I’ll never forget the sinking feeling I had when I checked my credit score for the first time and saw a disappointing 580 staring back at me. It felt like a financial prison sentence—no decent apartment would rent to me, car loans were out of the question, and forget about getting approved for a rewards credit card. But here’s what I learned: your credit score isn’t a life sentence. It’s a number you can change, sometimes faster than you think. If you’re searching for ways to raise your credit score fast, you’re in the right place. Whether you’re starting from rock bottom or just trying to push past that 700 threshold, these 11 proven strategies can help you rebuild your credit health and open doors to better financial opportunities in 2025.

Key Takeaways

- Payment history is king: Your payment track record accounts for 35% of your FICO score—making on-time payments is the single most impactful way to improve your credit score

- Credit utilization matters more than you think: Keeping your credit card balances below 30% of your available credit can boost your score within weeks

- Quick wins exist: Disputing errors, becoming an authorized user, and requesting credit limit increases can raise your score in as little as 30 days

- Technology is your ally: Free credit monitoring tools and apps can help you track progress and catch issues before they damage your credit

- Consistency beats perfection: Small, regular improvements compound over time—focus on sustainable habits rather than quick fixes

Understanding How Credit Scores Actually Work

Before we dive into the specific ways to raise your credit score fast, let’s demystify what we’re actually dealing with. Your credit score is essentially a three-digit snapshot of your creditworthiness, calculated using complex algorithms that analyze your credit behavior.

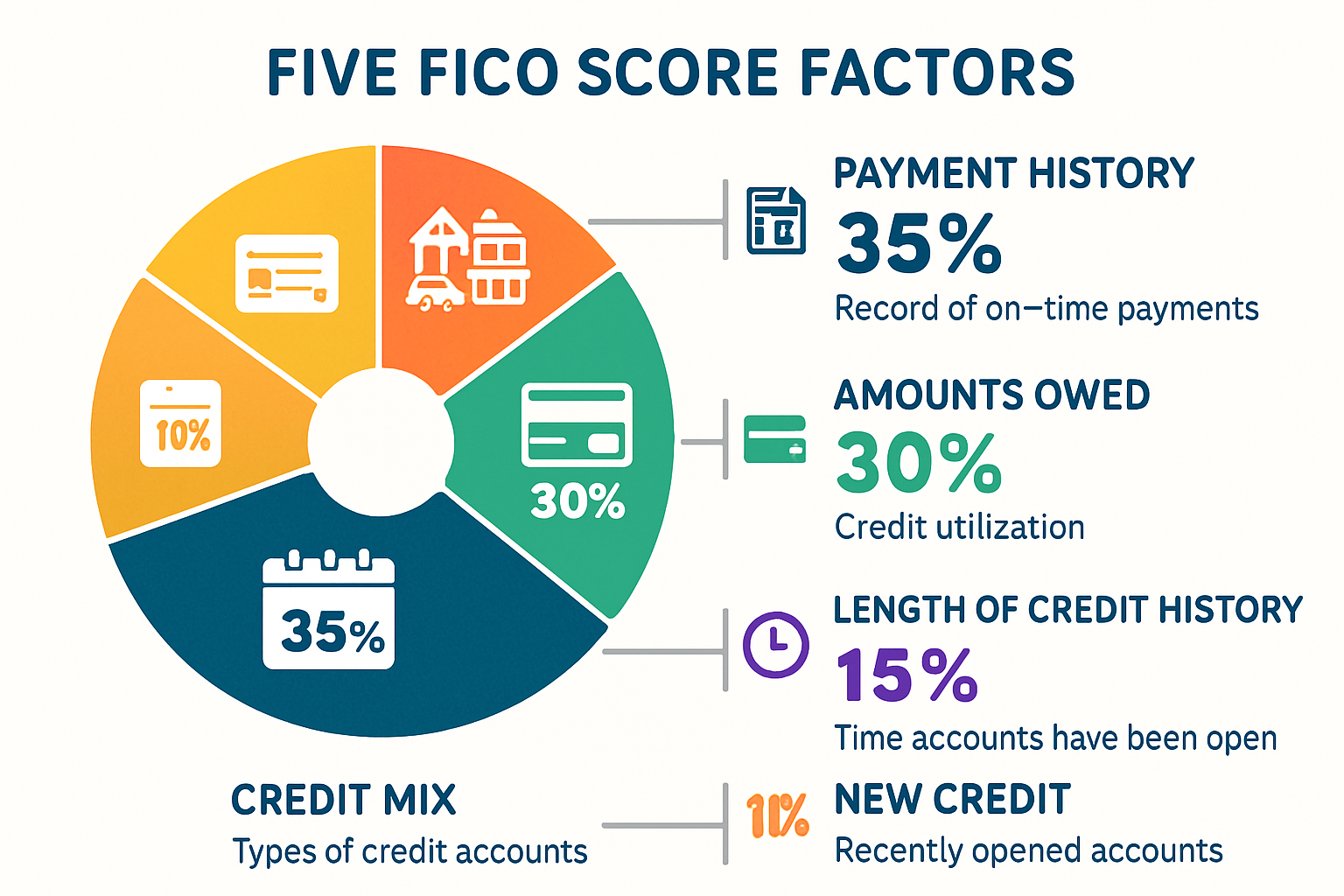

The most commonly used scoring model is the FICO score, which ranges from 300 to 850. Here’s how the credit scoring model breaks down:

| Credit Score Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | On-time vs. late payments, defaults, bankruptcies |

| Amounts Owed | 30% | Credit utilization ratio, total debt |

| Length of Credit History | 15% | Age of oldest account, average account age |

| Credit Mix | 10% | Diversity of credit types (cards, loans, mortgages) |

| New Credit | 10% | Recent credit inquiries and new accounts |

Understanding these credit score factors is crucial because it shows you exactly where to focus your energy. Notice that payment history and credit utilization make up 65% of your score—these are your highest-leverage opportunities for improvement.

The three major credit bureaus—Equifax, Experian, and TransUnion—collect information about your credit behavior from lenders and compile it into credit reports. Each bureau may have slightly different information, which is why your score can vary between them.

Here’s what most people don’t realize: your credit score isn’t static. It updates regularly as new information gets reported to the bureaus, typically every 30 days. This means that positive changes you make today can show up in your score within just a few weeks. That’s the foundation of every effective credit repair strategy—consistent, strategic actions that compound over time.

11 Proven Ways to Raise Your Credit Score Fast

💳 Credit Score Checker

Enter your current credit score to get personalized tips

1. 🎯 Make Every Payment On Time (No Exceptions)

This is the golden rule of credit score improvement. Since payment history accounts for 35% of your FICO score, nothing impacts your credit health more than your track record of paying bills when they’re due.

Here’s the brutal truth: a single late payment can drop your score by 60-110 points, and it stays on your credit report for seven years. But here’s the good news—the impact fades over time, and establishing a pattern of on-time payments can significantly boost your score within 3-6 months.

Actionable steps:

- Set up automatic payments for at least the minimum amount due

- Create calendar reminders 5 days before each due date

- Consider using payment apps that send push notifications

- Pay bills as soon as you receive them rather than waiting until the due date

- If you’ve missed payments, get current immediately and stay current—the positive payment history impact starts accumulating right away

I personally use a simple spreadsheet with all my payment due dates, but there are excellent apps like Mint or YNAB that can automate this tracking for you. The key is creating a system that works for your lifestyle and sticking to it religiously.

One insider tip: even if you can’t pay the full balance, always pay at least the minimum by the due date. Your payment history only tracks whether you paid on time—not whether you paid in full. Of course, paying in full is ideal to avoid interest charges, but from a credit score perspective, on-time minimum payments protect your score.

If you’re struggling with debt management, check out these proven ways to pay down debt faster that can help you stay current while making progress on your balances.

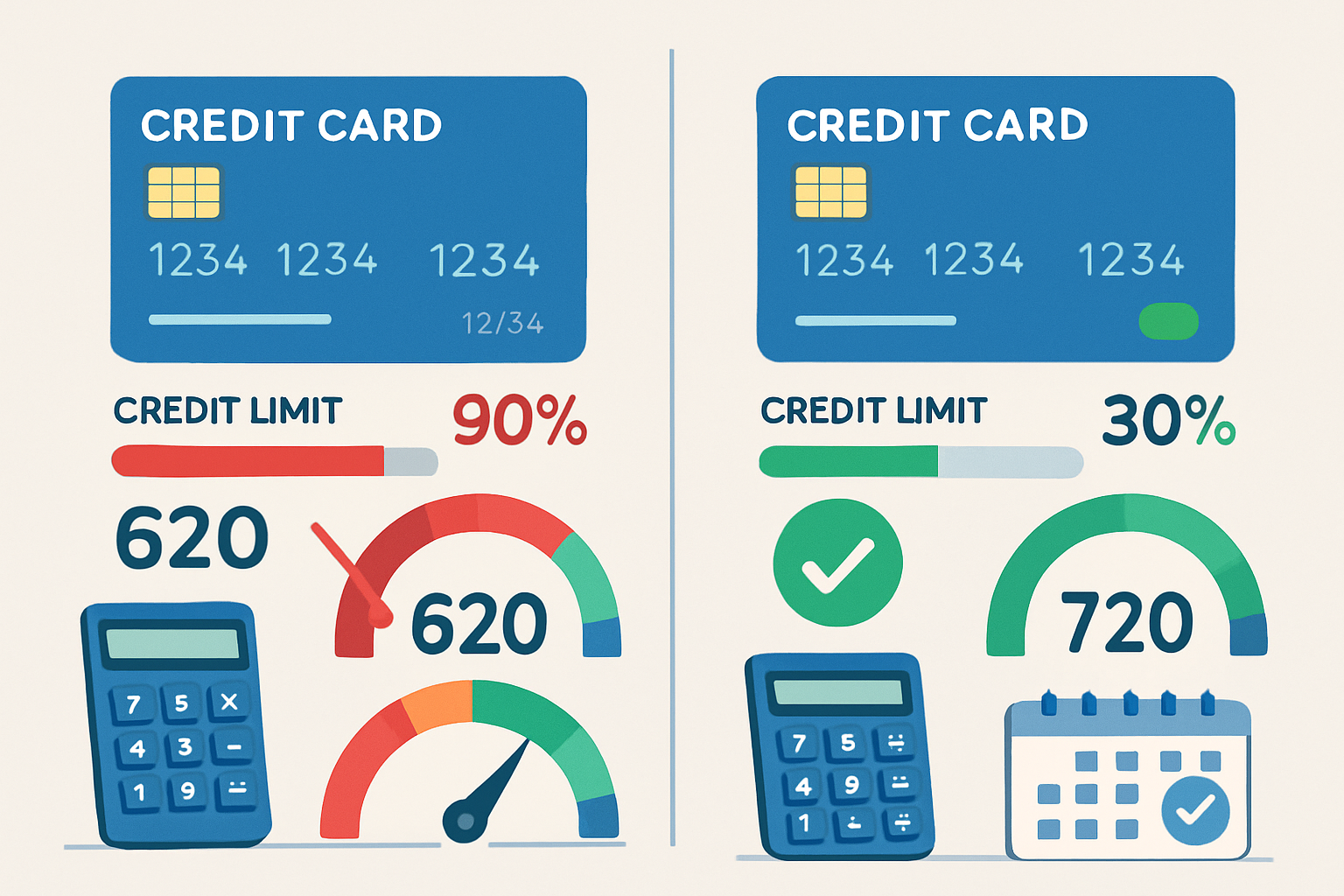

2. 📉 Slash Your Credit Utilization Ratio Below 30%

Your credit utilization ratio is the percentage of your available credit that you’re currently using. It’s the second most important factor in your credit score calculation, and it’s one of the fastest ways to see improvement.

Here’s how it works: If you have a credit card with a $10,000 limit and you’re carrying a $7,000 balance, your utilization is 70%—which is terrible for your score. Credit scoring models view high utilization as a sign of financial stress and credit risk.

The magic numbers:

- Below 30% utilization: Good

- Below 10% utilization: Excellent

- Below 5% utilization: Optimal

The beautiful thing about credit utilization is that it has no memory. Unlike late payments that haunt you for years, your utilization is calculated based on your current balances. This means you can see score improvements within 30-60 days of paying down balances.

Strategic approaches to lower utilization:

- Pay down existing balances: Focus on cards with the highest utilization first

- Make multiple payments per month: Instead of one monthly payment, make weekly payments to keep your reported balance low

- Request credit limit increases: This instantly lowers your utilization ratio without requiring you to pay down debt (more on this in #6)

- Spread balances across multiple cards: If you have $5,000 in debt, it’s better to have $1,000 on five cards than $5,000 on one card

- Time your payments strategically: Pay your balance before your statement closing date, not just before the due date, so a lower balance gets reported to the bureaus

I’ve seen people boost their scores by 40-60 points in just two months by aggressively paying down credit card balances. It’s one of the most powerful credit building techniques available.

For additional strategies on managing your money more effectively, explore these simple habits that help you stay debt-free for life.

3. 🔍 Dispute Errors on Your Credit Report

Here’s a shocking statistic: according to a Federal Trade Commission study, one in five consumers has an error on at least one of their credit reports[1]. These errors can range from accounts that don’t belong to you to incorrect late payment marks to outdated negative information that should have been removed.

Credit report optimization starts with knowing what’s on your reports. You’re entitled to one free credit report from each of the three major bureaus every year through AnnualCreditReport.com. In 2025, many credit monitoring services also offer free access to your reports.

Common errors to look for:

- Accounts that aren’t yours (possible identity theft)

- Incorrect account statuses (showing open when closed, or vice versa)

- Wrong credit limits (which can inflate your utilization ratio)

- Late payments you didn’t actually make

- Duplicate accounts

- Negative items older than seven years (ten years for bankruptcies)

- Incorrect personal information

The dispute process:

- Document the error: Take screenshots and gather any supporting documentation

- File disputes with all three bureaus: Errors on one report may not appear on others, but dispute with all three to be safe

- Submit your dispute online: Each bureau has an online dispute portal that’s faster than mail

- Be specific and provide evidence: Vague disputes get rejected; detailed disputes with documentation get resolved

- Follow up: Bureaus have 30 days to investigate; check back to ensure the error was corrected

I once helped a friend dispute a late payment that was incorrectly reported—she had proof of on-time payment. Within 45 days, the error was removed and her score jumped 35 points. That’s the power of credit report accuracy.

One advanced tip: if the bureaus don’t remove the error after your dispute, you can escalate by filing a complaint with the Consumer Financial Protection Bureau (CFPB). This often gets faster results because creditors take CFPB complaints very seriously.

4. 🚀 Become an Authorized User on Someone Else’s Account

This is one of the lesser-known credit repair strategies, but it can be incredibly effective, especially if you’re starting with a thin credit file or recovering from past mistakes.

When you become an authorized user on someone else’s credit card account, that account’s history may be added to your credit report. If the primary cardholder has a long history of on-time payments and low utilization, you can benefit from their positive credit behavior.

How to make this work:

- Choose the right person: Look for someone with excellent credit, a long account history, low utilization, and perfect payment history

- Confirm reporting: Not all issuers report authorized user accounts to all three bureaus; call and verify before proceeding

- You don’t need the card: You can be added as an authorized user without actually receiving or using the card

- Monitor the account: If the primary cardholder’s behavior changes (starts missing payments or maxing out the card), remove yourself immediately

Best candidates to ask:

- Parents or family members with established credit

- A spouse or partner with excellent credit

- Close friends who trust you (though this can be awkward)

I’ve seen this strategy add 50-100 points to someone’s score within 60 days, especially for young adults with limited credit history. The key is finding someone with a pristine credit account that’s at least 5-10 years old.

Important caveat: This is a supplemental strategy, not a replacement for building your own credit history. FICO’s newer scoring models can distinguish between authorized users and primary account holders, so you’ll eventually need your own positive credit accounts.

5. 📅 Keep Old Accounts Open (Even If You Don’t Use Them)

The length of your credit history accounts for 15% of your FICO score. This factor considers both the age of your oldest account and the average age of all your accounts. Many people make the mistake of closing old credit cards once they’re paid off, thinking it’s the responsible thing to do. In reality, this can hurt your score in two ways:

- It reduces your available credit, which increases your credit utilization ratio

- It can lower your average account age, especially if you close your oldest account

Strategy for managing old accounts:

- Keep your oldest cards active: Even if you don’t use them regularly, keep them open

- Use them occasionally: Put a small recurring charge on old cards (like a streaming subscription) and set up autopay to keep them active

- Avoid closing accounts after paying them off: Unless there’s an annual fee you can’t justify, keep paid-off cards open

- If you must close an account: Close newer accounts rather than older ones

Here’s a real example: Let’s say you have three credit cards—one that’s 10 years old, one that’s 5 years old, and one that’s 2 years old. Your average account age is 5.67 years. If you close the 10-year-old card, your average drops to 3.5 years. That’s a significant decrease that could lower your score.

The exception to this rule: if an old card has a high annual fee and you’re not getting value from it, the financial savings might outweigh the credit score impact. You’ll need to make that judgment call based on your specific situation.

For more insights on managing your overall financial health, consider these budgeting mistakes to avoid that could be holding you back.

6. 💳 Request Credit Limit Increases

This is one of my favorite ways to raise your credit score fast because it can work almost instantly and requires minimal effort. Requesting a credit limit increase lowers your credit utilization ratio without requiring you to pay down debt.

Here’s the math: If you have a $5,000 credit limit and carry a $2,500 balance, your utilization is 50%. If you get your limit increased to $10,000 while keeping the same $2,500 balance, your utilization drops to 25%—instantly moving you into the “good” range.

How to request increases strategically:

- Time your request: Wait until you’ve had the card for at least 6-12 months and have a perfect payment history

- Prepare your case: Be ready to explain why you deserve an increase (income increase, excellent payment history, etc.)

- Ask for a specific amount: Don’t just say “increase my limit”—request a specific number that would meaningfully lower your utilization

- Know if it’s a hard or soft inquiry: Some issuers do a hard credit pull for limit increases, which can temporarily ding your score; ask before they process the request

- Try every 6 months: If denied, wait six months and try again

Pro tip: Many credit card issuers allow you to request increases online without speaking to anyone. Some even offer automatic increases if you’ve been a good customer. Check your account settings or call customer service to ask about automatic increase programs.

I personally request limit increases on all my cards every 6-12 months. Over the past five years, I’ve increased my total available credit from $15,000 to over $60,000, which keeps my utilization extremely low even when I use my cards regularly.

Important warning: Getting a credit limit increase only helps if you don’t increase your spending. If you get a higher limit and immediately max it out, you’ve accomplished nothing. This strategy requires discipline.

7. 🎨 Diversify Your Credit Mix

While credit account diversity only accounts for 10% of your FICO score, it can still make a meaningful difference, especially if you’re trying to break into the “excellent” credit range (750+).

Credit scoring models like to see that you can responsibly manage different types of credit:

- Revolving credit: Credit cards, retail cards, lines of credit

- Installment loans: Auto loans, personal loans, student loans, mortgages

- Open accounts: Charge cards that must be paid in full each month

If you only have credit cards, adding an installment loan can boost your score. If you only have loans, adding a credit card (and using it responsibly) can help.

How to diversify without going into unnecessary debt:

- Credit builder loans: Some credit unions offer small loans specifically designed to help build credit; you make payments into a savings account and get the money back at the end

- Secured credit cards: If you don’t have any credit cards, a secured card (backed by a cash deposit) is a safe way to start

- Retail store cards: These are easier to get approved for and can add to your credit mix, though they often have high interest rates (pay in full!)

- Don’t take on debt just for credit score purposes: Only add credit types that make sense for your financial situation

I added a small personal loan to my credit mix a few years ago specifically to improve this factor. I borrowed $2,000, put it in a savings account, and made automatic monthly payments from that same account. It cost me about $150 in interest over the year, but my score increased by 25 points. For me, that was worth it because I was preparing to apply for a mortgage.

Reality check: Don’t obsess over credit mix if you’re just starting out. Focus on payment history and utilization first. Credit mix becomes more important once you’ve mastered the basics.

8. 🛑 Limit New Credit Applications (Hard Inquiries)

Every time you apply for new credit, the lender typically performs a “hard inquiry” or “hard pull” on your credit report. These inquiries can lower your score by 5-10 points each and remain on your report for two years (though they only impact your score for about 12 months).

New credit accounts for 10% of your FICO score, and multiple applications in a short period can signal financial desperation to lenders—a red flag in credit risk assessment.

Smart application strategies:

- Rate shopping window: FICO scoring models allow a 14-45 day window for rate shopping on auto loans, mortgages, and student loans; multiple inquiries for the same type of loan within this window count as a single inquiry

- Prequalification tools: Many lenders offer “soft pull” prequalification that doesn’t impact your score; use these to gauge your approval odds before applying

- Space out applications: If you need multiple credit products, space them out by at least 6 months

- Be selective: Only apply for credit you actually need and have a reasonable chance of getting

What doesn’t hurt your score:

- Checking your own credit (soft inquiry)

- Prequalification checks (soft inquiry)

- Employment credit checks

- Insurance quote inquiries

- Existing creditors reviewing your account

I made the mistake early in my credit journey of applying for three credit cards in one month because I was excited about rewards programs. My score dropped 40 points. It took six months to recover. Learn from my mistake—patience pays off.

If you’re working on improving your overall financial situation, these smart money saving tips can help you build a stronger foundation.

9. 💰 Pay Down Collections and Charge-Offs Strategically

If you have collections or charge-offs on your credit report, they’re doing serious damage to your score. However, how you handle them matters significantly for your credit score recovery.

Important distinctions:

- Collections: Debt that’s been sold to a collection agency

- Charge-offs: Debt the original creditor has written off as unlikely to be collected (though they may still pursue payment)

Here’s what many people don’t know: paying off a collection or charge-off doesn’t automatically remove it from your credit report. The account will be updated to show “paid,” but it can still remain on your report for up to seven years from the date of first delinquency.

Strategic approaches:

- Pay for delete: Before paying, negotiate with the collection agency to remove the item from your credit report in exchange for payment; get this agreement in writing

- Validate the debt: Request debt validation to ensure the collection is legitimate and the amount is correct; about 30% of collections contain errors

- Settle for less: Collection agencies often accept 30-50% of the original amount; negotiate before paying full price

- Prioritize recent collections: Older collections have less impact on your score; focus on recent ones first

- Know your statute of limitations: After a certain period (varies by state), debt becomes “time-barred” and collectors can’t sue you for it

Newer scoring models are more forgiving: FICO 9 and VantageScore 3.0 and 4.0 ignore paid collections entirely. However, many lenders still use older models, so don’t assume paying a collection will immediately boost your score.

I once helped a family member negotiate a “pay for delete” on a $1,200 medical collection. We settled for $600 and got it removed from her report within 60 days. Her score increased by 55 points. That’s the power of strategic negotiation.

Warning: Be careful about acknowledging very old debt. In some cases, making a payment or even acknowledging the debt can restart the statute of limitations. Consult with a credit counselor or attorney if you’re dealing with debt older than 4-5 years.

10. 🔔 Set Up Credit Monitoring and Alerts

In 2025, there’s no excuse for not knowing what’s happening with your credit. Credit monitoring tools can alert you to changes in real-time, helping you catch errors, fraud, or unexpected changes before they cause serious damage.

Free monitoring options:

- Credit Karma (free scores and monitoring from TransUnion and Equifax)

- Credit Sesame (free monitoring and score tracking)

- Experian (free FICO score and monitoring)

- Many credit card issuers now offer free FICO scores to cardholders

What to monitor:

- Score changes (understand what’s driving increases or decreases)

- New accounts (catch identity theft early)

- Hard inquiries (spot unauthorized credit applications)

- Credit utilization changes

- Payment history updates

- Public records (bankruptcies, liens, judgments)

Set up alerts for:

- Any new account opened in your name

- Hard inquiries

- Score changes of 20+ points

- Late payments reported

- Credit limit changes

I check my credit monitoring app every Monday morning—it takes about 60 seconds and has saved me twice from fraudulent applications. Early detection is everything when it comes to credit account management.

Advanced tip: Use a credit monitoring service that offers “credit score simulators.” These tools let you model how different actions (paying off a card, opening a new account, etc.) would impact your score before you actually do them. It’s like having a crystal ball for your credit decisions.

For more ways to take control of your finances, check out these genius savings strategy hacks that can complement your credit improvement journey.

11. 🎓 Consider Credit Counseling or Professional Help

Sometimes the best credit building techniques involve getting expert guidance. If you’re overwhelmed, dealing with serious credit damage, or just want personalized advice, professional help can accelerate your progress.

When to consider professional help:

- You have multiple collections, charge-offs, or judgments

- You’re recovering from bankruptcy

- You’ve been a victim of identity theft

- You don’t understand your credit report

- You’ve tried DIY methods without success

Options for professional assistance:

- Nonprofit credit counseling: Organizations like the National Foundation for Credit Counseling (NFCC) offer free or low-cost counseling

- Credit repair companies: Can dispute errors and negotiate with creditors, but be cautious—many are scams; look for companies with proven track records and avoid any that guarantee specific score increases

- Financial advisors: Can help with overall financial planning, including credit improvement strategies

- Debt management plans: Structured programs that consolidate payments and negotiate lower interest rates

Red flags to avoid:

- Companies that ask for payment before providing services

- Promises to remove accurate negative information

- Suggestions to create a new credit identity (this is illegal)

- Pressure to sign contracts immediately

- Companies that won’t explain their process

What legitimate credit counselors can do:

- Review your credit reports and explain what’s hurting your score

- Create a personalized action plan

- Negotiate with creditors on your behalf

- Help you understand your rights under the Fair Credit Reporting Act

- Provide financial education and budgeting support

I personally used a nonprofit credit counselor when I was starting my credit journey. The counselor helped me understand which debts to prioritize and created a 12-month action plan that increased my score from 580 to 695. The service was free, and the guidance was invaluable.

DIY vs. Professional: For most people, the strategies in this article are enough to significantly improve your credit score without paying for services. However, if you’re dealing with complex situations or feel stuck, professional help can provide clarity and acceleration.

If you’re working on becoming debt-free as part of your credit improvement journey, this step-by-step plan anyone can follow offers a comprehensive roadmap.

How Fast Can You Actually Raise Your Credit Score?

This is the million-dollar question everyone asks: “How long will this take?” The honest answer is: it depends on your starting point and which strategies you implement.

Realistic timelines for credit score improvement:

| Starting Situation | Strategy | Expected Timeline | Potential Score Increase |

|---|---|---|---|

| High utilization (60%+) | Pay down to <30% | 30-60 days | 40-80 points |

| Credit report errors | Dispute and remove | 30-45 days | 20-100 points |

| Become authorized user | Added to established account | 30-60 days | 30-100 points |

| No recent late payments | Establish 6 months on-time payments | 6 months | 50-100 points |

| Recent late payments | Wait for impact to fade | 12-24 months | Gradual recovery |

| Collections/charge-offs | Pay for delete | 30-90 days | 30-80 points |

| Thin credit file | Build credit history | 6-12 months | 50-150 points |

Fastest improvements (30-90 days):

- Paying down high credit card balances

- Disputing and removing errors

- Becoming an authorized user

- Getting credit limit increases

Medium-term improvements (3-6 months):

- Establishing consistent on-time payment history

- Adding new credit types to your mix

- Recovering from recent hard inquiries

Long-term improvements (6-24 months):

- Recovering from late payments

- Building credit history length

- Recovering from bankruptcies or foreclosures

My personal timeline: Starting from 580, I hit 650 in three months by disputing errors and paying down balances. I reached 720 in nine months by maintaining perfect payment history and becoming an authorized user. Breaking 760 took another year of consistent good behavior.

The key insight: early improvements come fast, but reaching “excellent” credit takes patience. Don’t get discouraged if your progress slows after the initial boost—that’s normal.

Common Mistakes That Sabotage Your Credit Score

Even when you’re trying to improve your credit, certain mistakes can undermine your progress. Here are the surprising things that hurt your credit score that many people don’t realize:

1. Closing old credit cards: As mentioned earlier, this reduces your available credit and can lower your average account age

2. Only making minimum payments: While this protects your payment history, it keeps your utilization high and costs you a fortune in interest

3. Ignoring small balances: A $50 balance on a $500 limit card creates 10% utilization on that card; pay it off completely

4. Applying for retail cards at checkout: That 10% discount isn’t worth the hard inquiry and potential score drop

5. Consolidating credit card debt onto a single card: This can spike your utilization on that card to 90%+, even if your overall utilization stays the same

6. Canceling cards after balance transfers: This eliminates the available credit you just freed up

7. Ignoring medical collections: These hurt your score just like any other collection; negotiate payment or dispute if inaccurate

8. Assuming paid collections disappear: They don’t—they just show as “paid” but remain on your report

9. Letting authorized user accounts hurt you: If the primary cardholder’s behavior deteriorates, remove yourself immediately

10. Not checking all three bureaus: Errors might only appear on one bureau; check all three annually

I made mistake #5 when I consolidated $8,000 in debt onto a single card with a $10,000 limit. My utilization on that card jumped to 80%, and my score dropped 35 points even though my overall utilization barely changed. I learned that per-card utilization matters as much as overall utilization.

The Psychology of Credit Improvement: Staying Motivated

Improving your credit score is as much a psychological challenge as a financial one. The process requires patience, discipline, and delayed gratification—qualities that don’t come naturally to everyone.

Mental frameworks that help:

1. Track your progress visually: Create a chart showing your score over time; seeing the upward trend provides motivation

2. Celebrate small wins: Hit 600? Celebrate. Removed an error? Celebrate. Paid off a card? Celebrate. These milestones matter.

3. Focus on what you can control: You can’t change the past, but you can control your behavior today and tomorrow

4. Reframe setbacks: A denied credit application isn’t personal rejection—it’s just data telling you you’re not quite ready yet

5. Connect credit to your bigger goals: Remind yourself why you’re doing this—to buy a house, get a better car loan rate, qualify for that rewards card, etc.

6. Find an accountability partner: Share your goals with someone who will check in on your progress

7. Automate good behavior: Set up automatic payments and alerts so good credit behavior happens without willpower

I keep a simple spreadsheet where I log my credit score on the first of every month. Seeing the number climb from 580 to 775 over two years was incredibly motivating, especially during months when progress felt slow.

The compound effect: Small improvements in credit behavior compound over time, just like investments. A 5-point increase this month plus a 7-point increase next month plus a 10-point increase the month after that adds up to meaningful change.

Technology Tools to Accelerate Your Credit Journey

In 2025, we have access to incredible credit monitoring technology that previous generations could only dream of. Here are the tools I personally use and recommend:

Credit monitoring apps:

- Credit Karma: Free scores from TransUnion and Equifax, plus personalized recommendations

- Experian: Free FICO score (the score most lenders actually use)

- Credit Sesame: Free monitoring with financial planning tools

- MyFICO: Paid service ($30-40/month) that provides all three FICO scores and comprehensive monitoring

Budgeting and payment apps:

- YNAB (You Need A Budget): Helps ensure you have money for all payments before they’re due

- Mint: Free budget tracking with bill payment reminders

- Prism: Consolidates all your bills in one place with payment reminders

Credit building tools:

- Self: Credit builder loan that reports to all three bureaus

- Chime Credit Builder: Secured credit card with no fees or interest

- Experian Boost: Free service that adds utility and streaming payments to your Experian credit report

Debt payoff calculators:

- Unbury.me: Visual debt payoff calculator showing avalanche vs. snowball methods

- Credit Karma’s debt repayment calculator: Shows how different payment strategies affect your timeline

I use Credit Karma for weekly monitoring, Experian for my actual FICO score, and YNAB to ensure I never miss a payment. This combination costs me $15/month for YNAB (Experian and Credit Karma are free) and has been worth every penny.

Automation is your friend: The more you can automate—payments, monitoring, alerts—the less you have to rely on memory and willpower. I have 17 different automated payments set up, and I haven’t missed a payment in over five years.

For additional ways to optimize your financial life, explore these passive income ideas that can provide extra cash flow to pay down debt faster.

Credit Score Improvement for Different Life Stages

Your age and life stage significantly impact both your credit challenges and your opportunities for improvement.

Young Adults (18-25): Building from Scratch

Challenges:

- Thin or nonexistent credit file

- Limited income

- Student loan debt

- Lack of credit education

Best strategies:

- Become an authorized user on a parent’s account

- Get a secured credit card and use it responsibly

- Keep student loans in good standing (on-time payments build credit)

- Start with a credit builder loan

- Avoid the temptation of easy retail credit cards

Timeline: You can build a 700+ score within 12-18 months starting from zero

Mid-Career Adults (26-45): Optimization and Recovery

Challenges:

- Recovering from past mistakes

- Balancing multiple financial priorities (mortgage, kids, retirement)

- Higher debt levels

Best strategies:

- Focus on utilization management as income increases

- Diversify credit mix strategically

- Leverage higher income to request credit limit increases

- Address any lingering collections or charge-offs

- Maintain long-term accounts while adding new ones strategically

Timeline: Recovery from moderate credit damage can take 6-24 months

Established Adults (46-65): Maintenance and Maximization

Challenges:

- Complacency (assuming good credit is permanent)

- Major purchases (homes, investment properties) that require excellent credit

- Potential identity theft (older adults are targeted more frequently)

Best strategies:

- Protect your excellent credit with monitoring

- Maintain low utilization even with high available credit

- Keep oldest accounts active

- Be strategic about new credit for major purchases

- Consider freezing your credit when not actively seeking new credit

Timeline: Maintaining excellent credit is ongoing; recovering from unexpected damage can take 3-12 months

Seniors (65+): Protection and Simplification

Challenges:

- Fixed income making credit management more critical

- Increased identity theft risk

- Confusion about credit in retirement

Best strategies:

- Simplify credit accounts while maintaining history

- Set up fraud alerts and monitoring

- Maintain some credit cards for emergency access

- Understand that good credit matters even in retirement (insurance rates, rental applications, etc.)

- Consider credit freezes for protection

I’ve helped my parents (both in their 70s) set up credit monitoring and fraud alerts. They were surprised to learn their credit scores still matter for things like insurance premiums and rental applications when they travel.

FAQ: Your Credit Score Questions Answered

Q: What is a good credit score in 2025?

A: Credit scores range from 300-850. Here’s the breakdown:

- 300-579: Poor

- 580-669: Fair

- 670-739: Good

- 740-799: Very Good

- 800-850: Exceptional

Most lenders consider 670+ to be “good” credit, but the best rates and terms typically require 740+. For the absolute best mortgage rates, aim for 760+.

Q: How fast can you improve your credit score?

A: It depends on your starting point and which strategies you use. Quick wins like disputing errors, paying down high balances, or becoming an authorized user can show results in 30-60 days. Building from a low score to excellent credit typically takes 12-24 months of consistent positive behavior.

Q: Do credit repair companies actually work?

A: Legitimate credit repair companies can help by disputing errors and negotiating with creditors, but they can’t do anything you couldn’t do yourself for free. Many are scams. If you choose to use one, research thoroughly, avoid any that guarantee specific results, and never pay upfront fees before services are rendered.

Q: Will paying off collections improve my score?

A: Not always immediately. Paying a collection updates it to “paid,” but it doesn’t remove it from your report. However, newer scoring models (FICO 9, VantageScore 3.0+) ignore paid collections, so it can help if lenders use these models. Always try to negotiate “pay for delete” before paying.

Q: How many credit cards should I have?

A: There’s no magic number, but most credit experts recommend 3-5 cards. This provides enough available credit to keep utilization low while building a diverse credit history. The key is using them responsibly, not the specific number.

Q: Does checking my own credit score hurt it?

A: No. Checking your own credit is a “soft inquiry” that doesn’t impact your score. You can check as often as you want through services like Credit Karma, Experian, or your credit card issuer.

Q: Can I remove accurate negative information from my credit report?

A: Generally, no. Accurate negative information can remain on your report for 7 years (10 years for bankruptcies). However, you can sometimes negotiate “pay for delete” with collection agencies, or request goodwill adjustments from creditors for isolated late payments if you have an otherwise perfect history.

Q: Should I close credit cards I’m not using?

A: Usually no. Keeping old cards open helps your credit utilization ratio and average account age. The exception is if the card has a high annual fee you can’t justify, or if having the card tempts you to overspend.

Taking Action: Your 30-Day Credit Improvement Plan

Knowledge without action is useless. Here’s a concrete 30-day plan to jumpstart your credit improvement journey:

Week 1: Assessment and Foundation

- Day 1-2: Pull all three credit reports from AnnualCreditReport.com

- Day 3-4: Review reports thoroughly and document any errors

- Day 5: Sign up for free credit monitoring (Credit Karma, Experian)

- Day 6: Calculate your current credit utilization across all cards

- Day 7: Set up automatic payments for all credit accounts

Week 2: Quick Wins

- Day 8-9: File disputes for any errors found on your credit reports

- Day 10-11: Pay down credit card with highest utilization

- Day 12: Request credit limit increases on cards with good payment history

- Day 13: Become an authorized user on a family member’s account (if possible)

- Day 14: Review and organize all bills to ensure nothing falls through cracks

Week 3: Strategic Improvements

- Day 15-16: Contact collection agencies to negotiate “pay for delete” agreements

- Day 17-18: Make additional payments on high-balance cards

- Day 19: Set up calendar reminders for all payment due dates

- Day 20: Research credit builder loans if you have thin credit

- Day 21: Check credit monitoring app and review any changes

Week 4: Long-Term Habits

- Day 22-23: Create a budget to ensure you can afford all payments (check out saving money tips on a tight budget)

- Day 24-25: Set up bi-weekly credit card payments to keep utilization low

- Day 26: Review old credit cards and decide which to keep active

- Day 27-28: Make small purchases on old cards to keep them active

- Day 29: Follow up on credit report disputes

- Day 30: Check your credit score and document your progress

After 30 days: Repeat the cycle, focusing on maintaining good habits and addressing any remaining issues. Check your score monthly to track progress.

This plan combines quick wins with sustainable long-term habits. You should see measurable improvement within 60-90 days if you follow it consistently.

The Bigger Picture: Credit as Part of Financial Health

While improving your credit score is important, it’s just one piece of your overall financial health puzzle. A great credit score means little if you’re drowning in debt or have no emergency savings.

Holistic financial health includes:

- Emergency fund: 3-6 months of expenses in savings

- Debt management: Paying down high-interest debt aggressively

- Budget discipline: Living below your means consistently

- Retirement savings: Contributing regularly to retirement accounts

- Insurance coverage: Protecting against major financial risks

- Credit health: Maintaining a strong credit profile

Think of your credit score as a tool that enables other financial goals—lower interest rates mean more money for savings and investments, better insurance rates reduce monthly expenses, and access to credit provides a safety net for emergencies.

I’ve seen people obsess over raising their score from 780 to 800 while carrying $30,000 in credit card debt at 22% APR. That’s missing the forest for the trees. Focus on the fundamentals: spend less than you earn, pay off high-interest debt, build savings, and your credit score will naturally improve as a byproduct of good financial behavior.

For a comprehensive approach to managing your finances, consider starting with a new year budget plan that addresses all aspects of your financial life.

Conclusion: Your Credit Score Is a Journey, Not a Destination

Improving your credit score isn’t a one-time project—it’s an ongoing journey that requires consistent attention and good habits. The ways to raise your credit score fast that I’ve outlined in this guide are proven, actionable strategies that work for people at every credit level.

Remember these key principles:

✅ Payment history is everything: Never miss a payment, no matter what

✅ Utilization matters: Keep balances low relative to your limits

✅ Errors hurt: Check your reports regularly and dispute inaccuracies

✅ Time is your ally: The longer you maintain good habits, the stronger your credit becomes

✅ Quick wins exist: Some strategies show results in 30-60 days

✅ Technology helps: Use apps and automation to make good behavior effortless

Whether you’re starting at 550 or pushing toward 800, every positive action you take compounds over time. The person with a 580 score who implements these strategies consistently will likely have better credit in 18 months than someone with a 720 who gets complacent.

Your next steps:

- Check your credit score today (it’s free!)

- Pull your credit reports and look for errors

- Choose 3-5 strategies from this guide to implement immediately

- Set up automatic payments and monitoring

- Track your progress monthly

- Celebrate small wins along the way

Your credit score is a powerful financial tool that impacts everything from loan rates to job opportunities to housing options. By taking control of it today, you’re investing in your financial future and opening doors to opportunities that might currently be closed.

Start today. Your future self will thank you.

For more resources on building a stronger financial foundation, visit MSBudget for comprehensive guides on budgeting, saving, and achieving financial freedom.