule”—save 25 times your annual expenses, then you can safely withdraw 4% annually indefinitely. So if you spend $40,000/year, you’d need $1 million invested. However, if you build passive income streams that cover expenses, you need far less in investments. I prefer the “multiple streams” approach over relying on one large number.

Conclusion: Your Financial Freedom Journey Starts Now

We’ve covered a lot of ground—from the psychology of money to specific investment strategies, from debt elimination to passive income creation. But here’s what I want you to remember: how to achieve financial freedom isn’t about one perfect decision or lucky break. It’s about consistent, intentional actions compounded over time.

You don’t need to implement everything at once. Start with the mindset work and basic budgeting. Get that foundation solid, then add debt elimination. Once you’re making progress there, start investing. Finally, layer in passive income streams. Each step builds on the previous one.

The most important thing? Start today. Not next month when you get a raise. Not next year when you’ve paid off more debt. Today. Even if it’s just tracking your expenses for one week or opening a high-yield savings account. Small actions create momentum, and momentum creates transformation.

I’m not going to lie and say it’s easy. There were months I wanted to give up, times I felt like I was making no progress, and moments of doubt about whether financial freedom was really possible for someone like me. But every small decision—every budget created, every debt payment made, every dollar invested—was a vote for the future I wanted.

Your next steps:

- This week: Complete Week 1 of the 30-day kickstart plan above

- This month: Set up your budget and automation systems

- This quarter: Make your first investment and choose a debt payoff strategy

- This year: Build your first passive income stream and increase your net worth by at least 20%

Financial freedom isn’t a destination—it’s a journey of continuous growth, learning, and intentional choices. You’re not going to do it perfectly, and that’s completely okay. What matters is that you’re moving forward, one decision at a time.

The life you want—the one where money is a tool for freedom rather than a source of stress—is absolutely achievable. I’ve done it, thousands of others have done it, and you can too. Your financial freedom story starts the moment you decide it does.

Ready to take control of your financial future? Visit MSBudget for more resources, tools, and step-by-step guides to support your journey to financial freedom. Your future self will thank you for starting today.