Picture this: you’re scrolling through home listings late at night, dreaming about which bedroom would be your home office and where you’d put the couch. But then reality hits—how do you actually pay for a house? I’ve been there, and I’m here to tell you that navigating the loan process doesn’t have to feel like solving a Rubik’s cube blindfolded. This Homebuyer’s Loan Guide walks you through every step, from getting pre-approved to holding those shiny new keys in your hand.

Key Takeaways

- Pre-approval takes 3-5 days and requires credit reports, income verification, and bank statements—get this done before house hunting to strengthen your offers

- FHA loans remain the most accessible option for first-time buyers with credit scores as low as 580 and down payments starting at just 3.5%

- 2026 loan limits increased significantly, giving buyers $20,000-$40,000 more purchasing power compared to 2025

- Zero-down options exist through VA loans (for veterans) and USDA loans (for rural/suburban properties), plus state assistance programs can cover down payments

- Timing matters—winter months offer seller concessions of $5,000-$9,000 and properties priced 1.8% below list on average

Quick Answer

Getting a home loan as a first-time buyer involves five main steps: securing pre-approval (which takes 3-5 days and proves you’re a serious buyer), shopping for homes within your budget, making an offer, completing the underwriting process (30-45 days), and closing on your new home. The best loan type depends on your situation—FHA loans work for credit scores as low as 580 with 3.5% down, VA loans offer zero-down options for military members, USDA loans provide zero-down financing for eligible rural areas, and conventional loans suit buyers with 620+ credit scores and stable income.

What Is Pre-Approval and Why Do I Need It Before House Hunting?

Pre-approval is a lender’s written commitment stating how much they’re willing to loan you based on verified financial information. You need it before house hunting because it shows sellers you’re a serious buyer with financing already lined up, which strengthens your offer in competitive markets.

Here’s what happens during pre-approval:

Documents You’ll Need:

- Last 2 years of tax returns

- Recent pay stubs (usually last 30 days)

- W-2s from the past 2 years

- Bank statements from the last 2-3 months

- Government-issued ID

- Proof of any additional income sources

What Lenders Check:

- Credit score: Most programs require 580-640+ (FHA accepts 580, conventional typically needs 620)

- Debt-to-income ratio: FHA allows up to 56.9%, with some lenders approving 57% for borrowers with strong compensating factors[2][4]

- Employment history: Typically 2 years of steady employment

- Assets: Cash reserves for down payment and closing costs

The process typically takes 3-5 days, and you’ll receive a pre-approval letter valid for 60-90 days. This letter specifies the maximum loan amount you qualify for, which helps you focus on homes within your actual budget rather than wasting time on properties you can’t afford.

Common mistake: Don’t confuse pre-qualification with pre-approval. Pre-qualification is a quick estimate based on self-reported information, while pre-approval involves actual verification of your finances and carries much more weight with sellers.

Before you even start this process, make sure your finances are in order. Check out our guide on raising your credit score fast if you need to boost your numbers before applying.

Which First-Time Homebuyer Loan Programs Should I Consider in 2026?

The four main loan types for first-time buyers are FHA, VA, USDA, and conventional loans—each designed for different financial situations and eligibility requirements. Choose based on your credit score, down payment savings, military status, and where you’re buying.

FHA Loans: The Most Accessible Option

FHA loans remain the go-to choice for buyers with lower credit scores or limited savings. With a minimum credit score of 580, you qualify for a 3.5% down payment. If your score falls between 500-579, you’ll need 10% down[2].

FHA advantages in 2026:

- Debt-to-income ratios up to 56.9% accepted[2][4]

- Loan limits increased, providing $20,000-$40,000 more purchasing power than 2025[1]

- Baseline conforming limit rose to $832,750 for one-unit properties[3]

- More flexible credit requirements than conventional loans

FHA considerations:

- Requires mortgage insurance premium (MIP) for the life of the loan if you put down less than 10%

- Upfront MIP of 1.75% of the loan amount

- Properties must meet FHA appraisal standards

VA Loans: Zero Down for Veterans

If you’ve served in the military, VA loans offer unbeatable terms. These loans require no down payment, no private mortgage insurance (PMI), and typically feature lower interest rates than other programs[1].

2026 VA updates:

- Reduced funding fees saving buyers $1,200-$2,800 at closing[1]

- No maximum loan amount for qualified veterans

- More lenient credit requirements (typically 580-620 minimum)

Who qualifies:

- Active-duty service members

- Veterans with qualifying service

- Some surviving spouses

- National Guard and Reserve members who meet service requirements

USDA Loans: Zero Down for Rural and Suburban Buyers

USDA loans provide 100% financing for eligible properties in rural and suburban areas. The 2026 income limits expanded across almost all eligible areas, meaning more middle-income families now qualify[1].

USDA requirements:

- Property must be in an eligible rural area (check USDA’s online map)

- Income cannot exceed 115% of area median income

- Must be your primary residence

- Credit score typically 640+ required

Real-world example: A family earning $95,000 annually might have been over the income limit in 2025 but now qualifies in 2026 due to expanded thresholds. In fact, 62% of buyers who thought they earned too much still qualified under the new limits[1].

Conventional Loans: Best for Strong Credit

Conventional loans work well for buyers with credit scores of 620-640+ and stable income. Programs like HomeReady and Home Possible allow down payments as low as 3%, though income caps apply[1].

When to choose conventional:

- Credit score above 680 (for best rates)

- Can afford 5-20% down payment

- Stable employment history

- Want to avoid upfront mortgage insurance

Conventional advantages:

- PMI drops off once you reach 20% equity

- More property type flexibility

- Higher loan limits in expensive areas

| Loan Type | Min. Credit Score | Min. Down Payment | Income Limits | PMI/MIP Required |

|---|---|---|---|---|

| FHA | 580 | 3.5% | None | Yes (for life if <10% down) |

| VA | ~580-620 | 0% | None | No |

| USDA | ~640 | 0% | 115% of area median | Yes (annual fee) |

| Conventional | 620-640 | 3% | Varies by program | Yes (until 20% equity) |

Managing your budget during this process is crucial. Our Dave Ramsey budget percentages guide can help you determine how much house you can truly afford.

How Much Money Do I Actually Need to Buy My First Home?

You’ll need money for three main categories: down payment (0-20% of purchase price), closing costs (2-5% of loan amount), and cash reserves (1-3 months of mortgage payments). The exact amount depends on your loan type, purchase price, and lender requirements.

Breaking Down the Costs

Down Payment Options:

- FHA: 3.5% with 580+ credit score

- VA: 0% for qualified veterans

- USDA: 0% for eligible rural properties

- Conventional: 3-20% (5% typical for first-timers)

Example: On a $300,000 home:

- FHA down payment: $10,500

- Conventional 5% down: $15,000

- VA/USDA: $0

Closing Costs Include:

- Loan origination fees (0.5-1% of loan amount)

- Appraisal ($400-$600)

- Home inspection ($300-$500)

- Title insurance ($1,000-$2,000)

- Attorney fees (varies by state)

- Prepaid property taxes and insurance

- Recording fees

Total closing costs typically run 2-5% of your loan amount, or $6,000-$15,000 on a $300,000 purchase.

Cash Reserves:

Most lenders want to see 1-3 months of mortgage payments in savings after closing. This proves you can handle unexpected expenses or temporary income disruptions.

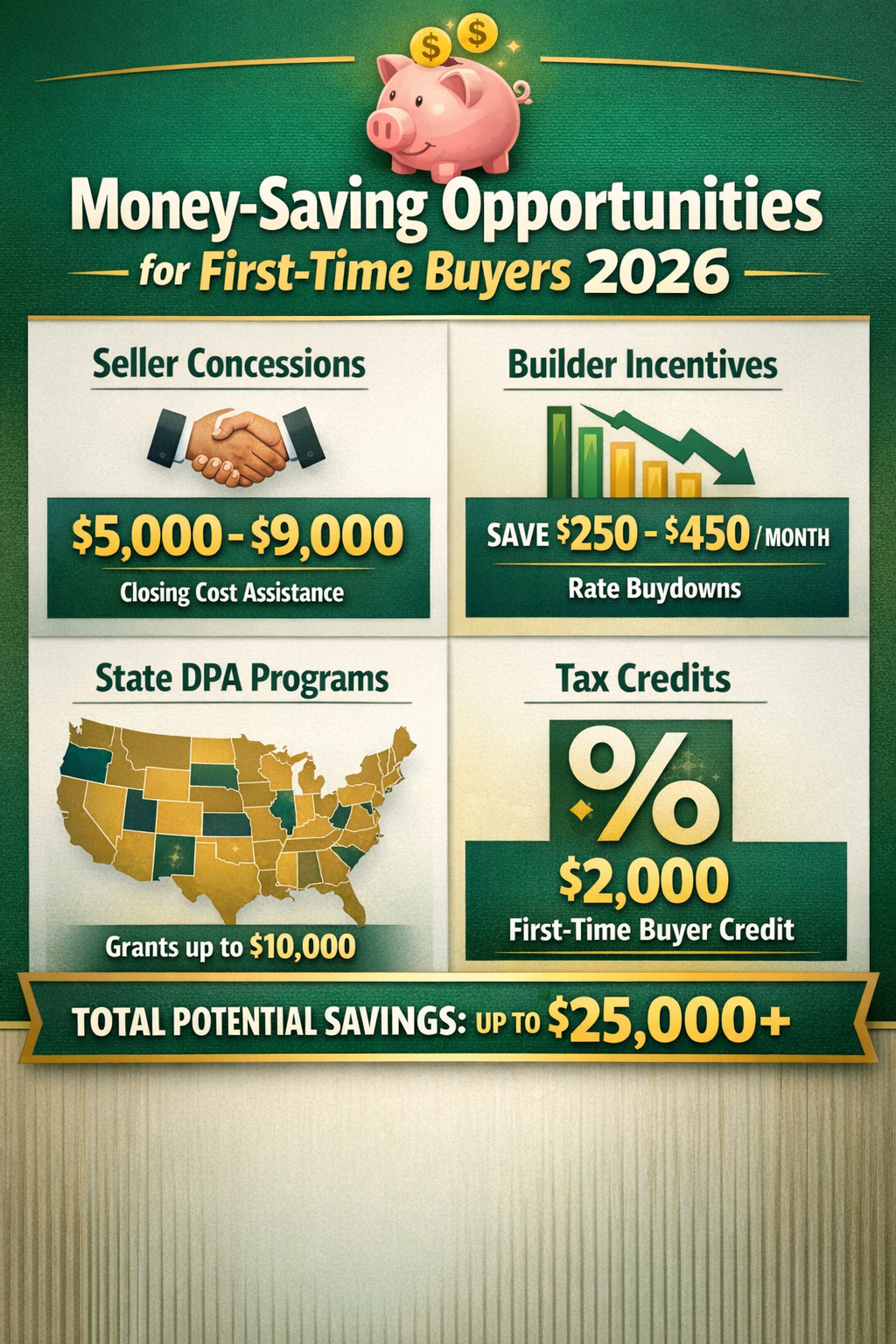

Money-Saving Strategies for 2026

Seller Concessions:

Winter months in 2026 are seeing typical seller concessions of $5,000-$9,000, which can cover a significant portion of your closing costs[1].

Builder Incentives:

New construction buyers are getting:

- Temporary rate buydowns saving $250-$450/month[1]

- Permanent rate reductions of 0.25-0.75%[1]

- Free upgrades valued at $3,000-$7,000[1]

State Down Payment Assistance:

Many states offer grants or low-interest loans for down payments. Florida’s Hometown Heroes Program, for example, provides up to $35,000 in assistance for nurses, teachers, law enforcement, and other essential workers[1].

Choose this approach if: You’re a first-time buyer in a qualifying profession or buying in a state with robust DPA programs.

Need to save more before buying? Our guide to saving $10,000 offers practical strategies that actually work.

What’s the Step-by-Step Process From Pre-Approval to Closing?

The home buying process follows seven distinct phases over 30-60 days: pre-approval (3-5 days), house hunting (varies), offer submission (1-2 days), home inspection (7-10 days), appraisal (7-14 days), underwriting (2-3 weeks), and closing (1 day). Each phase has specific requirements and potential roadblocks.

Phase 1: Get Pre-Approved (3-5 Days)

Submit your financial documents to a lender and receive a pre-approval letter. This step was covered in detail earlier but bears repeating—don’t skip this.

Phase 2: House Hunting (Timeline Varies)

Armed with your pre-approval, start touring homes within your budget. Work with a buyer’s agent (their commission is typically paid by the seller, so this costs you nothing).

Smart house hunting tips:

- Focus on homes priced 5-10% below your pre-approval amount to leave room for bidding

- Visit neighborhoods at different times of day

- Check school ratings even if you don’t have kids (affects resale value)

- Research property tax rates and HOA fees

Phase 3: Make an Offer (1-2 Days)

When you find “the one,” your agent helps you submit a written offer that includes:

- Purchase price

- Earnest money deposit (typically 1-3% of purchase price)

- Contingencies (inspection, appraisal, financing)

- Requested closing date

- Any requests for seller concessions

Negotiation reality: Properties in winter 2026 are averaging 1.8% below list price[1], giving buyers more negotiating power than in previous years.

Phase 4: Home Inspection (7-10 Days)

Once your offer is accepted, hire a professional inspector to examine the property. This typically costs $300-$500 but can save you thousands by identifying problems before you commit.

What inspectors check:

- Foundation and structural integrity

- Roof condition and age

- HVAC systems

- Plumbing and electrical

- Pest damage

- Water damage or mold

If major issues surface, you can negotiate repairs, request a price reduction, or walk away (if you included an inspection contingency).

Phase 5: Appraisal (7-14 Days)

Your lender orders an appraisal to confirm the home’s value supports the loan amount. The appraisal costs $400-$600 and protects both you and the lender from overpaying.

Common issue: If the appraisal comes in below your offer price, you’ll need to either negotiate a lower price, bring extra cash to closing to cover the gap, or walk away.

Phase 6: Underwriting (2-3 Weeks)

The underwriter reviews all your financial documents, the appraisal, and the title report to make a final lending decision. They may request additional documentation during this phase.

What triggers underwriting delays:

- Job changes during the process

- Large deposits or withdrawals from bank accounts

- New credit inquiries or debt

- Discrepancies in documentation

Critical rule: Don’t make any major financial changes between pre-approval and closing—no new cars, credit cards, or job switches.

Phase 7: Closing Day (1 Day)

You’ll sign final paperwork, pay closing costs and down payment, and receive the keys to your new home. Bring a cashier’s check or arrange a wire transfer for the exact amount specified on your Closing Disclosure (received 3 days before closing).

Final walkthrough: Schedule this 24 hours before closing to verify agreed-upon repairs were completed and the property is in the expected condition.

How Can I Improve My Chances of Loan Approval?

Boost your approval odds by raising your credit score above 640, reducing your debt-to-income ratio below 43%, maintaining steady employment for at least 2 years, and saving 3-6 months of expenses beyond your down payment and closing costs. These four factors carry the most weight in lending decisions.

Credit Score Optimization

Quick wins for credit improvement:

- Pay down credit card balances below 30% of limits (ideally below 10%)

- Dispute any errors on your credit reports

- Become an authorized user on a family member’s established card

- Don’t close old credit cards (length of credit history matters)

- Avoid new credit applications for 6 months before applying

Timeline: Most credit improvements take 3-6 months to fully reflect in your score. Start early.

For detailed strategies, check out our comprehensive guide on proven ways to raise your credit score fast.

Debt-to-Income Ratio Management

Your DTI compares monthly debt payments to gross monthly income. Most lenders prefer 43% or lower, though FHA allows up to 56.9%[2][4].

Calculate your DTI:

- Add up all monthly debt payments (student loans, car payments, credit cards, proposed mortgage)

- Divide by gross monthly income

- Multiply by 100 for percentage

Example: $2,500 in monthly debts ÷ $6,000 gross income = 41.7% DTI

How to lower DTI:

- Pay off small debts completely

- Increase income through side hustles (must be documented for 2 years)

- Choose a less expensive home

- Make a larger down payment to reduce monthly mortgage payment

Looking for ways to increase income? Our high-income skills guide shows realistic paths to earning more.

Employment Stability

Lenders typically require 2 years of employment history, preferably in the same field. Job hopping raises red flags about income stability.

If you’re self-employed:

- Expect to provide 2 years of tax returns

- Your qualifying income is typically the average of those 2 years

- Business owners may need additional documentation (profit/loss statements, business tax returns)

- Some lenders require 3 years of self-employment history

Cash Reserves

Beyond down payment and closing costs, lenders like seeing 1-3 months of mortgage payments in savings. This demonstrates financial cushion for emergencies.

Acceptable reserve sources:

- Checking and savings accounts

- Retirement accounts (though withdrawing may trigger penalties)

- Stocks and bonds

- Cash value of life insurance

Not acceptable:

- Borrowed money

- Unsecured loans

- Recent large deposits without clear documentation

If you need to build savings quickly, our 30-day saving challenge provides a structured approach.

What Are the Biggest Mistakes First-Time Buyers Make With Loans?

The three costliest mistakes are: shopping for homes before getting pre-approved (wastes time and weakens offers), making major financial changes during underwriting (can kill your loan), and focusing only on monthly payment instead of total loan cost (leads to choosing expensive loan products). Avoid these and you’ll sidestep 90% of first-timer problems.

Mistake #1: Skipping Pre-Approval

Why it’s costly: You waste weekends touring homes you can’t afford, and sellers don’t take your offers seriously without proof of financing.

The fix: Get pre-approved before your first showing. Period.

Mistake #2: Maxing Out Your Budget

Just because you’re approved for $400,000 doesn’t mean you should spend $400,000. Lenders qualify you based on ratios, not your actual lifestyle expenses.

Reality check: Your pre-approval doesn’t account for:

- Furniture and moving costs

- Home maintenance (budget 1-2% of home value annually)

- Utilities (often higher than renting)

- HOA fees

- Property tax increases

- Lifestyle expenses you’re not willing to cut

Better approach: Aim for a mortgage payment that’s 25-28% of your gross income, leaving room for savings, retirement, and life.

Our family budget guide helps you determine what you can actually afford, not just what lenders will approve.

Mistake #3: Ignoring Total Interest Costs

A lower monthly payment isn’t always better if it comes from stretching the loan term or accepting a higher interest rate.

Example comparison on $300,000 loan:

- 30-year at 7%: $1,996/month, $418,527 total interest

- 15-year at 6.5%: $2,613/month, $170,340 total interest

The 15-year costs $617 more monthly but saves $248,187 in interest. If you can afford the higher payment, the savings are massive.

Mistake #4: Making Financial Changes During Underwriting

Don’t do these things between pre-approval and closing:

- Switch jobs

- Finance a car

- Open new credit cards

- Make large purchases on credit

- Move money between accounts without documentation

- Co-sign loans for others

Why it matters: Underwriters verify your employment and credit right before closing. Changes can delay or kill your loan.

Mistake #5: Skipping the Home Inspection

Trying to save $400 on an inspection can cost you $40,000 in unexpected repairs. Always get a professional inspection, even on new construction.

What inspections miss: Inspectors can’t see inside walls or underground. Consider additional specialized inspections for:

- Sewer lines (especially on older homes)

- Radon testing

- Pest inspection

- Mold testing (if you notice musty smells)

Mistake #6: Draining All Savings for Down Payment

Putting every dollar into your down payment leaves you vulnerable to immediate expenses like:

- Moving costs

- Immediate repairs

- Furniture

- Appliances

- Lawn equipment

- Emergency fund depletion

Smart approach: Keep 3-6 months of expenses in savings after closing, even if it means making a smaller down payment and paying PMI temporarily.

For more financial pitfalls to avoid, read our guide on money mistakes costing you thousands.

How Do I Choose the Right Lender and Get the Best Rate?

Compare at least three lenders by requesting Loan Estimates for the same loan amount and type, then evaluate based on interest rate, closing costs, lender fees, and customer service quality. A 0.5% rate difference on a $300,000 loan costs you $30,000+ over 30 years, so shopping around matters.

Types of Lenders

Banks: Traditional institutions offering competitive rates for existing customers. Often slower processing but stable and regulated.

Credit Unions: Member-owned institutions typically offering lower rates and fees. Require membership but often have lenient qualification criteria.

Mortgage Brokers: Work with multiple lenders to find you the best deal. They earn commissions but can save you time and potentially money.

Online Lenders: Fast processing, competitive rates, and convenient digital applications. Less hand-holding but efficient for straightforward situations.

What to Compare

Request a Loan Estimate (LE) from each lender within the same 2-week period (multiple mortgage inquiries in this window count as one credit pull).

Key numbers on the Loan Estimate:

- Interest rate: The percentage charged on the loan principal

- APR (Annual Percentage Rate): Includes interest plus fees, giving you the true cost

- Loan amount: Should be identical across all estimates

- Closing costs: Section C shows lender fees you can negotiate

- Monthly payment: Principal, interest, taxes, insurance

Red flags:

- Lender fees exceeding 1% of loan amount

- Pressure to lock rates before you’re ready

- Unwillingness to explain fees

- Drastically different APR from interest rate (indicates high fees)

Rate Lock Strategy

Interest rates fluctuate daily. A rate lock guarantees your rate for 30-60 days while you complete the purchase.

When to lock:

- After your offer is accepted

- When rates are favorable and trending upward

- When you’re confident you can close within the lock period

Rate lock costs: Most lenders offer 30-day locks free, with fees for longer periods (typically 0.125-0.25% per additional 15 days).

Negotiation Tactics

Yes, you can negotiate:

- Origination fees

- Processing fees

- Underwriting fees

- Application fees

What you can’t negotiate:

- Third-party fees (appraisal, title, recording)

- Government fees

- Prepaid items (taxes, insurance)

Leverage: “Lender A offered me the same rate with $800 less in fees. Can you match that?”

Questions to Ask Every Lender

- What’s your average time to close?

- Who will be my main point of contact?

- What happens if rates drop before closing?

- Are there prepayment penalties?

- What’s included in your rate lock?

- How long have you been originating loans?

Choose the lender offering: Competitive rates, transparent fees, responsive communication, and a track record of closing on time.

Frequently Asked Questions About This Homebuyer’s Loan Guide

How long does the entire home buying process take?

From pre-approval to closing typically takes 30-60 days, though house hunting time varies widely. Pre-approval takes 3-5 days, finding a home can take weeks to months, and closing (after offer acceptance) runs 30-45 days on average.

Can I buy a house with bad credit?

Yes, FHA loans accept credit scores as low as 500 (with 10% down) or 580 (with 3.5% down)[2]. However, you’ll get better rates with scores above 640. Consider improving your credit before applying if you have time.

How much income do I need to buy a house?

Most lenders want your total monthly debts (including the new mortgage) to stay below 43-50% of gross income, though FHA allows up to 56.9%[2][4]. On a $300,000 home with 5% down, you’d need roughly $65,000-$75,000 annual income, depending on other debts.

Should I use a buyer’s agent?

Yes, buyer’s agents typically cost you nothing (seller pays their commission), provide expertise in negotiations, and help navigate paperwork. They also know which homes have issues or have been on the market too long.

What if the appraisal comes in low?

You have four options: negotiate a lower purchase price, bring extra cash to cover the gap, request a second appraisal if you believe the first was wrong, or walk away using your appraisal contingency.

Can I use gift money for my down payment?

Yes, most loan programs allow gift funds from family members. You’ll need a gift letter stating the money doesn’t need to be repaid, and documentation showing the transfer. Some programs require you to contribute a minimum percentage from your own funds.

What’s the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate based on self-reported information, while pre-approval involves verification of your credit, income, and assets. Pre-approval carries significantly more weight with sellers.

Should I pay points to lower my interest rate?

Paying points (1 point = 1% of loan amount) to reduce your rate makes sense if you’ll keep the loan long enough to recoup the cost. Calculate your break-even point: if you pay $3,000 for points that save you $100/month, you break even after 30 months.

Can I buy a house while paying off student loans?

Yes, but student loan payments count toward your debt-to-income ratio. If your loans are in deferment, lenders typically calculate 1% of the balance as a monthly payment for DTI purposes. Paying down student debt can improve your qualification. Our student loan payoff guide offers strategies.

What happens if I lose my job during the buying process?

Lenders verify employment right before closing. Job loss typically kills the loan unless you immediately secure comparable employment. This is why maintaining employment stability during the process is critical.

Are closing costs tax-deductible?

Some closing costs are deductible (points paid, prepaid property taxes, prepaid mortgage interest), while others aren’t (appraisal, inspection, title fees). Consult a tax professional for your specific situation.

How soon can I refinance after buying?

Most lenders require 6-12 months of payment history before refinancing, though some allow it sooner. Refinancing makes sense when rates drop at least 0.75-1% below your current rate or when you want to eliminate PMI.

Conclusion: Your Path to Homeownership Starts Now

Getting from “I want to buy a house” to holding keys in your hand doesn’t require a finance degree or perfect credit. This Homebuyer’s Loan Guide showed you the exact steps: get pre-approved with verified financial documents, choose the right loan program for your situation (FHA, VA, USDA, or conventional), save for down payment and closing costs, find a home within your true budget (not just your pre-approval amount), complete inspections and appraisal, survive underwriting without making financial changes, and close on your new home.

The 2026 market offers real advantages for first-time buyers. Loan limits increased significantly, giving you $20,000-$40,000 more purchasing power than last year[1]. VA funding fees dropped, saving qualified veterans $1,200-$2,800[1]. USDA income limits expanded, opening zero-down financing to more middle-income families[1]. Winter buying conditions are delivering seller concessions of $5,000-$9,000 and properties priced 1.8% below list[1].

Your next steps:

- This week: Pull your credit reports from all three bureaus and check for errors

- This month: Gather financial documents (tax returns, pay stubs, bank statements) and get pre-approved with at least three lenders

- Next 30 days: Research first-time buyer programs in your state and interview buyer’s agents

- Next 60 days: Start house hunting with your pre-approval in hand

Remember, the biggest mistake is waiting for “perfect” conditions. Rates, prices, and programs constantly change. The best time to buy is when you’re financially ready, regardless of market predictions.

Building the financial foundation for homeownership takes discipline. Our guide to achieving financial freedom provides the framework for long-term success beyond just buying a house.

You’ve got this. Thousands of first-time buyers navigate this process successfully every month, and you’re now armed with the knowledge to join them. Start with pre-approval, stay organized, avoid the common mistakes outlined in this guide, and you’ll be turning that key in your own front door before you know it.

Key Takeaways

- Pre-approval is mandatory before house hunting—it takes 3-5 days and requires credit reports, income verification, and bank statements

- FHA loans accept credit scores as low as 580 with 3.5% down, making them the most accessible option for first-time buyers with limited savings

- VA loans offer zero-down financing with no PMI for qualified veterans, with 2026 funding fees reduced by $1,200-$2,800

- USDA loans provide 100% financing for eligible rural and suburban properties, with expanded 2026 income limits opening eligibility to more families

- Conventional loans work best for buyers with 620+ credit scores and 3-20% down payment, with PMI dropping off at 20% equity

- Total costs include down payment (0-20%), closing costs (2-5% of loan amount), and cash reserves (1-3 months of payments)

- The buying process takes 30-60 days from offer to closing, with underwriting being the most document-intensive phase

- Never make major financial changes (job switches, new credit, large purchases) between pre-approval and closing

- Compare at least three lenders using Loan Estimates to find the best combination of rate, fees, and service

- 2026 loan limits increased significantly, giving buyers $20,000-$40,000 more purchasing power than 2025

References

[1] First Time Home Buyers Programme In The Us – https://www.realpha.com/blog/first-time-home-buyers-programme-in-the-us

[2] Watch – https://www.youtube.com/watch?v=aOfhgnHjiAo

[3] Understanding The New Conforming Loan Limits For 2026 – https://www.thefederalsavingsbank.com/Blog/understanding-the-new-conforming-loan-limits-for-2026/

[4] Firsttime Home Buyer Programs In Everything You Need To Know – https://www.amerisave.com/learn/firsttime-home-buyer-programs-in-everything-you-need-to-know

![How I Paid Off $50,000 in Debt: My Step-by-Step Debt Free Journey Last updated: March 31, 2026 Quick Answer: Paying off $50,000 in debt is absolutely possible, even on an average income. I did it by getting brutally honest about my numbers, choosing a payoff method that fit my personality, cutting expenses aggressively, and adding extra income streams. It took focus and sacrifice, but the process is straightforward: list every debt, build a small emergency fund, attack debt with every spare dollar, and protect your progress along the way. Key Takeaways Know your exact numbers first. You can't pay off what you haven't fully faced. List every balance, interest rate, and minimum payment. The debt snowball and debt avalanche are the two main payoff methods. Snowball wins on motivation; avalanche wins on math. A small $1,000 emergency fund before you start keeps unexpected expenses from derailing your plan. Cutting expenses alone usually isn't enough. Adding income — even a few hundred dollars a month — dramatically speeds up your debt free journey. 74% of Americans now define financial success as being debt-free, according to KeyBank's 2025 Financial Mobility Survey. You're not alone in this goal. [2] Automate your payments. Willpower runs out; automation doesn't. Celebrate small wins. Each paid-off account is real progress, not just a number. Debt stress is real. Building a support system or accountability partner makes a measurable difference in staying consistent. Once debt-free, redirect those payments immediately toward savings and investing so you never slide back. What Does a Debt Free Journey Actually Look Like? A debt free journey is the intentional, step-by-step process of eliminating all personal debt — credit cards, car loans, student loans, medical bills — until you owe nothing. It's not a single moment; it's a series of decisions made consistently over months or years. For me, it started with a number that made my stomach drop: $50,247.13. That was the total across four credit cards, a car loan, and leftover student loan debt. I had been making minimum payments for years, watching the balances barely move. When I finally sat down and added it all up, I realized I had been treading water. According to a 2026 survey by Southwest Voices, 33% of U.S. consumers define financial success as being debt-free, regardless of income or assets — a shift away from the old idea that wealth is measured by what you own. [1] That reframing helped me. I stopped feeling behind and started feeling motivated. Here's the honest truth: a debt free journey looks messy in the middle. There are months where you feel unstoppable and months where an unexpected car repair wipes out your progress. What matters is that you keep going. Step 1: Face the Full Picture (This Part Is Uncomfortable) Before you can make a plan, you need complete, accurate information about every debt you owe. Here's exactly what I tracked in a simple spreadsheet: Debt Balance Interest Rate Minimum Payment Credit Card A $8,400 24.99% APR $210 Credit Card B $6,100 19.99% APR $155 Credit Card C $3,200 22.49% APR $80 Car Loan $14,500 6.9% APR $320 Student Loan $18,047 5.5% APR $195 Total $50,247 — $960/month Looking at that table was hard. But it was also the most important thing I did, because it turned a vague, overwhelming cloud of "I have a lot of debt" into a concrete list I could actually work through. Common mistake: Many people underestimate their total debt because they avoid checking balances. Log in to every account, pull your free credit report at AnnualCreditReport.com, and write down every number. Step 2: Build a Small Emergency Fund First Before throwing every extra dollar at debt, save $1,000 as a starter emergency fund. This sounds counterintuitive when you're paying 24.99% interest, but here's why it works: without a cash cushion, the first flat tire or medical co-pay goes right back on a credit card, undoing your progress and crushing your motivation. A 2025 KeyBank survey found that 25% of Americans cannot come up with $2,000 for unexpected expenses, up from 19% the year before. [2] That statistic shows how common this vulnerability is — and why plugging it first protects your entire plan. Once you hit $1,000, stop saving and redirect everything to debt. You can build a full 3–6 month emergency fund after you're debt-free. Step 3: Choose Your Debt Payoff Strategy Two methods dominate personal finance, and both work. The right one depends on your personality. Debt Snowball (Dave Ramsey's method): Pay minimums on all debts. Throw every extra dollar at the smallest balance first. When it's gone, roll that payment to the next smallest. Best for: people who need quick wins to stay motivated. Debt Avalanche: Pay minimums on all debts. Throw every extra dollar at the highest interest rate first. Best for: people who are motivated by math and want to pay the least interest overall. I used the snowball method because I needed to feel progress. Paying off that $3,200 credit card in four months gave me a surge of confidence that kept me going for the next two years. If you want a detailed breakdown of both approaches, check out this guide on 7 proven ways to pay down debt faster. Edge case: If you have a debt with a balance transfer offer at 0% APR, consider moving high-interest credit card balances there first. Harvard FCU recommends balance transfer cards as a way to freeze interest accrual and focus entirely on paying down principal. [5] Just watch for transfer fees (typically 3–5%) and make sure you can pay the balance before the promotional period ends. Step 4: Cut Expenses Without Losing Your Mind Cutting expenses is where most people start — and where many people quit, because they try to cut everything at once and feel deprived. My approach: cut in tiers. Tier 1 — Cut immediately (no lifestyle impact): Unused subscriptions and memberships Negotiated lower rates on phone, internet, and insurance Switched to generic/store-brand groceries Tier 2 — Reduce (some adjustment required): Eating out dropped from 4x/week to once a week Grocery budget planned with a weekly meal plan (I saved roughly $200/month here) Paused gym membership and worked out at home Tier 3 — Temporary sacrifices (hard but worth it): Skipped vacations for 18 months Sold my newer car and bought a paid-off used car, eliminating the $320/month payment A 2025 KeyBank survey found that 49% of consumers switched to less expensive brands or services and 41% reduced subscriptions or memberships in response to rising costs. [2] These aren't dramatic moves — they're practical ones that add up fast. For practical grocery savings, this budget meal planning guide shows how to feed a family on $50/week, which is a real game-changer when you're redirecting every dollar to debt. Step 5: Increase Your Income (This Is the Real Accelerator) Cutting expenses has a floor — you can only cut so much. Income has no ceiling. Adding even $300–$500 per month in extra income can cut months or years off your debt free journey. What I did to earn extra money: Sold stuff I didn't need. I made over $1,000 in 30 days selling furniture, clothes, and electronics. (This decluttering guide shows exactly how.) Freelanced on weekends. I offered writing and editing services through Upwork for about 8 hours per week. Used money-making apps. Small amounts — $50–$100/month — but every dollar went straight to debt. Every single dollar of extra income went directly to the target debt. Not to lifestyle upgrades. Not to "treating myself." Straight to the balance. If you're looking for ways to earn more without a second job, check out these 15 best money making apps that pay real cash or explore high income skills you can learn at home that can significantly boost your monthly income over time. How Do You Stay Motivated During a Long Debt Free Journey? Staying motivated over a multi-year debt payoff is genuinely the hardest part. The math is simple; the psychology is not. 38% of U.S. women report that money makes them feel anxious most of the time, compared to 24% of men, according to a 2026 Southwest Voices survey. [1] Debt stress is real, and ignoring it doesn't make it go away. What actually helped me stay on track: A visual debt payoff tracker. I colored in a bar graph on my fridge every time I paid off $1,000. Silly? Maybe. Effective? Absolutely. An accountability partner. My sister was on her own debt free journey. We checked in monthly. Celebrating milestones. When I paid off each account, I did something small and free to mark it — a picnic, a movie night at home. Reading stories like mine. Seeing that a debt-free family paid off $67K on one income made my $50K feel conquerable. If you're feeling overwhelmed, this resource on debt stress relief and staying motivated has practical strategies that go beyond "just believe in yourself." Decision rule: If you're losing motivation, don't restart from scratch. Switch strategies temporarily. If you've been doing the avalanche method, switch to snowball for one month to get a quick win. Then go back. What Was My Month-by-Month Debt Payoff Timeline? Here's an honest look at how the $50,247 came down over 26 months. I'm sharing this because most debt payoff stories skip the messy middle. Month Range Action Running Balance Months 1–2 Built $1,000 emergency fund $50,247 Months 3–6 Paid off Credit Card C ($3,200) $47,047 Months 7–11 Paid off Credit Card B ($6,100) $40,947 Months 12–16 Paid off Credit Card A ($8,400) $32,547 Month 17 Sold car, eliminated car loan $18,047 Months 18–26 Paid off student loan $0 Month 17 was the turning point. Selling the car felt terrifying, but it eliminated $14,500 in debt overnight and freed up $320/month. After that, the student loan felt manageable. Note on the car: I bought a $5,000 used Honda Civic with cash. It wasn't glamorous, but it ran fine and I drove it for two years while I finished paying off everything else. What Mistakes Almost Derailed My Debt Free Journey? Knowing what to avoid is just as important as knowing what to do. Mistake 1: Not having an emergency fund first.Early on, I skipped the $1,000 buffer and put everything at debt. Three months in, a $700 car repair went right back on a credit card. Demoralizing. Mistake 2: Setting an unrealistic budget.My first budget was so tight I lasted two weeks before blowing it. I had to build in a small "fun money" line — even $30/month — to make the budget sustainable. Mistake 3: Ignoring the emotional side.I white-knuckled it for the first six months without any support system. Burnout hit hard. Once I found an accountability partner and started tracking wins visually, consistency improved dramatically. Mistake 4: Lifestyle creep after early wins.After paying off the first credit card, I celebrated by spending more than I should have for a couple of months. I lost about six weeks of progress. Celebrate, but keep the momentum. To avoid common budgeting pitfalls, this list of 10 budgeting mistakes to avoid is worth reading before you build your plan. What Happens After You Become Debt-Free? Becoming debt-free is not the finish line — it's the starting line for building actual wealth. 38% of people say being debt-free is the most important financial milestone, according to the 2026 BHG Financial Consumer Debt & Finances Survey. [4] But once you're there, the same discipline that paid off debt becomes your wealth-building engine. Here's what I did the month I made my last payment: Built a full 3–6 month emergency fund using what used to be my debt payments. Started investing — maxed out my Roth IRA contribution for the year. Kept living on my "debt payoff budget" for six more months to build a real financial cushion. Raised my credit score — paying off revolving debt dramatically improved my utilization ratio. 74% of respondents in the BHG Financial survey feel optimistic about their financial future, with that number climbing to 80% among higher-income households. [4] I felt that shift personally. Once the debt was gone, financial decisions stopped feeling like damage control and started feeling like choices. For the next chapter, this guide on how to achieve financial freedom in 5 steps is exactly where I'd point anyone who just made their last debt payment. Frequently Asked Questions Q: How long does it realistically take to pay off $50,000 in debt?A: It depends on your income, expenses, and how aggressively you can pay. With focused effort — cutting expenses and adding income — most people can pay off $50,000 in 2–4 years. I did it in 26 months by combining both strategies. Q: Should I save money or pay off debt first?A: Build a small $1,000 emergency fund first, then attack debt aggressively. Without that buffer, unexpected expenses will send you back to credit cards and undo your progress. Q: What's the best method for paying off debt — snowball or avalanche?A: Both work. Snowball (smallest balance first) is better if you need motivational wins to stay consistent. Avalanche (highest interest first) saves more money mathematically. Choose the one you'll actually stick to. Q: Can I pay off debt on a low income?A: Yes, but it requires more focus on increasing income alongside cutting expenses. Even an extra $200–$300/month makes a significant difference over time. This guide on how to pay off credit card debt fast on a low income has specific strategies for tighter budgets. Q: Should I use a balance transfer card to pay off debt faster?A: A 0% APR balance transfer card can be a smart move for high-interest credit card debt, because it stops interest from accruing and lets you focus entirely on the principal. [5] Watch for transfer fees and make sure you have a plan to pay it off before the promotional period ends. Q: What if I have an emergency and go back into debt during my payoff journey?A: It happens. Don't quit. Rebuild your $1,000 buffer, then resume your payoff plan. One setback doesn't erase your progress. Q: Is a no-spend challenge worth trying during debt payoff?A: Absolutely. A no-spend month challenge can generate an extra $200–$500 in a single month, which goes directly to your target debt. It also resets spending habits in a lasting way. Q: How do I stay motivated when debt payoff feels like it's taking forever?A: Use a visual tracker, find an accountability partner, and celebrate each paid-off account. Also, recalculate your payoff date every few months — watching it move closer is genuinely motivating. Q: Will paying off debt hurt my credit score?A: Paying off installment loans (like a car or student loan) can cause a small, temporary dip because it reduces your credit mix. But paying off credit cards improves your utilization ratio, which typically raises your score. The net effect of becoming debt-free is almost always positive over time. Q: What's the first step if I'm completely overwhelmed and don't know where to start?A: Write down every debt you owe — balance, interest rate, minimum payment — in one place. That single act of clarity is the foundation of every successful debt free journey. Conclusion: Your Debt Free Journey Starts With One Decision Paying off $50,000 in debt wasn't about being perfect. It was about being consistent. I made mistakes, had setbacks, and had months where I wanted to give up. But I kept coming back to the plan. Here's your action plan for this week: List every debt with its balance, interest rate, and minimum payment. Set up a $1,000 starter emergency fund before you do anything else. Choose your payoff method (snowball or avalanche) and commit to it. Find one expense to cut and one way to earn extra money this month. Tell someone — an accountability partner changes everything. If you're ready to go deeper, the debt free in 12 months step-by-step plan is a great next resource, and these 10 simple habits that help you stay debt-free for life will help you protect everything you build. You don't need a perfect plan. You need a real one. Start today. References [1] Debt Free Flexible And Focused On Stability The Money Mindset Of Us Consumers In 2026 - https://www.southwestvoices.news/premium/stacker/stories/debt-free-flexible-and-focused-on-stability-the-money-mindset-of-us-consumers-in-2026,150595 [2] Is Debt Free The New Luxury Keybank Survey Explores 302606087 - https://www.prnewswire.com/news-releases/is-debt-free-the-new-luxury-keybank-survey-explores-302606087.html [4] Money Map Report - https://bhgfinancial.com/research/money-map-report [5] Gift Yourself Financial Peace How Be Debt Free In 2026 - https://harvardfcu.org/blog/gift-yourself-financial-peace-how-be-debt-free-in-2026/ Meta Title: How I Paid Off $50,000 in Debt: My Debt Free Journey Meta Description: I paid off $50,000 in debt in 26 months. Here's my honest, step-by-step debt free journey — what worked, what failed, and how you can do it too. Tags: debt free journey, paying off debt, debt snowball, debt avalanche, debt payoff plan, personal finance, budgeting tips, credit card debt, student loan payoff, financial freedom, debt stress, money motivation](https://msbudget.com/wp-content/uploads/2026/03/slot-0-1774952346462-500x330.png)