When my car broke down on a Tuesday morning and the repair bill came to $1,400, I didn’t panic. I didn’t reach for a credit card or stress about which bill to skip. I simply transferred money from my emergency fund and went about my day. That’s the power of learning how to create a family budget that actually prepares you for life’s curveballs.

Most families think budgeting is about restriction and saying “no” to everything fun. But here’s what I’ve learned: how to create a family budget is really about building a financial safety net that lets you sleep soundly at night, even when unexpected expenses pop up (and they always do).

Key Takeaways

- Start with a $1,000 emergency fund before tackling other financial goals to break the cycle of emergency borrowing

- Use the 50/30/20 rule as a framework: 50% for needs, 30% for wants, and 20% for savings and debt repayment

- Build your budget on actual spending data from the past three months, not idealized guesses about what you think you spend

- Automate your savings by setting up transfers on payday so emergency funds grow without requiring willpower

- Review and adjust monthly because budgets aren’t set-it-and-forget-it tools—they’re living documents that evolve with your life

Quick Answer

How to create a family budget that survives emergencies starts with tracking your actual spending for three months, categorizing expenses into needs (50%), wants (30%), and savings (20%), then building a starter emergency fund of $1,000 before expanding to 3-6 months of essential expenses. The key is automating savings transfers on payday and reviewing your budget monthly to adjust for real life changes, not creating a perfect plan that sits unused in a drawer.

Why Most Family Budgets Fail During Emergencies

Most family budgets collapse the moment an unexpected expense appears because they’re built on wishful thinking rather than reality. Families create beautiful spreadsheets showing exactly where every dollar should go, but they forget to plan for the car repair, the broken water heater, or the emergency dental visit.

According to a January 2026 Bankrate survey, only 47% of Americans have sufficient emergency funds to cover a $1,000 expense, despite the average emergency expense reaching approximately $1,700.[2] Even more concerning, the Federal Reserve’s Survey of Household Economics and Decision Making shows that 37% of U.S. adults struggle to cover a $400 emergency expense without borrowing or selling assets.[6]

Here’s what makes budgets fail:

- No buffer zone between income and expenses, leaving zero room for surprises

- Treating irregular expenses as emergencies instead of planning for predictable costs like car registration or holiday shopping

- Saving “whatever’s left” at the end of the month (which is usually nothing)

- Creating unrealistic spending targets that don’t match actual habits

- Giving up after one bad month instead of adjusting and continuing

The solution isn’t a more complicated budget. It’s a budget designed with emergencies already built into the plan, plus a separate emergency fund that acts as your financial shock absorber.

How to Create a Family Budget: The Foundation Steps

Creating a family budget that actually works starts with understanding where your money currently goes, not where you wish it went. This foundation takes about two hours of focused work, but it sets you up for years of financial stability.

Step 1: Gather three months of spending data

Pull your bank statements, credit card statements, and cash spending records from the past 90 days. This gives you real numbers instead of guesses. Look for patterns in categories like groceries, gas, dining out, subscriptions, and miscellaneous purchases.[4]

Step 2: Calculate your total monthly income

Add up all sources of income after taxes: paychecks, side hustles, child support, rental income, or any other money coming in. If your income varies, use the lowest month from the past six months as your baseline. This conservative approach prevents overspending during lean months.

Step 3: Categorize your expenses into three buckets

Organize everything into these categories:[4]

- Fixed Expenses: Housing (rent/mortgage), insurance, utilities, childcare, car payments, minimum debt payments

- Variable Expenses: Groceries, gas, dining out, entertainment, clothing, personal care

- Savings + Debt Repayment: Emergency fund contributions, retirement accounts, extra debt payments

Step 4: Apply the 50/30/20 framework

Use this proven allocation as your starting point: 50% for needs, 30% for wants, and 20% for savings and debt payoff.[6] If your numbers don’t fit this framework initially, don’t panic. It’s a target to work toward, not a requirement for day one.

Step 5: Account for irregular but predictable expenses

List annual or semi-annual costs like vehicle registration, property taxes, insurance premiums, holiday shopping, back-to-school supplies, and home maintenance. Divide each by 12 and add that monthly amount to your budget.[4] This prevents these expenses from derailing your plan when they arrive.

For families managing biweekly paychecks, this foundation becomes even more important because you need to align your budget cycles with your actual income timing.

Building Your Emergency Fund Layer by Layer

An emergency fund isn’t a nice-to-have luxury. It’s the difference between a budget that survives tough times and one that crumbles at the first unexpected expense. Financial experts recommend building this fund in stages rather than trying to save everything at once.[1]

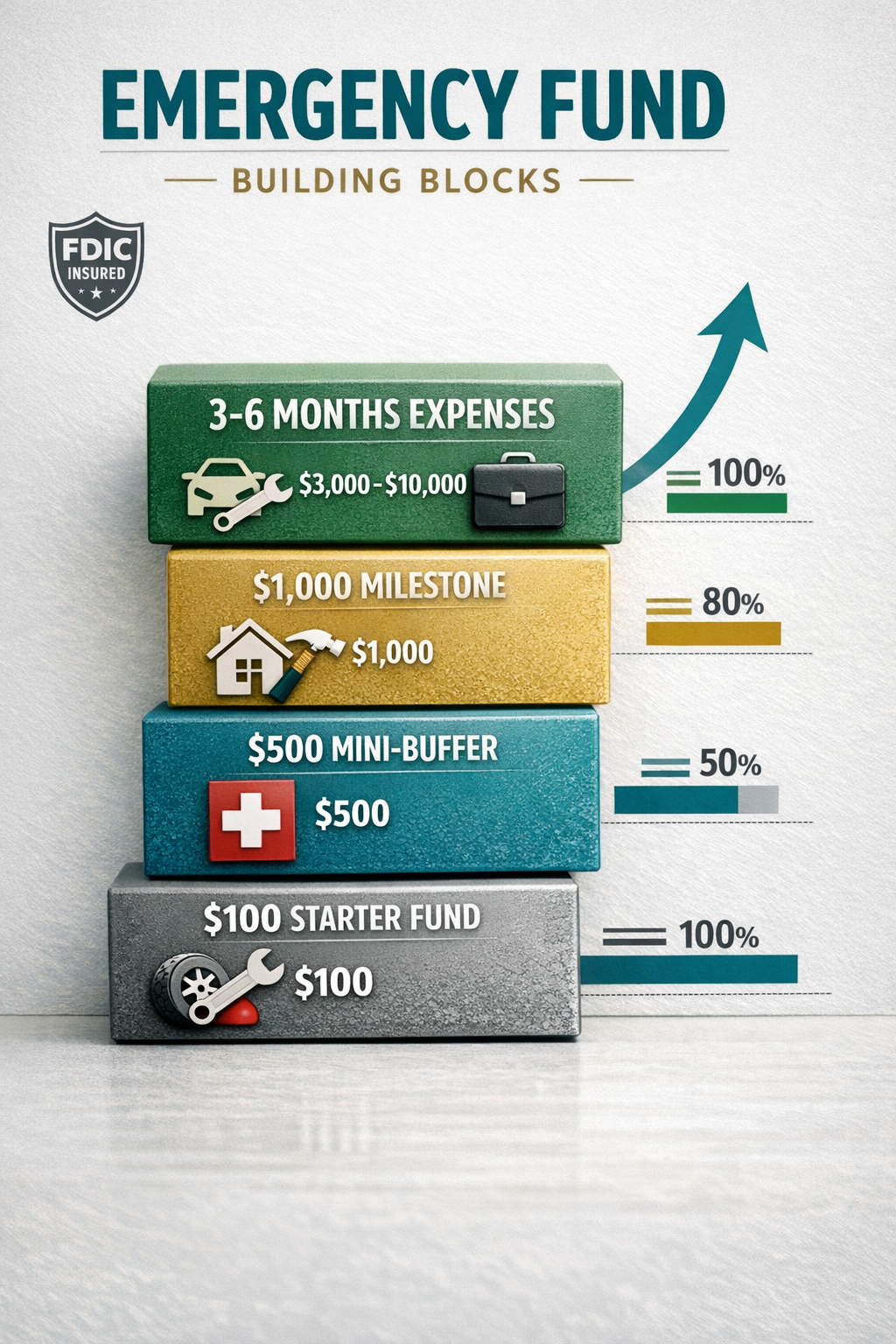

Stage 1: The $1,000 Starter Fund

Your first milestone is $1,000 in a separate savings account. This starter emergency fund stops the cycle of reaching for credit cards when the car needs new brakes or the furnace breaks in January.[1] Even if you have debt, pause extra payments temporarily to build this buffer first.

How to get there:

- Save $50 per paycheck if you’re paid biweekly (20 paychecks = $1,000)

- Cut one major discretionary expense for 2-3 months

- Redirect any windfalls like tax refunds or bonuses

- Use savings strategy hacks to accelerate progress

Stage 2: The 3-6 Month Life Buffer

Once you’ve cleared high-interest debt, expand your emergency fund to cover 3-6 months of essential expenses. This means housing, utilities, food, insurance, transportation, and minimum debt payments—not your full spending including wants.[5]

The target varies by household:[2]

- 3 months for dual-income households with stable jobs

- 6 months for single-income households

- 6+ months for variable income, self-employment, or households with dependents who have special needs

Stage 3: Specialized Emergency Reserves

Some families benefit from additional targeted savings beyond the standard emergency fund:

- Medical deductible fund if you have a high-deductible health plan

- Home repair reserve for homeowners (1% of home value annually)

- Vehicle replacement fund if you drive an older car

Starting amounts as small as $100 create the savings habit, and consistency matters more than the initial size.[2] Even $20 per week builds momentum and proves to yourself that you can do this.[3]

The psychological benefit of an emergency fund extends beyond just having money available. It creates mental space to make better long-term decisions about career moves, investments, and major purchases without fear that one missed paycheck will collapse your household.[1]

How to Create a Family Budget That Adapts to Income Changes

Income rarely stays perfectly steady. Bonuses arrive, overtime hours fluctuate, side hustles grow or shrink, and job changes happen. A budget that survives emergencies must flex with these income variations rather than breaking.

For variable income households:

Build your budget on your lowest typical monthly income from the past year. When higher-income months arrive, allocate the surplus using this priority order:

- Top up emergency fund to target level

- Make extra debt payments

- Fund irregular expense categories (holidays, maintenance)

- Increase retirement contributions

- Enjoy guilt-free spending on wants

For sudden income increases (raises, bonuses):

Avoid lifestyle inflation by immediately redirecting at least 50% of any raise to savings or debt payoff before your spending habits adjust upward. If you get a $200 monthly raise, automatically transfer $100 to savings and allow yourself to enjoy the other $100.

For income decreases or job loss:

This is where your emergency fund proves its worth. Immediately switch to a bare-bones budget covering only the needs category (50% in the standard framework). Pause all want spending and savings contributions temporarily. Your emergency fund covers the gap while you adjust.

Review these budget items when income drops:

- Negotiate lower rates on insurance, phone plans, internet

- Pause subscription services (streaming, gym, meal kits)

- Switch to generic brands for groceries and household items

- Defer all non-essential purchases

- Consider temporary income sources from side hustles

The key is making these adjustments proactively based on your new reality rather than continuing to spend at previous levels and hoping things work out.

Separating Needs from Wants Without Feeling Deprived

One of the hardest parts of learning how to create a family budget is honestly categorizing expenses as needs versus wants. This distinction becomes critical during emergencies when you need to cut spending quickly.

True needs (essential for basic living):

- Housing (rent, mortgage, property taxes)

- Utilities (electric, gas, water, basic internet)

- Food and groceries

- Basic transportation (car payment, gas, insurance, public transit)

- Health insurance and necessary medical care

- Basic clothing

- Minimum debt payments

Wants (enhance life but aren’t essential):

- Dining out and takeout

- Streaming services and entertainment subscriptions

- Cable TV packages

- Gym memberships (when home workouts are possible)

- New clothes beyond basic replacements

- Hobbies and recreation

- Vacation and travel

- Latest technology upgrades

The gray area (depends on your situation):

- Internet speed above basic (need if you work from home, want otherwise)

- Cell phone plans (basic service is a need, unlimited premium data is a want)

- Childcare (need if both parents work, want if one stays home)

- Pet expenses (basic vet care is a need once you have the pet, but getting the pet was a want)

Here’s the important part: wants aren’t bad. The 50/30/20 framework specifically allocates 30% of your budget to wants because life isn’t just about survival.[6] The goal is conscious spending on wants you truly value while having clarity about what you could cut during an emergency.

I’ve found that families who try to eliminate all wants from their budget typically burn out within two months. Instead, identify your highest-value wants (the things that genuinely make your life better) and cut the low-value wants (subscriptions you forgot about, impulse purchases you regret).

Check out these budgeting hacks for beginners to find ways to enjoy wants while staying within your 30% allocation.

Automating Your Budget to Remove Decision Fatigue

The most successful family budgets run on autopilot for routine transactions. Automation eliminates the daily decisions about whether to save, removes the temptation to skip a month, and ensures your emergency fund grows consistently.

Set up these automatic transfers on payday:

- Emergency fund contribution (even $50 per paycheck adds up to $1,300 annually for biweekly pay)

- Retirement account deposits (401k, IRA, or other investment accounts)

- Debt payments beyond minimums if you’re in payoff mode

- Irregular expense fund for predictable-but-annual costs

- Bills with fixed amounts (insurance, subscriptions, loan payments)

The “save first, spend second” principle:

Traditional budgeting advice says to save whatever’s left at month’s end. In reality, there’s rarely anything left. Instead, automatically transfer savings on payday before you have a chance to spend it.[4] This single change transforms savings from an afterthought into a priority.

Where to keep automated savings:

- Emergency fund: High-yield savings account separate from your checking account, offering 4-5% interest in 2026 while maintaining FDIC insurance protection[2]

- Irregular expenses: Separate savings account or subdivided accounts with labels for different purposes

- Short-term goals: Money market accounts or savings accounts

- Long-term goals: Retirement accounts, investment accounts, or 529 education savings

The physical and mental separation from your everyday checking account prevents you from “borrowing” from your emergency fund for non-emergencies.[2] If the money sits in checking, you’ll spend it. If it requires a transfer and a day’s wait, you’ll think twice.

Tools that help with automation:

- Your bank’s automatic transfer feature (free)

- Budgeting apps that round up purchases and save the difference

- Employer direct deposit split between checking and savings

- Credit card autopay for fixed bills (then pay the card in full monthly)

Start with small automated amounts if large transfers feel scary. The habit matters more than the amount. You can always increase transfers as you get comfortable with the system.

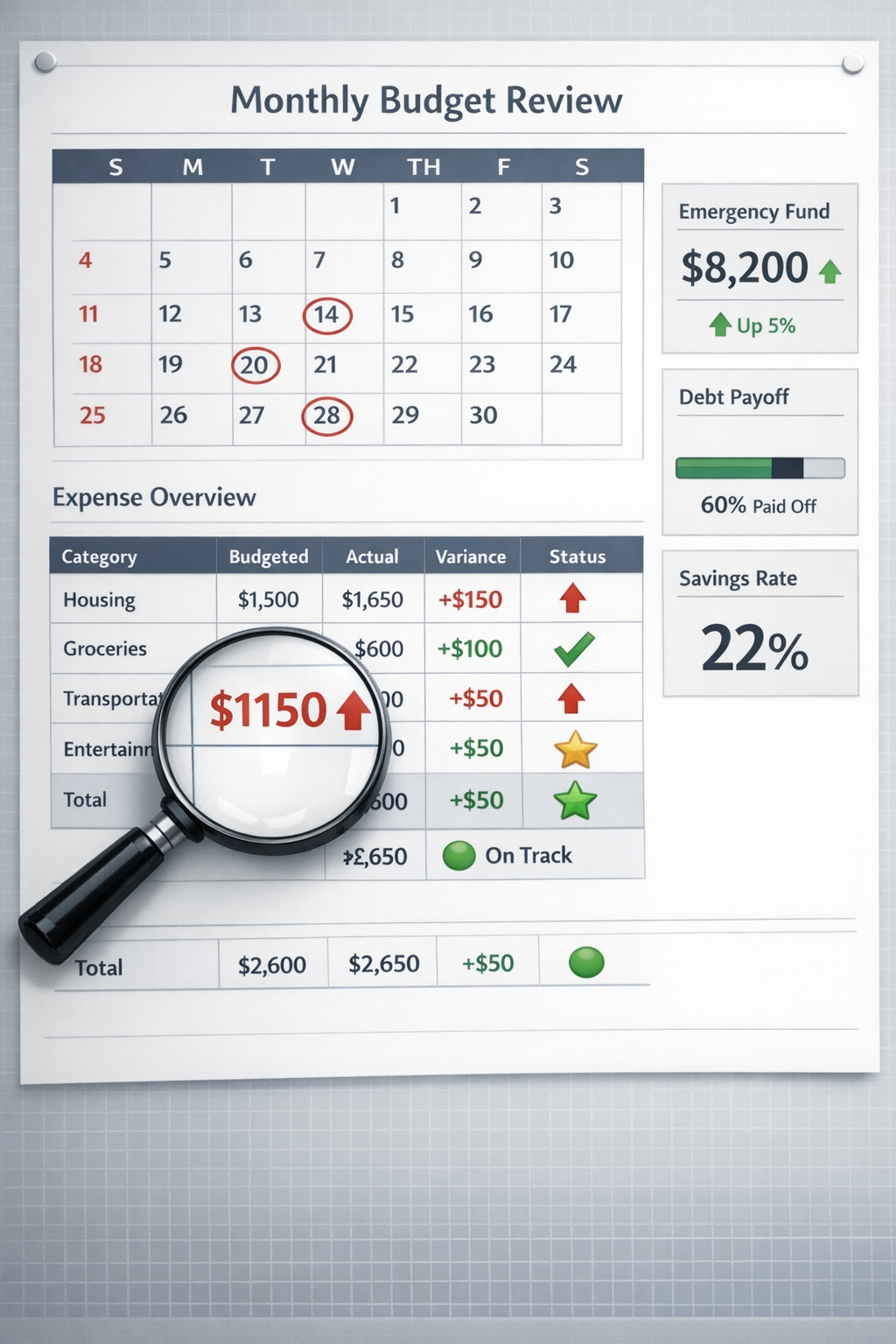

The Monthly Budget Review That Prevents Disaster

Creating a budget is step one. Maintaining it through monthly reviews is what actually keeps your family financially stable. Families don’t fail because they design bad budgets—they fail because they stop monitoring and adjusting.

Schedule a 30-minute monthly money meeting:

Pick the same day each month (I use the last Sunday) and review these key metrics:[4]

- Actual spending vs. budgeted amounts in each category

- Emergency fund balance and progress toward your target

- Debt balances and payoff progress if applicable

- Upcoming irregular expenses in the next 30-60 days

- Income changes or expected variations

What to do when you’re over budget:

Going over budget in a category isn’t failure—it’s data. Ask these questions:

- Was this a one-time unusual expense or a pattern?

- Did I underestimate this category when creating the budget?

- Can I reduce spending here next month, or do I need to adjust other categories?

- Should I create a new budget line item for this type of expense?

What to do when you’re under budget:

Celebrate, then redirect the surplus strategically:

- If emergency fund isn’t complete, transfer the surplus there

- If you have debt, make an extra payment

- If both are handled, increase retirement contributions or save for a specific goal

Red flags that require immediate budget adjustments:

- Emergency fund being tapped for non-emergencies

- Credit card balances growing month over month

- Consistently overspending in the same categories

- Stress or arguments about money increasing

- Avoiding looking at account balances

I’ve found that couples benefit from doing this review together, even if one person handles day-to-day transactions. It keeps both partners informed and aligned on financial priorities. For more guidance on managing money as a team, see this couples budgeting guide.

The monthly review also helps you avoid common budgeting mistakes that derail even well-intentioned plans.

Testing Your Budget Against Common Emergencies

A budget that looks perfect on paper might crumble when real emergencies strike. Test your budget’s resilience by running through these common scenarios and planning your response in advance.

Emergency Scenario 1: $1,500 car repair

- Ideal response: Pay from emergency fund, then rebuild fund over next 2-3 months

- If fund isn’t large enough: Pay what you can from fund, put remainder on 0% intro APR credit card, aggressively pay off within the promotional period

- Prevention: Budget $100 monthly for vehicle maintenance and repairs in your irregular expense category

Emergency Scenario 2: Job loss with 3-month gap before new employment

- Ideal response: Live on emergency fund covering essential needs only (housing, food, utilities, insurance, minimum debt payments)

- Budget adjustments: Immediately cut all want spending, pause retirement contributions, negotiate payment plans with creditors if needed, apply for unemployment benefits

- Prevention: Maintain 6-month emergency fund for single-income households, 3-month fund for dual-income

Emergency Scenario 3: $5,000 medical expense after insurance

- Ideal response: Pay from emergency fund or medical deductible fund if you’ve built one

- Alternative: Negotiate payment plan with medical provider (often 0% interest), pay from emergency fund over 12-24 months

- Prevention: Understand your health insurance deductible and out-of-pocket maximum, build these amounts into your emergency fund target

Emergency Scenario 4: Home repair (roof leak, HVAC failure) costing $3,000-$8,000

- Ideal response: Pay from emergency fund or dedicated home repair fund

- If fund is insufficient: Get multiple quotes, consider home equity line of credit for major repairs, evaluate whether repair can be staged over time

- Prevention: Homeowners should budget 1% of home value annually for maintenance and repairs

Emergency Scenario 5: Reduced work hours or pay cut

- Immediate response: Recalculate budget based on new lower income, identify which wants to eliminate temporarily, look for ways to reduce needs (refinance, switch insurance, negotiate bills)

- Medium-term: Explore side income opportunities, update resume, consider whether job change is needed

- Prevention: Keep emergency fund robust and avoid lifestyle inflation during high-income periods

Run through each scenario with your specific numbers. Can your current emergency fund handle it? If not, how close are you? What would you cut first? Having these answers before crisis hits removes panic from the equation.

Adjusting Your Budget as Your Family Grows and Changes

Life doesn’t stand still, and neither should your budget. Family changes like having children, kids starting school, caring for aging parents, or launching adult children all require budget adjustments.

When a baby arrives:

New expenses include diapers ($70-80 monthly), formula if not breastfeeding ($150-200 monthly), childcare ($200-2,000 monthly depending on location and type), increased medical costs, and baby gear. Many families also face reduced income if one parent takes unpaid leave or reduces hours.

Budget adjustments:

- Increase emergency fund target to 6 months due to increased household vulnerability

- Add childcare as a fixed need expense

- Reduce want spending temporarily to accommodate new needs

- Review health insurance and life insurance coverage

- Start or increase 529 education savings if possible

When kids start school:

School brings new costs like supplies, fees, activities, sports, school lunches, and clothing. It may also allow a stay-at-home parent to return to work or increase hours.

Budget adjustments:

- Create an annual school expense category and fund it monthly

- Budget for extracurricular activities separately from general entertainment

- If income increases with parent returning to work, allocate at least 50% to savings/debt before increasing lifestyle spending

When caring for aging parents:

Supporting elderly parents can include direct financial assistance, medical expenses, home modifications, or caregiver costs. This often happens during peak earning years when you’re also saving for retirement.

Budget adjustments:

- Assess total support costs and create a dedicated budget category

- Explore whether parent qualifies for Medicaid, veterans benefits, or other assistance

- Consider whether combining households makes financial sense

- Maintain your own emergency fund and retirement savings if possible—you can’t pour from an empty cup

When kids leave home:

The empty nest phase often brings reduced expenses for food, utilities, insurance, and activities, creating an opportunity to accelerate financial goals.

Budget adjustments:

- Redirect former kid expenses to retirement savings (you’re in the final stretch)

- Boost emergency fund if it’s below target

- Pay off remaining mortgage or other debt

- Avoid lifestyle inflation just because you have extra room in the budget

Each life transition requires a budget reset. Schedule a comprehensive budget review whenever major life changes occur, not just during your regular monthly check-ins.

Common Budget-Busting Traps and How to Avoid Them

Even well-designed budgets face predictable challenges. Knowing these traps in advance helps you plan around them instead of falling victim.

Trap 1: The “small purchase” leak

Daily coffee runs, vending machine snacks, app purchases, and impulse Amazon orders feel insignificant individually but drain $200-500 monthly. These purchases often don’t even register as spending in your mind.

Solution: Track every purchase for one week using a notes app on your phone. You’ll be shocked at how much the small stuff adds up. Then choose one or two small indulgences you truly enjoy and eliminate the rest.

Trap 2: Lifestyle inflation

Every raise, bonus, or debt payoff creates breathing room in your budget. The natural tendency is to immediately increase spending to fill that space. Within months, you’re back to living paycheck to paycheck despite earning more.

Solution: Implement the 50/50 rule for any income increase. Automatically redirect 50% to savings or debt payoff before adjusting your lifestyle spending. This lets you enjoy some improvement in quality of life while still making financial progress.

Trap 3: Treating credit card rewards as “free money”

Cashback and points feel like bonuses, encouraging additional spending to “maximize rewards.” Research shows people spend 12-18% more when using credit cards versus cash, often negating the 1-2% rewards.

Solution: Use rewards cards only for budgeted purchases you’d make anyway. Treat rewards as a bonus to put toward savings or debt, not as justification for additional spending. Learn more credit card strategies that actually build wealth.

Trap 4: The “special occasion” exception

Birthdays, holidays, graduations, weddings, and other celebrations create pressure to overspend beyond your budget. These events are predictable yet somehow always feel like surprises.

Solution: Create a gift and celebration category in your budget funded year-round. Estimate annual spending on all gifts and events, divide by 12, and set that amount aside monthly. When occasions arrive, you have dedicated funds waiting.

Trap 5: Comparing your budget to others

Your neighbor’s new car, your friend’s vacation photos, or your coworker’s home renovation can make your budget feel restrictive and unfair. Social comparison is the enemy of contentment and budget adherence.

Solution: Focus on your own financial goals and values. Define what matters most to your family and allocate your want spending there, ignoring what others prioritize. Remember that you’re seeing others’ highlight reels, not their credit card statements or stress levels.

Trap 6: All-or-nothing thinking

One overspending day or week makes you feel like you’ve “blown the budget,” leading to abandoning the whole plan. This perfectionism trap prevents many families from ever developing lasting budget habits.

Solution: Expect imperfection. A budget is a guide, not a prison sentence. When you overspend, simply adjust the rest of the month or make a note to course-correct next month. Progress, not perfection, is the goal. For more perspective, check out these good financial habits that matter more than perfect budgeting.

FAQ

How much should I have in my emergency fund?

Start with $1,000 as a starter emergency fund, then build to 3-6 months of essential expenses once high-interest debt is cleared. Dual-income households typically need 3 months, while single-income households should target 6 months. Households with variable income, self-employment, or special circumstances may need 6-12 months.[1][2][5]

Where should I keep my emergency fund?

Store emergency funds in a high-yield savings account or money market account that’s separate from your everyday checking account. Look for FDIC insurance protection, easy access within 1-2 business days, and competitive interest rates (4-5% in 2026). Avoid investing emergency funds in stocks or locking them in CDs where you can’t access them quickly.[2]

Should I save for emergencies or pay off debt first?

Build a $1,000 starter emergency fund first, then focus on paying off high-interest debt (credit cards, payday loans). Once high-interest debt is cleared, expand your emergency fund to the full 3-6 months while making minimum payments on low-interest debt like mortgages or student loans.[1]

What counts as a real emergency?

True emergencies are unexpected, necessary, and urgent expenses like medical bills, essential car repairs, emergency home repairs, or job loss. Regular expenses you forgot to budget for (car registration, holiday gifts, annual insurance premiums) aren’t emergencies—they’re irregular expenses that should have their own budget category.[4]

How do I start a budget when I’m living paycheck to paycheck?

Start by tracking actual spending for one month without judgment. Then identify one or two expenses to reduce (subscriptions, dining out, or switching to generic brands) and redirect that money to a starter emergency fund. Even $25 per paycheck creates momentum. Focus on small wins rather than perfect budgets. See this guide on stopping the paycheck-to-paycheck cycle.

What if my spouse and I disagree about budget priorities?

Schedule a monthly money meeting where both partners have equal input. Start by agreeing on shared goals (emergency fund, debt payoff, retirement), then allocate “fun money” for each person to spend without judgment. The key is making the budget together rather than one person imposing it on the other. Consider this couples budgeting approach for specific strategies.

How often should I review my budget?

Review spending versus budget monthly to catch problems early and make adjustments. Do a comprehensive budget overhaul quarterly or whenever major life changes occur (job change, new baby, move, income increase or decrease). The monthly review takes 30 minutes; the quarterly review might take 1-2 hours.[4]

Can I still have fun on a budget?

Absolutely. The 50/30/20 framework specifically allocates 30% of income to wants, which includes entertainment, dining out, hobbies, and other enjoyable activities. The goal is conscious spending on things you truly value rather than mindless spending on things that don’t matter to you.[6]

What’s the best budgeting app or tool?

The best tool is the one you’ll actually use consistently. Options range from simple spreadsheets to apps like YNAB, EveryDollar, Mint, or PocketGuard. Start simple—even a notebook works. You can always upgrade to more sophisticated tools once the habit is established. Many families find that simple budgeting methods work better than complex systems.

How do I budget with irregular income?

Build your budget on your lowest typical monthly income from the past year. When higher-income months arrive, allocate surplus to emergency fund, debt payoff, and irregular expense categories. Keep a larger emergency fund (6-12 months) since your income varies. Consider using the half-payment method to smooth out income fluctuations.

What if an emergency exceeds my emergency fund?

First, use all available emergency fund money. Then explore options in this order: payment plans with the provider (often 0% interest for medical or repair bills), 0% intro APR credit cards paid off within the promotional period, low-interest personal loans, or as a last resort, home equity lines of credit. Avoid payday loans or high-interest options. After the crisis, rebuild your emergency fund before resuming other financial goals.

How do I explain budgeting to my kids?

Use age-appropriate approaches: give young children three jars labeled “spending,” “saving,” and “giving” for allowance; let older kids help with grocery shopping and price comparisons; involve teenagers in family budget discussions about priorities and trade-offs. The goal is teaching that money is finite and choices have consequences, not creating anxiety about finances.

Key Takeaways

- Build emergency resilience in layers: Start with a $1,000 starter fund, expand to 3-6 months of essential expenses, then add specialized reserves for medical deductibles or home repairs based on your situation

- Use the 50/30/20 framework as your foundation: Allocate 50% to needs, 30% to wants, and 20% to savings and debt repayment, adjusting percentages as needed for your specific circumstances

- Base your budget on reality, not wishes: Track actual spending for three months before creating your budget, then build categories around real spending patterns rather than idealized estimates

- Automate savings to remove willpower from the equation: Set up automatic transfers to your emergency fund and other savings goals on payday, saving first and spending second rather than hoping money is left at month’s end

- Separate irregular expenses from true emergencies: Create a dedicated budget category for predictable-but-annual costs like holiday shopping, car registration, and home maintenance so these don’t derail your plan

- Review and adjust monthly without judgment: Schedule a 30-minute money meeting each month to compare actual spending to your budget, celebrate wins, and adjust categories based on real data

- Test your budget against common scenarios: Walk through job loss, medical expenses, car repairs, and home emergencies before they happen to identify gaps and build appropriate reserves

- Expect imperfection and plan for it: One overspending week doesn’t mean budget failure—it means you adjust and continue, focusing on progress over perfection

- Protect your emergency fund from non-emergencies: Keep it in a separate account with a 1-2 day transfer time to create friction that prevents casual spending

- Adjust your budget as life changes: Major transitions like having children, job changes, or caring for aging parents require budget resets, not just minor tweaks to existing categories

Conclusion

Learning how to create a family budget that survives emergencies isn’t about restricting every dollar or living in deprivation. It’s about building a financial foundation that gives you options when life throws curveballs—and life always throws curveballs.

The families who weather emergencies without financial crisis aren’t necessarily the ones earning the most money. They’re the ones who built emergency funds layer by layer, tracked spending honestly, automated their savings, and reviewed their budgets monthly. They treated budgeting as a flexible tool rather than a rigid rulebook.

Your emergency-proof budget starts with small, manageable steps: track your spending for one month, build a $1,000 starter fund, set up one automatic transfer, and schedule your first monthly review. You don’t need to perfect everything before you begin.

Your next steps:

- This week: Pull three months of bank and credit card statements and categorize your actual spending

- This month: Create your first budget using the 50/30/20 framework as a starting point, adjusting percentages to fit your reality

- By next month: Set up automatic transfers to a separate savings account for your emergency fund, starting with whatever amount fits your budget

- Ongoing: Schedule monthly 30-minute budget reviews on your calendar and actually do them

The budget you create today won’t be perfect, and that’s okay. It will evolve as you learn what works for your family, as your income changes, and as life circumstances shift. The goal isn’t perfection—it’s progress toward financial stability that lets you handle emergencies without panic.

Start building your emergency-proof budget today. Future you, facing an unexpected $1,500 car repair or a temporary job loss, will be incredibly grateful you did.

For more practical money management strategies, explore these frugal living tips and money-saving techniques that complement your new budgeting skills.

References

[1] Family Financial Wellness Guide – https://getsqwire.com/family-financial-wellness-guide/

[2] How To Build An Emergency Fund In 2026 A Step By Step Guide – https://useorigin.com/resources/blog/how-to-build-an-emergency-fund-in-2026-a-step-by-step-guide

[3] Do This Not That Plan Your 2026 Finances With Ease – https://www.greylock.org/post/do_this_not_that_plan_your_2026_finances_with_ease.html?psrc=1459

[4] How To Create A 2026 Household Budget That Actually Sticks – https://www.naccacpas.com/blog/how-to-create-a-2026-household-budget-that-actually-sticks

[5] Yes You Need An Emergency Fund Heres How To Start In 2022 Even If Youre Still Feeling Behind – https://hermoney.com/invest/financial-planning/yes-you-need-an-emergency-fund-heres-how-to-start-in-2022-even-if-youre-still-feeling-behind/

[6] Budgeting And Saving For 2026 A Smart Start To The New Year – https://www.wedbush.com/budgeting-and-saving-for-2026-a-smart-start-to-the-new-year/