I’ll never forget the night I sat at our kitchen table, surrounded by bills, tears streaming down my face as I realized we owed more than $67,000. With three kids under seven, a single income, and what felt like a mountain of debt crushing us, becoming a debt free family seemed impossible. But here’s the truth: three years later, we paid off every single penny. If you’re drowning in debt while raising kids on one income, I’m here to tell you that freedom is possible—and I’m going to show you exactly how we did it.

Key Takeaways

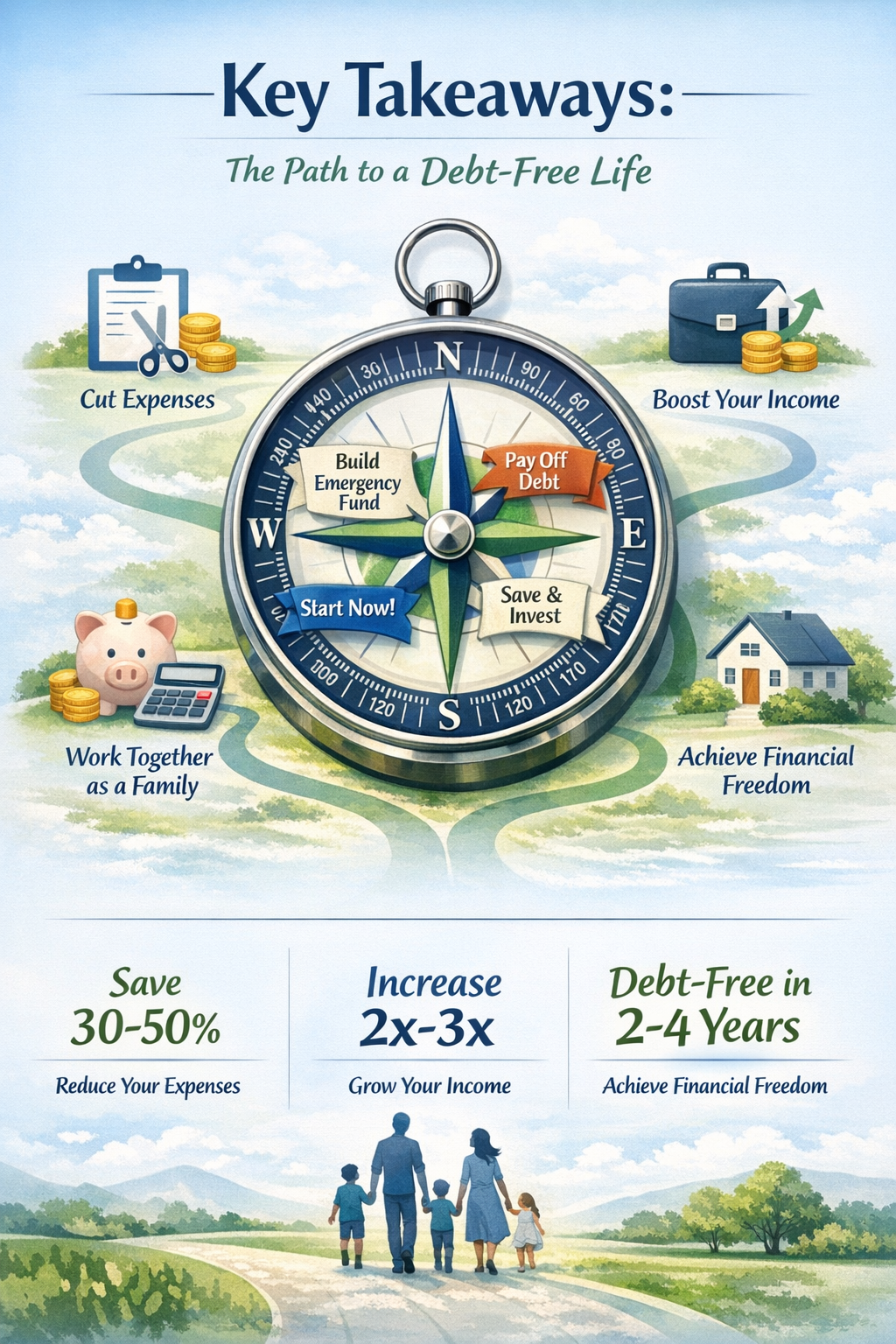

- Becoming a debt free family on one income is achievable with intentional budgeting, sacrifice, and a clear payoff strategy

- The debt snowball method combined with extreme frugality helped us eliminate $67,000 in 36 months

- Involving your kids in the journey teaches valuable money lessons and creates family unity around financial goals

- Cutting expenses ruthlessly while finding creative income sources accelerates debt payoff dramatically

- Building simple money habits ensures you stay debt-free long after the final payment

Our Debt-Free Family Story: Where It All Started 💔

Let me take you back to 2023. My husband had just started a new job after being laid off, and I had recently become a stay-at-home mom to our three beautiful children. We thought we were doing okay—until I actually sat down and added up all our debt.

Our debt breakdown looked like this:

| Debt Type | Amount | Interest Rate |

|---|---|---|

| Credit Cards | $23,400 | 18-24% |

| Car Loan | $18,600 | 6.5% |

| Student Loans | $21,000 | 5.2% |

| Medical Bills | $4,000 | 0% |

| Total | $67,000 | Varies |

On a single income of $52,000 per year, this felt insurmountable. We were living paycheck to paycheck, constantly stressed about money, and setting a terrible example for our kids. Something had to change.

The turning point came when our oldest asked why we couldn’t go on vacation like her friends. I realized our debt was stealing not just our money, but our family experiences and peace of mind. That night, I made a commitment: we would become a debt-free family, no matter what it took.

Step 1: Facing the Truth and Creating Our Debt-Free Family Plan 📊

The hardest part of any debt payoff journey is getting brutally honest about your situation. I spent an entire weekend gathering every statement, bill, and financial document we had. It was painful, but necessary.

Getting Crystal Clear on Our Numbers

First, I created a complete debt inventory. I wrote down:

- Every creditor’s name

- Total balance owed

- Minimum monthly payment

- Interest rate

- Due date

This simple act of facing our reality gave us power over our debt instead of letting it have power over us. I recommend using a step-by-step debt payoff plan to organize this process.

Choosing Our Payoff Strategy

After researching different methods, we chose the debt snowball approach. This meant listing our debts from smallest to largest and attacking the smallest first while making minimum payments on everything else.

Why? Because we needed quick wins. As a debt free family wannabe with three kids to feed and only one income, we needed motivation to keep going. Paying off that first $800 medical bill in two months gave us the momentum we desperately needed.

Setting Our Target Date

We calculated that with aggressive payments, we could be debt-free in three years. I circled December 31, 2026, on our calendar and wrote “FREEDOM DAY” in big red letters. That date became our family’s rallying cry.

Step 2: Slashing Our Budget to the Bone 🔪

Becoming a debt free family on one income meant we had to get serious about our spending. I’m talking extreme frugality that would make our friends think we’d lost our minds.

Our Grocery Budget Transformation

Our biggest expense after housing was food. We were spending nearly $900 a month feeding five people, eating out regularly, and wasting tons of food.

Here’s what we changed:

✅ Meal planning every single week – No more wandering the grocery store aimlessly

✅ Shopping with a strict list – If it wasn’t on the list, it didn’t go in the cart

✅ Cooking from scratch – Goodbye convenience foods, hello dried beans and rice

✅ Eliminating restaurants – We went from eating out 8 times a month to zero

✅ Using every leftover – “Leftover night” became a weekly tradition

We cut our grocery bill to $450 a month using frugal grocery strategies that actually work. That’s $450 extra per month toward debt—$5,400 per year!

Cutting the “Necessities” That Weren’t

We questioned everything. Did we really need cable? Nope. Did we need the latest phones? Absolutely not. Did we need a gym membership when we could exercise at home? You get the idea.

Our monthly cuts included:

- Cable TV: Saved $120/month

- Gym memberships: Saved $80/month

- Subscription boxes: Saved $45/month

- Premium phone plans: Saved $60/month (switched to prepaid)

- Reduced car insurance: Saved $35/month (shopped around)

- Cancelled streaming services: Saved $40/month (kept one, rotated)

Total monthly savings: $380

Annual savings: $4,560

Combined with grocery savings, we found nearly $10,000 per year just by cutting expenses. For a family trying to stop living paycheck to paycheck, this was life-changing.

Housing and Transportation Sacrifices

We seriously considered downsizing our home, but the moving costs and market conditions didn’t make sense. Instead, we:

- Rented out our spare bedroom to a college student ($400/month)

- Sold one car and became a one-car family (saved $280/month on payment, insurance, and gas)

- Kept the thermostat at 68°F in winter, 76°F in summer

These weren’t easy choices, especially with three kids. But every sacrifice brought us closer to becoming a debt free family.

Step 3: Increasing Our Income While Staying Home 💰

Cutting expenses only gets you so far. To really accelerate our debt payoff, I needed to find ways to earn money while still being home with our kids.

My Side Hustle Journey

As a stay-at-home mom, I had limited time, but I was determined. Here’s what worked:

Freelance Writing ($300-600/month)

I started writing articles during naptime and after the kids went to bed. It was exhausting, but that extra income made a huge difference.

Selling Items We No Longer Needed ($2,400 in year one)

We decluttered our entire house and sold everything from old toys to furniture we didn’t use. I made $1,000 in one month just by decluttering.

Online Surveys and Apps ($50-100/month)

While not huge money, every little bit helped. I used money-making apps during downtime.

Babysitting for Friends ($200/month)

Since I was already home with my kids, watching one or two more a few times a week was manageable and brought in cash.

My Husband’s Efforts

My husband also stepped up:

- Took on overtime whenever available

- Started a small lawn care business on weekends (seasonal)

- Sold his collectibles that had been gathering dust

Between both of us, we added roughly $800-1,200 per month in extra income during our most aggressive debt payoff phase.

Step 4: Involving Our Kids in the Debt-Free Family Mission 👨👩👧👦

One of the best decisions we made was being age-appropriately honest with our children about our financial situation and goals.

Teaching Moments

We didn’t burden them with adult stress, but we did explain:

- Why we were choosing different activities (free parks instead of expensive entertainment)

- How saving money helps our family

- The importance of being grateful for what we have

- How to distinguish between wants and needs

Our Debt-Free Chart

We created a giant thermometer chart on our refrigerator showing our progress toward zero debt. Every time we paid off a debt, the kids helped color in the chart. They celebrated with us!

Kid-Friendly Sacrifices

Our children learned to:

- Choose library books over bookstore purchases

- Enjoy homemade pizza nights instead of delivery

- Appreciate hand-me-downs and thrift store finds

- Save their own money for special wants

These lessons were priceless. Our kids developed financial literacy that will serve them their entire lives. They saw firsthand that becoming a debt free family requires teamwork and sacrifice.

Step 5: Staying Motivated Through the Tough Times 💪

Let me be real: there were moments when I wanted to quit. When the car broke down and needed $800 in repairs. When all three kids needed new shoes at the same time. When I was so tired of saying “no” to everything fun.

Our Motivation Strategies

Monthly Celebrations

Every time we paid off a debt, we had a small celebration—usually a homemade special dinner or a free family activity we loved.

Visual Reminders

Besides our refrigerator chart, I kept a photo of our family on my phone with “DEBT FREE 2026” as the caption. Every time I was tempted to overspend, I looked at it.

Community Support

I joined online debt-free communities where other families shared their journeys. Knowing we weren’t alone made a huge difference. Reading about staying motivated while dealing with debt stress helped during the hardest months.

Tracking Every Win

I kept a journal where I wrote down every payment, every milestone, every small victory. Looking back at how far we’d come kept us moving forward.

The Emergency Fund Buffer

One critical strategy: we paused our aggressive debt payoff to save a $1,000 emergency fund first. This prevented us from going further into debt when unexpected expenses hit. Once we had that buffer, we attacked debt with everything we had.

The Numbers: Our Three-Year Debt-Free Family Journey 📈

Here’s exactly how we paid off $67,000 in 36 months on one income:

Year One:

- Debt paid: $18,200

- Average monthly payment: $1,517

- Methods: Extreme budget cuts + side hustles + selling stuff

- Debts eliminated: All medical bills, 2 credit cards

Year Two:

- Debt paid: $22,800

- Average monthly payment: $1,900

- Methods: Continued frugality + increased side income + tax refund

- Debts eliminated: Remaining credit cards, car loan

Year Three:

- Debt paid: $26,000

- Average monthly payment: $2,167

- Methods: Snowball effect + bonus from husband’s work + final push

- Debts eliminated: All student loans

Our Income Breakdown

Primary income: $52,000/year ($4,333/month)

Side income average: $800/month

Total monthly income: $5,133

Our debt payment averaged: $1,794/month

Percentage of income to debt: 35%

We lived on roughly $3,300/month for a family of five, which included:

- Mortgage/rent

- Utilities

- Groceries

- Basic necessities

- Minimal entertainment

It was tight. Really tight. But we made it work by implementing proven strategies to pay down debt faster.

Life After Becoming a Debt-Free Family 🎉

On December 28, 2026 (three days ahead of schedule!), we made our final student loan payment. I literally cried tears of joy. Our kids made us a “Congratulations!” banner, and we had a family dance party in our living room.

What Changed Immediately

The most noticeable change was breathing room. That $1,800+ we’d been throwing at debt every month suddenly became available for:

- Building a real emergency fund (we’re now at 6 months of expenses)

- Saving for our kids’ education

- Planning a modest family vacation (our first in three years!)

- Starting to invest for retirement

The Habits That Stuck

Even though we’re debt-free, we’ve maintained many of the frugal habits that got us here:

- Meal planning and cooking from scratch

- Thoughtful spending on wants

- Living below our means

- Avoiding lifestyle inflation

These simple habits help us stay debt-free for life.

Our New Financial Goals

Now we’re focused on:

- Achieving complete financial freedom

- Building wealth for our family’s future

- Teaching our kids about money management

- Giving generously to causes we care about

Practical Tips for Your Debt-Free Family Journey 🎯

Based on our experience, here’s my best advice for families trying to become debt-free on one income:

Start Where You Are

Don’t wait for the “perfect” time. We weren’t in an ideal situation when we started, but we started anyway. Even if you can only put $50 extra toward debt this month, that’s $50 closer to freedom.

Get Your Spouse on Board

This only works if you’re united. My husband and I had to have some difficult conversations, but we committed to the goal together. If you’re struggling with money discussions, try a couples budgeting approach that reduces conflict.

Be Flexible But Committed

Life happens. Kids get sick. Cars break down. Appliances die. When setbacks occur, adjust your timeline but don’t abandon your goal.

Find Free Fun

We discovered so many free activities: library story times, community events, nature walks, free museum days, backyard camping. Your kids won’t remember expensive entertainment—they’ll remember time together.

Avoid These Common Mistakes

Based on what I learned, avoid these pitfalls:

- Don’t skip the emergency fund (even a small one)

- Don’t hide spending from your spouse

- Don’t deprive yourself so much you burn out

- Don’t compare your journey to others

- Don’t forget to celebrate small wins

For more guidance, check out common money mistakes to avoid that could derail your progress.

Consider Your Timeline Realistically

We chose three years, but your timeline might be different. Factors to consider:

- Total debt amount

- Income level

- Family size and expenses

- Geographic location (cost of living)

- Health considerations

Some families do it faster; some take longer. What matters is consistent progress, not perfection.

Resources That Helped Our Debt-Free Family Succeed 📚

Throughout our journey, certain tools and resources were invaluable:

Books That Changed Our Mindset

“Debt-Free Forever” by Gail Vaz-Oxlade became our debt payoff bible [1]. Her practical, no-nonsense approach resonated with us and provided actionable steps we could implement immediately.

Tracking Tools

We used:

- A simple Excel spreadsheet to track all debts

- A debt-free journal to document our journey [3]

- Free budgeting apps to monitor spending

- Cash envelopes for variable expenses

Online Communities

Connecting with other families on the same journey provided encouragement, accountability, and practical tips. YouTube channels featuring debt-free stories [2] kept us motivated during tough months.

Financial Education

We educated ourselves through:

- Personal finance blogs and podcasts

- Library books on money management [4]

- Free online courses on budgeting

- Debt payoff calculators to track progress

Your Debt-Free Family Action Plan: Start Today ✅

Ready to begin your own journey? Here’s your step-by-step action plan:

This Week:

- Gather all debt statements and create your complete debt inventory

- Calculate your total debt amount (yes, it’s scary, but necessary)

- Have an honest conversation with your spouse about your financial goals

- Choose your debt payoff method (snowball or avalanche)

This Month:

- Create a bare-bones budget focusing on needs vs. wants

- Identify 3-5 expenses you can cut immediately

- Set up automatic minimum payments on all debts

- Start your $1,000 emergency fund

- List items you can sell for quick cash

This Quarter:

- Establish a side hustle or additional income stream

- Make your first extra debt payment

- Create a visual tracker for your family

- Review and adjust your budget based on what’s working

- Celebrate your first small win

This Year:

- Pay off your first debt completely

- Build your emergency fund to one month of expenses

- Involve your kids in age-appropriate ways

- Reassess your timeline and adjust as needed

- Stay connected to your support community

Remember, becoming a debt free family isn’t about being perfect—it’s about making consistent progress toward freedom.

Conclusion: Your Debt-Free Family Future Awaits 🌟

Three years ago, I couldn’t imagine how we’d ever escape our $67,000 debt prison. Today, we’re completely debt-free, building wealth, and teaching our children financial principles that will change their lives.

If we could do it on one income with three kids, you can too. Will it be easy? Absolutely not. Will it require sacrifice? Yes. Will there be moments you want to quit? Definitely. But will it be worth it? Without a doubt.

The peace of mind that comes from being a debt free family is indescribable. No more anxiety about bills. No more fighting about money. No more feeling trapped by payments. Just freedom to build the life you actually want.

Your journey starts with a single decision: today is the day you commit to change. You don’t need perfect circumstances, unlimited income, or special knowledge. You just need determination, a plan, and the willingness to do hard things for a better future.

We’re cheering for you. Your debt-free family story is waiting to be written. Now go write it! 💪

![How I Paid Off $50,000 in Debt: My Step-by-Step Debt Free Journey Last updated: March 31, 2026 Quick Answer: Paying off $50,000 in debt is absolutely possible, even on an average income. I did it by getting brutally honest about my numbers, choosing a payoff method that fit my personality, cutting expenses aggressively, and adding extra income streams. It took focus and sacrifice, but the process is straightforward: list every debt, build a small emergency fund, attack debt with every spare dollar, and protect your progress along the way. Key Takeaways Know your exact numbers first. You can't pay off what you haven't fully faced. List every balance, interest rate, and minimum payment. The debt snowball and debt avalanche are the two main payoff methods. Snowball wins on motivation; avalanche wins on math. A small $1,000 emergency fund before you start keeps unexpected expenses from derailing your plan. Cutting expenses alone usually isn't enough. Adding income — even a few hundred dollars a month — dramatically speeds up your debt free journey. 74% of Americans now define financial success as being debt-free, according to KeyBank's 2025 Financial Mobility Survey. You're not alone in this goal. [2] Automate your payments. Willpower runs out; automation doesn't. Celebrate small wins. Each paid-off account is real progress, not just a number. Debt stress is real. Building a support system or accountability partner makes a measurable difference in staying consistent. Once debt-free, redirect those payments immediately toward savings and investing so you never slide back. What Does a Debt Free Journey Actually Look Like? A debt free journey is the intentional, step-by-step process of eliminating all personal debt — credit cards, car loans, student loans, medical bills — until you owe nothing. It's not a single moment; it's a series of decisions made consistently over months or years. For me, it started with a number that made my stomach drop: $50,247.13. That was the total across four credit cards, a car loan, and leftover student loan debt. I had been making minimum payments for years, watching the balances barely move. When I finally sat down and added it all up, I realized I had been treading water. According to a 2026 survey by Southwest Voices, 33% of U.S. consumers define financial success as being debt-free, regardless of income or assets — a shift away from the old idea that wealth is measured by what you own. [1] That reframing helped me. I stopped feeling behind and started feeling motivated. Here's the honest truth: a debt free journey looks messy in the middle. There are months where you feel unstoppable and months where an unexpected car repair wipes out your progress. What matters is that you keep going. Step 1: Face the Full Picture (This Part Is Uncomfortable) Before you can make a plan, you need complete, accurate information about every debt you owe. Here's exactly what I tracked in a simple spreadsheet: Debt Balance Interest Rate Minimum Payment Credit Card A $8,400 24.99% APR $210 Credit Card B $6,100 19.99% APR $155 Credit Card C $3,200 22.49% APR $80 Car Loan $14,500 6.9% APR $320 Student Loan $18,047 5.5% APR $195 Total $50,247 — $960/month Looking at that table was hard. But it was also the most important thing I did, because it turned a vague, overwhelming cloud of "I have a lot of debt" into a concrete list I could actually work through. Common mistake: Many people underestimate their total debt because they avoid checking balances. Log in to every account, pull your free credit report at AnnualCreditReport.com, and write down every number. Step 2: Build a Small Emergency Fund First Before throwing every extra dollar at debt, save $1,000 as a starter emergency fund. This sounds counterintuitive when you're paying 24.99% interest, but here's why it works: without a cash cushion, the first flat tire or medical co-pay goes right back on a credit card, undoing your progress and crushing your motivation. A 2025 KeyBank survey found that 25% of Americans cannot come up with $2,000 for unexpected expenses, up from 19% the year before. [2] That statistic shows how common this vulnerability is — and why plugging it first protects your entire plan. Once you hit $1,000, stop saving and redirect everything to debt. You can build a full 3–6 month emergency fund after you're debt-free. Step 3: Choose Your Debt Payoff Strategy Two methods dominate personal finance, and both work. The right one depends on your personality. Debt Snowball (Dave Ramsey's method): Pay minimums on all debts. Throw every extra dollar at the smallest balance first. When it's gone, roll that payment to the next smallest. Best for: people who need quick wins to stay motivated. Debt Avalanche: Pay minimums on all debts. Throw every extra dollar at the highest interest rate first. Best for: people who are motivated by math and want to pay the least interest overall. I used the snowball method because I needed to feel progress. Paying off that $3,200 credit card in four months gave me a surge of confidence that kept me going for the next two years. If you want a detailed breakdown of both approaches, check out this guide on 7 proven ways to pay down debt faster. Edge case: If you have a debt with a balance transfer offer at 0% APR, consider moving high-interest credit card balances there first. Harvard FCU recommends balance transfer cards as a way to freeze interest accrual and focus entirely on paying down principal. [5] Just watch for transfer fees (typically 3–5%) and make sure you can pay the balance before the promotional period ends. Step 4: Cut Expenses Without Losing Your Mind Cutting expenses is where most people start — and where many people quit, because they try to cut everything at once and feel deprived. My approach: cut in tiers. Tier 1 — Cut immediately (no lifestyle impact): Unused subscriptions and memberships Negotiated lower rates on phone, internet, and insurance Switched to generic/store-brand groceries Tier 2 — Reduce (some adjustment required): Eating out dropped from 4x/week to once a week Grocery budget planned with a weekly meal plan (I saved roughly $200/month here) Paused gym membership and worked out at home Tier 3 — Temporary sacrifices (hard but worth it): Skipped vacations for 18 months Sold my newer car and bought a paid-off used car, eliminating the $320/month payment A 2025 KeyBank survey found that 49% of consumers switched to less expensive brands or services and 41% reduced subscriptions or memberships in response to rising costs. [2] These aren't dramatic moves — they're practical ones that add up fast. For practical grocery savings, this budget meal planning guide shows how to feed a family on $50/week, which is a real game-changer when you're redirecting every dollar to debt. Step 5: Increase Your Income (This Is the Real Accelerator) Cutting expenses has a floor — you can only cut so much. Income has no ceiling. Adding even $300–$500 per month in extra income can cut months or years off your debt free journey. What I did to earn extra money: Sold stuff I didn't need. I made over $1,000 in 30 days selling furniture, clothes, and electronics. (This decluttering guide shows exactly how.) Freelanced on weekends. I offered writing and editing services through Upwork for about 8 hours per week. Used money-making apps. Small amounts — $50–$100/month — but every dollar went straight to debt. Every single dollar of extra income went directly to the target debt. Not to lifestyle upgrades. Not to "treating myself." Straight to the balance. If you're looking for ways to earn more without a second job, check out these 15 best money making apps that pay real cash or explore high income skills you can learn at home that can significantly boost your monthly income over time. How Do You Stay Motivated During a Long Debt Free Journey? Staying motivated over a multi-year debt payoff is genuinely the hardest part. The math is simple; the psychology is not. 38% of U.S. women report that money makes them feel anxious most of the time, compared to 24% of men, according to a 2026 Southwest Voices survey. [1] Debt stress is real, and ignoring it doesn't make it go away. What actually helped me stay on track: A visual debt payoff tracker. I colored in a bar graph on my fridge every time I paid off $1,000. Silly? Maybe. Effective? Absolutely. An accountability partner. My sister was on her own debt free journey. We checked in monthly. Celebrating milestones. When I paid off each account, I did something small and free to mark it — a picnic, a movie night at home. Reading stories like mine. Seeing that a debt-free family paid off $67K on one income made my $50K feel conquerable. If you're feeling overwhelmed, this resource on debt stress relief and staying motivated has practical strategies that go beyond "just believe in yourself." Decision rule: If you're losing motivation, don't restart from scratch. Switch strategies temporarily. If you've been doing the avalanche method, switch to snowball for one month to get a quick win. Then go back. What Was My Month-by-Month Debt Payoff Timeline? Here's an honest look at how the $50,247 came down over 26 months. I'm sharing this because most debt payoff stories skip the messy middle. Month Range Action Running Balance Months 1–2 Built $1,000 emergency fund $50,247 Months 3–6 Paid off Credit Card C ($3,200) $47,047 Months 7–11 Paid off Credit Card B ($6,100) $40,947 Months 12–16 Paid off Credit Card A ($8,400) $32,547 Month 17 Sold car, eliminated car loan $18,047 Months 18–26 Paid off student loan $0 Month 17 was the turning point. Selling the car felt terrifying, but it eliminated $14,500 in debt overnight and freed up $320/month. After that, the student loan felt manageable. Note on the car: I bought a $5,000 used Honda Civic with cash. It wasn't glamorous, but it ran fine and I drove it for two years while I finished paying off everything else. What Mistakes Almost Derailed My Debt Free Journey? Knowing what to avoid is just as important as knowing what to do. Mistake 1: Not having an emergency fund first.Early on, I skipped the $1,000 buffer and put everything at debt. Three months in, a $700 car repair went right back on a credit card. Demoralizing. Mistake 2: Setting an unrealistic budget.My first budget was so tight I lasted two weeks before blowing it. I had to build in a small "fun money" line — even $30/month — to make the budget sustainable. Mistake 3: Ignoring the emotional side.I white-knuckled it for the first six months without any support system. Burnout hit hard. Once I found an accountability partner and started tracking wins visually, consistency improved dramatically. Mistake 4: Lifestyle creep after early wins.After paying off the first credit card, I celebrated by spending more than I should have for a couple of months. I lost about six weeks of progress. Celebrate, but keep the momentum. To avoid common budgeting pitfalls, this list of 10 budgeting mistakes to avoid is worth reading before you build your plan. What Happens After You Become Debt-Free? Becoming debt-free is not the finish line — it's the starting line for building actual wealth. 38% of people say being debt-free is the most important financial milestone, according to the 2026 BHG Financial Consumer Debt & Finances Survey. [4] But once you're there, the same discipline that paid off debt becomes your wealth-building engine. Here's what I did the month I made my last payment: Built a full 3–6 month emergency fund using what used to be my debt payments. Started investing — maxed out my Roth IRA contribution for the year. Kept living on my "debt payoff budget" for six more months to build a real financial cushion. Raised my credit score — paying off revolving debt dramatically improved my utilization ratio. 74% of respondents in the BHG Financial survey feel optimistic about their financial future, with that number climbing to 80% among higher-income households. [4] I felt that shift personally. Once the debt was gone, financial decisions stopped feeling like damage control and started feeling like choices. For the next chapter, this guide on how to achieve financial freedom in 5 steps is exactly where I'd point anyone who just made their last debt payment. Frequently Asked Questions Q: How long does it realistically take to pay off $50,000 in debt?A: It depends on your income, expenses, and how aggressively you can pay. With focused effort — cutting expenses and adding income — most people can pay off $50,000 in 2–4 years. I did it in 26 months by combining both strategies. Q: Should I save money or pay off debt first?A: Build a small $1,000 emergency fund first, then attack debt aggressively. Without that buffer, unexpected expenses will send you back to credit cards and undo your progress. Q: What's the best method for paying off debt — snowball or avalanche?A: Both work. Snowball (smallest balance first) is better if you need motivational wins to stay consistent. Avalanche (highest interest first) saves more money mathematically. Choose the one you'll actually stick to. Q: Can I pay off debt on a low income?A: Yes, but it requires more focus on increasing income alongside cutting expenses. Even an extra $200–$300/month makes a significant difference over time. This guide on how to pay off credit card debt fast on a low income has specific strategies for tighter budgets. Q: Should I use a balance transfer card to pay off debt faster?A: A 0% APR balance transfer card can be a smart move for high-interest credit card debt, because it stops interest from accruing and lets you focus entirely on the principal. [5] Watch for transfer fees and make sure you have a plan to pay it off before the promotional period ends. Q: What if I have an emergency and go back into debt during my payoff journey?A: It happens. Don't quit. Rebuild your $1,000 buffer, then resume your payoff plan. One setback doesn't erase your progress. Q: Is a no-spend challenge worth trying during debt payoff?A: Absolutely. A no-spend month challenge can generate an extra $200–$500 in a single month, which goes directly to your target debt. It also resets spending habits in a lasting way. Q: How do I stay motivated when debt payoff feels like it's taking forever?A: Use a visual tracker, find an accountability partner, and celebrate each paid-off account. Also, recalculate your payoff date every few months — watching it move closer is genuinely motivating. Q: Will paying off debt hurt my credit score?A: Paying off installment loans (like a car or student loan) can cause a small, temporary dip because it reduces your credit mix. But paying off credit cards improves your utilization ratio, which typically raises your score. The net effect of becoming debt-free is almost always positive over time. Q: What's the first step if I'm completely overwhelmed and don't know where to start?A: Write down every debt you owe — balance, interest rate, minimum payment — in one place. That single act of clarity is the foundation of every successful debt free journey. Conclusion: Your Debt Free Journey Starts With One Decision Paying off $50,000 in debt wasn't about being perfect. It was about being consistent. I made mistakes, had setbacks, and had months where I wanted to give up. But I kept coming back to the plan. Here's your action plan for this week: List every debt with its balance, interest rate, and minimum payment. Set up a $1,000 starter emergency fund before you do anything else. Choose your payoff method (snowball or avalanche) and commit to it. Find one expense to cut and one way to earn extra money this month. Tell someone — an accountability partner changes everything. If you're ready to go deeper, the debt free in 12 months step-by-step plan is a great next resource, and these 10 simple habits that help you stay debt-free for life will help you protect everything you build. You don't need a perfect plan. You need a real one. Start today. References [1] Debt Free Flexible And Focused On Stability The Money Mindset Of Us Consumers In 2026 - https://www.southwestvoices.news/premium/stacker/stories/debt-free-flexible-and-focused-on-stability-the-money-mindset-of-us-consumers-in-2026,150595 [2] Is Debt Free The New Luxury Keybank Survey Explores 302606087 - https://www.prnewswire.com/news-releases/is-debt-free-the-new-luxury-keybank-survey-explores-302606087.html [4] Money Map Report - https://bhgfinancial.com/research/money-map-report [5] Gift Yourself Financial Peace How Be Debt Free In 2026 - https://harvardfcu.org/blog/gift-yourself-financial-peace-how-be-debt-free-in-2026/ Meta Title: How I Paid Off $50,000 in Debt: My Debt Free Journey Meta Description: I paid off $50,000 in debt in 26 months. Here's my honest, step-by-step debt free journey — what worked, what failed, and how you can do it too. Tags: debt free journey, paying off debt, debt snowball, debt avalanche, debt payoff plan, personal finance, budgeting tips, credit card debt, student loan payoff, financial freedom, debt stress, money motivation](https://msbudget.com/wp-content/uploads/2026/03/slot-0-1774952346462-500x330.png)