Let me be honest with you: I used to think budgeting was for people who didn’t make enough money. Then I realized I was making decent money but still couldn’t figure out where it all went by the end of the month. Sound familiar? If you’re tired of the paycheck-to-paycheck cycle and ready to take control of your finances in 2025, understanding the budgeting mistakes to avoid is your first step toward financial freedom.

The truth is, most people don’t fail at budgeting because they lack willpower or don’t earn enough. They fail because they’re making critical mistakes that sabotage their efforts from the start. These aren’t small oversights—they’re fundamental errors that keep you trapped in a cycle of financial stress, regardless of your income level.

Key Takeaways

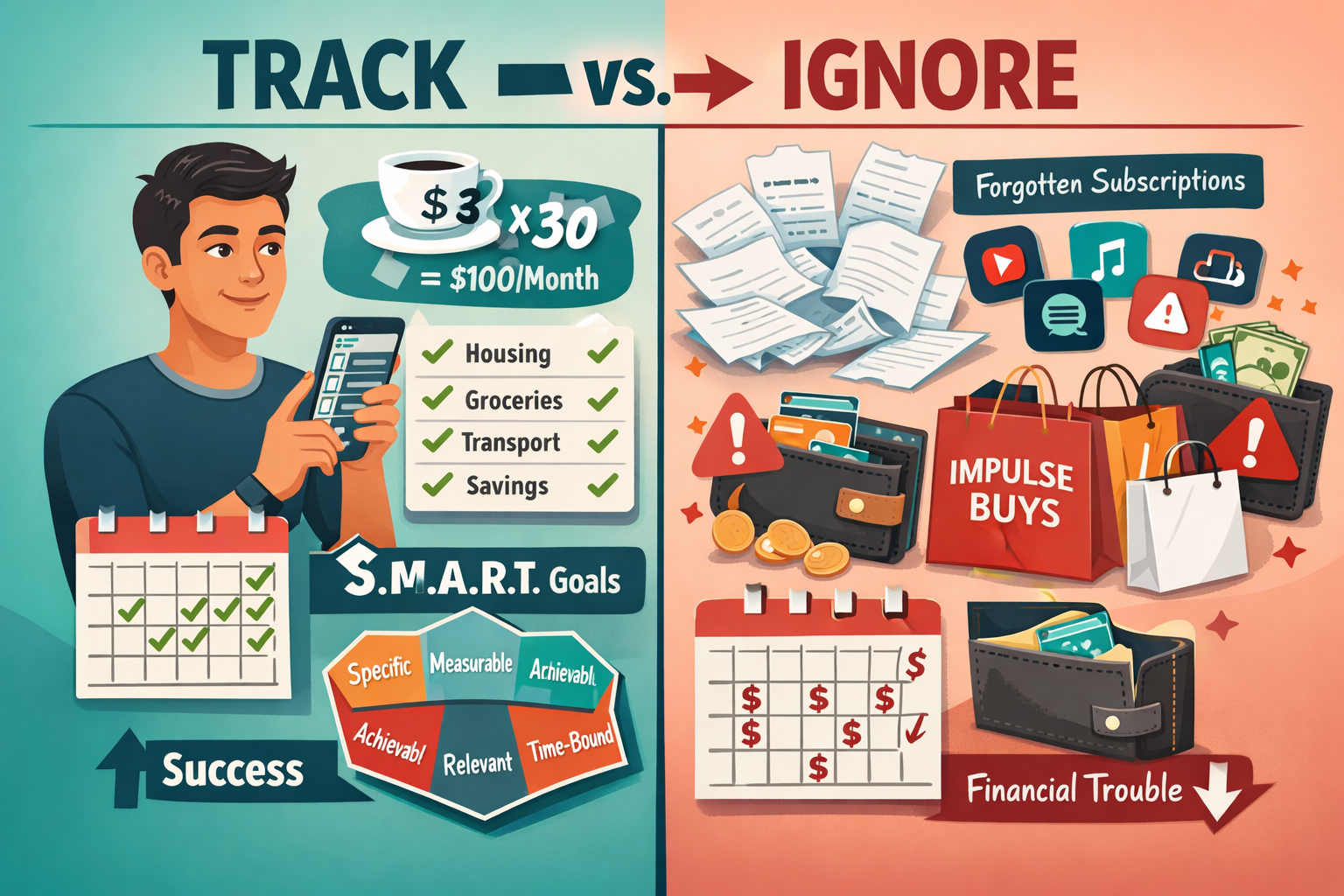

- Tracking matters more than planning: Small daily expenses like a $3 coffee add up to over $100 monthly—tracking reveals where your money actually goes

- Realistic goals prevent burnout: Setting achievable targets using the SMART method creates sustainable budgeting habits instead of restrictive plans that fail

- Emergency funds are non-negotiable: Starting with just $500 prevents single unexpected expenses from derailing your entire financial plan

- Budget on net income, not gross: Using your actual take-home pay as your baseline prevents overallocation and budget shortfalls

- Flexibility sustains success: Allowing discretionary spending in areas you value maintains long-term motivation and prevents impulsive overspending

Understanding Why Budgeting Mistakes Keep You Stuck

Before we dive into the specific budgeting mistakes to avoid, let’s talk about why these errors are so damaging. When you make fundamental budgeting mistakes, you’re not just losing money—you’re losing momentum, confidence, and the belief that you can actually change your financial situation.

The psychological impact of failed budgeting attempts creates a vicious cycle. You try to budget, make critical mistakes, watch your plan fall apart, feel defeated, and then avoid budgeting altogether. This pattern keeps millions of Americans living paycheck to paycheck, even when they earn comfortable incomes.[1]

Financial wellness isn’t about perfection—it’s about avoiding the major pitfalls that derail progress. That’s exactly what we’re going to address in this comprehensive guide. Each mistake we’ll cover represents a real barrier that I’ve either experienced myself or witnessed countless others struggle with.

The Top 10 Budgeting Mistakes to Avoid in 2025

1. Not Tracking Your Actual Spending Patterns

This is the granddaddy of all budgeting mistakes. You cannot manage what you don’t measure. Period.

Here’s what happens: You estimate that you spend about $300 on groceries each month. Seems reasonable, right? But when you actually track your spending for 30 days, you discover you’re spending $450—and that doesn’t even include the “quick stops” at convenience stores or those DoorDash orders you mentally categorized as “occasional treats.”

The $3 Coffee Problem ☕

Let me give you a concrete example that illustrates why expense tracking is critical. That daily $3 coffee seems harmless—it’s just three bucks, right? But here’s the math that changes everything:

- $3 per day × 20 workdays = $60 per month

- Add weekend coffee runs (2 per week × 4 weeks × $5) = $40 per month

- Total: $100 per month or $1,200 per year

I’m not saying you should never buy coffee. I’m saying you need to know that you’re spending $1,200 annually on it and make that choice consciously. When you track expenses, you can decide if that coffee brings you $1,200 worth of joy—or if you’d rather redirect some of that money toward building debt-free habits.

How to Actually Track Spending:

- Review the past 12 months of bank and credit card statements

- Categorize every transaction (housing, food, transportation, entertainment, etc.)

- Identify patterns in recurring and one-off costs

- Use technology like budgeting apps to automate tracking going forward

The key insight here is that analyzing your actual spending patterns reveals the truth about your money habits. Estimating creates a fantasy budget that exists only on paper.

2. Budgeting Based on Gross Income Instead of Net Take-Home Pay

This mistake sets you up for failure before you even start. Your gross income is what you earn before taxes, retirement contributions, health insurance, and other deductions. Your net income is what actually hits your bank account.

The Reality Check:

If you earn $60,000 annually, your gross monthly income is $5,000. But after federal taxes, state taxes, Social Security, Medicare, 401(k) contributions, and health insurance, your actual take-home might be closer to $3,600. That’s a $1,400 difference every single month.[2]

When you budget based on that $5,000 figure, you’re allocating money you’ll never see. This creates an immediate shortfall that makes your budget impossible to follow.

“The most common budgeting mistake I see is people planning their expenses based on what they earn before taxes and deductions. This fundamental error makes every other budgeting decision wrong from the start.” — Financial Planning Expert

The Fix:

- Pull up your most recent pay stub or direct deposit history

- Use your actual net income as your budgeting baseline

- If your income varies, use the average of your last 3-6 months of take-home pay

- Build your entire budget around money you actually receive

This single shift—budgeting on net instead of gross—eliminates a major source of budget failure and creates a realistic foundation for your financial plan.

3. Setting Unrealistic Savings Goals That Guarantee Burnout

I’ve seen this pattern repeatedly: Someone gets inspired to change their finances, reads about aggressive savings strategies, and decides to save 50% of their income starting immediately. Within three weeks, they’ve given up entirely.

The Burnout Cycle:

Highly restrictive budgets create psychological pressure that leads to impulsive spending. It’s the financial equivalent of crash dieting—you deprive yourself so severely that you eventually binge and undo all your progress.

The SMART Goal Framework for Budgeting:

Instead of setting arbitrary, aggressive targets, use the SMART method to create sustainable goals:

- Specific: “Save $500 for an emergency fund” (not “save more money”)

- Measurable: Track progress with concrete numbers

- Achievable: Start with 5-10% of income, not 50%

- Relevant: Align with your actual financial priorities

- Time-bound: Set a realistic deadline (e.g., “in 6 months”)

Real Example:

Instead of: “I’m going to save $10,000 this year by cutting all entertainment and eating only rice and beans.”

Try: “I’m going to save $2,000 in the next 12 months by automatically transferring $167 per month to my savings account and reducing restaurant spending by $100 monthly.”

The second goal is achievable and sustainable. The first is a recipe for failure. If you want to see how realistic goal-setting can lead to significant savings, check out these proven savings strategy hacks.

4. Ignoring Irregular and Unexpected Expenses

This is the budgeting mistake that catches people off guard every single time. You create a beautiful monthly budget that accounts for rent, utilities, groceries, and gas. Everything balances perfectly. Then December arrives with holiday gifts, or your car needs a $800 repair, or you get hit with an annual insurance premium—and your entire budget collapses.

The Sinking Fund Solution 💰

A sinking fund is a simple but powerful concept: you divide large, irregular expenses by 12 months and save that amount monthly. This transforms unpredictable financial bombs into manageable, planned expenses.

Common Irregular Expenses to Plan For:

| Expense Category | Annual Cost | Monthly Sinking Fund |

|---|---|---|

| Car Maintenance/Repairs | $1,200 | $100 |

| Holiday Gifts | $600 | $50 |

| Annual Insurance Premiums | $1,800 | $150 |

| Home Repairs | $1,200 | $100 |

| Medical Deductibles | $1,500 | $125 |

| Total | $6,300 | $525 |

When you don’t plan for these expenses, a single $800 car repair feels like a financial emergency. When you’ve been setting aside $100 monthly in a car maintenance sinking fund, that same repair is just a planned expense you’ve already saved for.

Implementation Steps:

- List all irregular expenses you’ve had in the past 2-3 years

- Estimate annual costs for each category

- Divide by 12 to get monthly sinking fund amounts

- Open separate savings accounts or use budgeting apps with category tracking

- Automatically transfer sinking fund amounts each month

This approach prevents financial surprises and keeps your budget intact even when life happens.

5. Failing to Build Even a Small Emergency Fund

Here’s a sobering statistic: Nearly 40% of Americans couldn’t cover a $400 emergency expense without borrowing money or selling something.[3] This is one of the most critical budgeting mistakes to avoid because it creates a domino effect of financial problems.

Why Emergency Funds Matter:

Without an emergency fund, a single unexpected expense—a medical bill, car repair, or broken appliance—forces you to choose between:

- Going into credit card debt

- Missing other bill payments

- Borrowing from friends or family

- Taking out a payday loan

Each option creates additional financial stress and pushes you deeper into the paycheck-to-paycheck cycle.

The $500 Starter Emergency Fund 🚨

You don’t need to save six months of expenses right away. That’s overwhelming and unrealistic when you’re just starting. Instead, focus on building a modest $500 emergency fund first.

Why $500? Research shows this amount covers most minor emergencies:

- Urgent care visit: $150-$300

- Minor car repair: $200-$400

- Broken appliance repair: $100-$300

- Emergency travel: $200-$500

Your Emergency Fund Roadmap:

Phase 1: Save $500 (covers most minor emergencies)

Phase 2: Build to $1,000 (covers moderate emergencies)

Phase 3: Reach 1 month of expenses (provides breathing room)

Phase 4: Grow to 3-6 months of expenses (full financial security)

The key is starting small and building momentum. Even $500 transforms your financial resilience and prevents single unexpected expenses from derailing your entire budget.

6. Relying Too Heavily on Credit Cards Without Tracking Cash Flow

Credit cards create a dangerous psychological disconnection from your actual spending. When you swipe a card, you don’t feel the immediate impact the same way you do when handing over cash. This disconnect masks true spending patterns and creates debt cycles that keep you living paycheck to paycheck.

The Credit Card Illusion:

Here’s what happens: You charge $150 for groceries, $80 for gas, $60 for dinner out, and $40 for online shopping throughout the week. It feels manageable because you’re not seeing money leave your account. Then the credit card bill arrives at $1,200, and you can only afford to pay $400, leaving an $800 balance that starts accruing 18-24% interest.

The Real Cost of Minimum Payments:

If you carry a $5,000 credit card balance at 20% APR and make only minimum payments (typically 2-3% of the balance), you’ll:

- Pay for approximately 15 years

- Spend over $6,000 in interest alone

- More than double the original purchase price

Breaking the Credit Card Cycle:

- Track credit card spending in real-time using your budgeting app

- Treat credit cards like debit cards—only charge what you can pay off immediately

- Review statements weekly instead of waiting for the monthly bill

- Set up balance alerts to stay aware of accumulating charges

- Use cash or debit for discretionary spending to feel the psychological impact

I’m not saying credit cards are evil—they offer rewards, fraud protection, and convenience. But you must track credit spending with the same rigor as cash spending, or you’ll lose visibility into your actual cash flow.

For comprehensive guidance on eliminating existing credit card debt, explore this step-by-step debt-free plan.

7. Not Allowing Any Flexibility for Discretionary Spending

This might seem counterintuitive, but one of the biggest budgeting mistakes to avoid is creating a budget that’s too restrictive. When you eliminate all discretionary spending and fun from your budget, you’re setting yourself up for psychological burnout and eventual rebellion.

The Deprivation-Binge Cycle:

Think about extreme diets. When you completely eliminate foods you enjoy, what happens? You eventually crack and binge on exactly what you’ve been denying yourself. The same psychological pattern applies to budgeting.

The 50/30/20 Rule with Flexibility:

A popular and sustainable budgeting framework is:

- 50% for needs (housing, utilities, groceries, transportation)

- 30% for wants (entertainment, dining out, hobbies)

- 20% for savings and debt repayment

Notice that 30% is allocated to wants—things that bring you joy but aren’t essential. This flexibility is crucial for long-term success.

Building in “Fun Money” 🎉

Even if you can’t allocate 30% to wants right now, include some discretionary spending in your budget:

- $50-100 monthly for entertainment

- A coffee budget if that’s important to you

- Money for hobbies that bring genuine happiness

- Occasional dining out with friends or family

The key is making these choices consciously rather than restricting everything and then overspending impulsively when you reach your breaking point.

“The best budget is one you can actually stick to for years, not one that’s perfect on paper but impossible to maintain in real life.”

When you allow flexibility in areas that align with your values and priorities, you maintain motivation and avoid the burnout that causes people to abandon budgeting altogether.

8. Overlooking Subscription Creep and Recurring Charges

This is a modern budgeting mistake that’s becoming increasingly common in 2025. Subscription services have exploded—streaming platforms, meal kits, apps, software, gym memberships, beauty boxes, gaming services, and countless others. Each one seems affordable individually, but collectively they drain hundreds of dollars monthly without you noticing.

The Subscription Trap:

- Netflix: $15.49/month

- Spotify: $10.99/month

- Amazon Prime: $14.99/month

- Gym membership: $50/month

- Meal kit service: $60/month

- Cloud storage: $9.99/month

- Gaming subscription: $14.99/month

- Beauty box: $25/month

- News subscription: $12/month

- Total: $214.44/month or $2,573.28/year

Many people have subscriptions they’ve completely forgotten about or services they signed up for during free trials and never canceled.

The Subscription Audit Process:

- Review 3 months of bank and credit card statements

- Highlight every recurring charge, no matter how small

- List all subscriptions with costs and usage

- Ask: “Do I actively use this? Does it bring value equal to its cost?”

- Cancel anything you don’t use weekly or monthly

- Set calendar reminders before annual renewals to reassess

Using Technology to Combat Subscription Creep:

Apps like Rocket Money (formerly Truebill) automatically identify subscriptions, track spending patterns, and help you cancel unwanted services. These tools reveal the true scope of your recurring charges and make it easy to trim unnecessary expenses.

The 30-Day Rule:

Before adding any new subscription, commit to a 30-day waiting period. This cooling-off period prevents impulsive sign-ups and helps you determine if you genuinely need the service or if it’s just appealing in the moment.

Eliminating just $100 in unused subscriptions creates $1,200 annually that can be redirected toward emergency savings, debt repayment, or financial goals that actually matter to you.

9. Ignoring the Impact of Inflation on Your Budget

This is a critical budgeting mistake that became painfully obvious in recent years. Inflation erodes your purchasing power, meaning the same budget that worked last year doesn’t stretch as far this year. In 2025, accounting for rising costs is essential for realistic budget planning.

The Inflation Reality:

From 2021 to 2023, Americans experienced inflation rates not seen in decades:

- Groceries increased 20-30% in many categories

- Gas prices fluctuated dramatically

- Housing costs rose significantly

- Healthcare expenses continued climbing

If you’re using a budget you created two years ago without adjusting for inflation, you’re underfunding essential categories and wondering why you’re constantly over budget.[4]

Inflation-Proofing Your 2025 Budget:

- Review and increase budget allocations for categories most affected by inflation (groceries, gas, utilities)

- Track price changes in items you buy regularly

- Adjust spending or find substitutes when prices rise significantly

- Build a buffer (5-10% extra) in variable expense categories

- Negotiate fixed expenses annually (insurance, phone plans, internet)

The Income-Inflation Gap:

Here’s the challenge: inflation affects everyone, but wage increases don’t keep pace for most workers. If inflation is 6% but your income only increased 3%, you’ve effectively taken a 3% pay cut in purchasing power.

Strategies to Combat This Gap:

- Increase income through side hustles, skill development, or job changes

- Reduce discretionary spending in lower-priority areas

- Shop strategically using sales, bulk buying, and generic brands

- Eliminate waste to maximize the value of every dollar

Ignoring inflation means your budget becomes increasingly unrealistic over time. Acknowledging and planning for rising costs keeps your budget grounded in current economic reality.

10. Not Adjusting Your Budget When Income Increases

This final budgeting mistake is particularly insidious because it feels good in the moment but sabotages long-term financial stability. It’s called “lifestyle inflation” or “lifestyle creep,” and it’s why many high earners still live paycheck to paycheck.

The Lifestyle Inflation Trap:

You get a raise, promotion, or new job with higher pay. Suddenly you have more money coming in each month. What happens next?

- You upgrade your apartment or buy a bigger house

- You lease a nicer car

- You increase restaurant spending

- You add more subscriptions and services

- You buy higher-end everything

Within months, your expenses have risen to match (or exceed) your new income, and you’re back to living paycheck to paycheck—just at a higher income level.

The Opportunity Cost:

Here’s what most people miss: Income increases represent the single best opportunity to build wealth and financial security. When you immediately spend every dollar of a raise, you waste this opportunity.

The 50/50 Rule for Raises 📈

When your income increases, use this simple framework:

- 50% toward lifestyle improvements (if desired)

- 50% toward financial goals (savings, investments, debt repayment)

Real Example:

You get a $5,000 annual raise ($417 more per month after taxes):

- $208 can enhance your lifestyle (nicer apartment, better car, more entertainment)

- $208 automatically goes to savings, investments, or debt payoff

This approach allows you to enjoy the fruits of your hard work while simultaneously building financial security. Over time, the 50% you’re saving compounds and creates real wealth.

Automating the Process:

The key to making this work is automation:

- Calculate your net income increase

- Immediately set up automatic transfers for 50% to savings/investments

- Adjust your budget to allocate the remaining 50%

- Never touch the automated savings for lifestyle expenses

When you automate savings before you see the money, you avoid the temptation to spend it all. This single habit—capturing half of every income increase—can transform your financial trajectory over a decade.

Measuring Outcomes, Not Just Participation:

High participation in savings programs doesn’t guarantee results. What matters is the actual outcome—the dollar amount you’ve saved and invested. Track your net worth quarterly to ensure your budgeting efforts are creating real financial progress, not just activity.

The Psychology Behind Budgeting Mistakes

Understanding why we make these budgeting mistakes is just as important as knowing what they are. Behavioral economics reveals that humans are fundamentally irrational when it comes to money decisions.

Common Psychological Barriers:

🧠 Present Bias: We overvalue immediate gratification and undervalue future benefits. That’s why spending $50 on dinner tonight feels better than saving $50 for retirement in 30 years.

🧠 Mental Accounting: We treat money differently based on arbitrary categories. We might refuse to spend $100 on a quality item we need but easily spend $100 on impulse purchases throughout the month.

🧠 Loss Aversion: We feel the pain of losing $100 more intensely than the pleasure of gaining $100. This makes budgeting feel like deprivation rather than empowerment.

🧠 Optimism Bias: We believe we’ll be more disciplined in the future than we actually are. “I’ll start budgeting seriously next month” becomes a perpetual promise.

Overcoming Psychological Barriers:

- Automate everything possible to remove willpower from the equation

- Make savings visible with progress trackers and visual goals

- Reframe budgeting as permission to spend, not restriction

- Use commitment devices like automatic transfers you can’t easily reverse

- Celebrate small wins to build positive associations with budgeting

Understanding these psychological patterns helps you design budgets that work with human nature rather than against it. For more insights on building sustainable financial habits, visit MSBudget’s homepage.

Technology Tools for Avoiding Budgeting Mistakes in 2025

The good news is that technology has made avoiding budgeting mistakes easier than ever. Here are the categories of tools that can transform your budgeting success:

Budget Tracking Apps:

- Automatically categorize transactions

- Provide real-time spending alerts

- Visualize spending patterns

- Track progress toward goals

Subscription Management Tools:

- Identify all recurring charges

- Cancel unwanted subscriptions with one click

- Negotiate better rates on services

- Alert you before renewals

Cash Flow Projection Software:

- Forecast future account balances

- Anticipate irregular expenses

- Prevent overdrafts and shortfalls

- Plan for seasonal income variations

Automated Savings Apps:

- Round up purchases and save the difference

- Analyze spending and save surplus automatically

- Set rules-based savings (save $10 every time you eat out)

- Make saving effortless and invisible

Investment Automation Platforms:

- Auto-invest income increases before you see them

- Rebalance portfolios automatically

- Minimize taxes through strategic placement

- Remove emotional decision-making

The key is choosing tools that match your specific budgeting challenges and actually using them consistently. Technology can’t fix budgeting mistakes if you don’t engage with it regularly.

Creating a Personalized Budget That Actually Works

Now that you understand the major budgeting mistakes to avoid, let’s talk about creating a budget that fits your unique situation, personality, and goals.

Different Budgeting Methods for Different People:

Zero-Based Budget: Every dollar is assigned a job. Income minus expenses equals zero. Best for people who want complete control and detailed tracking.

50/30/20 Budget: 50% needs, 30% wants, 20% savings. Best for people who want simplicity and flexibility.

Envelope System: Cash allocated to physical or digital envelopes for each category. Best for people who overspend on credit cards.

Pay Yourself First: Automatically save/invest first, then spend what’s left. Best for people who struggle with traditional budgeting.

No-Budget Budget: Track spending and set loose guidelines rather than strict limits. Best for naturally frugal people who feel restricted by traditional budgets.

Finding Your Method:

Consider your personality type:

- Detail-oriented? Try zero-based budgeting

- Big-picture thinker? Try 50/30/20

- Struggle with credit cards? Try the envelope system

- Hate budgeting? Try pay-yourself-first or no-budget approaches

There’s no single “right” way to budget. The right method is the one you’ll actually stick with for years.

Your 30-Day Budget Implementation Plan:

Week 1: Track every expense without judgment. Just observe your current patterns.

Week 2: Categorize expenses and calculate your baseline spending in each category.

Week 3: Choose a budgeting method and create your first budget using actual spending data.

Week 4: Implement your budget, track daily, and adjust as you discover what works and what doesn’t.

Month 2+: Refine your budget based on real-world experience. Adjust categories, amounts, and methods until you find your sustainable system.

Long-Term Financial Mindset Development

Avoiding budgeting mistakes isn’t just about tactics and tools—it’s about developing a healthy financial mindset that serves you for decades.

Shifting from Scarcity to Abundance Thinking:

Scarcity mindset: “I can’t afford anything. Budgeting means deprivation.”

Abundance mindset: “I’m choosing to allocate my resources toward what matters most. Budgeting gives me permission to spend on my priorities.”

The Growth Mindset in Personal Finance:

Fixed mindset: “I’m just bad with money. I’ll never be good at budgeting.”

Growth mindset: “I’m learning to manage money better. Each mistake teaches me something valuable.”

Building Financial Confidence:

- Start with small wins that build momentum

- Track progress to see tangible improvement

- Learn from setbacks without self-judgment

- Surround yourself with financially healthy people

- Invest in financial education through books, courses, and resources

The Compound Effect of Small Changes:

Remember that small, consistent improvements compound over time:

- Eliminating $100 in monthly subscriptions = $1,200 annually

- Saving an extra $200 monthly = $2,400 annually

- Investing that $2,400 at 8% returns for 30 years = over $272,000

The budgeting mistakes you avoid today create exponential benefits over decades.

Conclusion: Your Path to Breaking the Paycheck-to-Paycheck Cycle

Living paycheck to paycheck isn’t about how much you earn—it’s about the budgeting mistakes that keep you trapped in a cycle of financial stress. By avoiding these 10 critical errors, you can transform your financial situation regardless of your current income level.

Let’s recap the budgeting mistakes to avoid:

- ✅ Not tracking actual spending patterns

- ✅ Budgeting on gross income instead of net pay

- ✅ Setting unrealistic savings goals

- ✅ Ignoring irregular and unexpected expenses

- ✅ Failing to build an emergency fund

- ✅ Relying too heavily on credit cards

- ✅ Creating overly restrictive budgets

- ✅ Overlooking subscription creep

- ✅ Ignoring inflation’s impact

- ✅ Not adjusting budgets when income increases

Your Action Plan for the Next 30 Days:

This Week:

- Track every expense without judgment

- Calculate your actual net take-home pay

- Review 3 months of bank statements for subscriptions

Next Week:

- Choose a budgeting method that fits your personality

- Create your first budget based on actual spending data

- Set up one automatic savings transfer (even if it’s just $25)

Week 3:

- Start a $500 emergency fund

- Create sinking funds for irregular expenses

- Cancel at least one unused subscription

Week 4:

- Evaluate what’s working and what needs adjustment

- Celebrate your progress (no matter how small)

- Commit to reviewing and refining your budget monthly

Remember: The goal isn’t perfection. The goal is progress. Every budgeting mistake you avoid is a step toward financial freedom, security, and the ability to build wealth over time.

You don’t need to be perfect at budgeting—you just need to be better than you were last month. Start with one change, build momentum, and watch as small improvements compound into life-changing results.

The paycheck-to-paycheck cycle ends when you decide it ends. Make that decision today, avoid these critical budgeting mistakes, and take control of your financial future in 2025.