I’ll never forget the sinking feeling I had when I realized I’d spent $347 on food delivery apps in a single month. That’s more than my car insurance payment! As I sat there staring at my bank statement in 2026, I knew something had to change. The truth is, most of us are hemorrhaging money through completely avoidable mistakes—and we don’t even realize it until the damage is done. Understanding the money mistakes to avoid isn’t just about penny-pinching; it’s about building a life where your money works for you instead of disappearing into thin air.

Key Takeaways

- Most financial mistakes stem from psychological triggers rather than lack of knowledge—understanding your money mindset is the first step to avoiding costly errors

- Emergency funds and proper budgeting are non-negotiable foundations that prevent 80% of common financial crises

- Small daily money mistakes compound dramatically over time—eliminating just 3-5 bad habits can save you $5,000-$10,000 annually

- Technology and social media significantly influence modern spending patterns, making awareness of digital triggers essential

- Recovery from financial mistakes is always possible with the right strategy, accountability, and consistent action

Understanding the Psychology Behind Money Mistakes to Avoid

Before we dive into the specific mistakes, let’s talk about why we make them in the first place. According to behavioral economics research, our brains are wired with cognitive biases that actively work against smart financial decision-making[1].

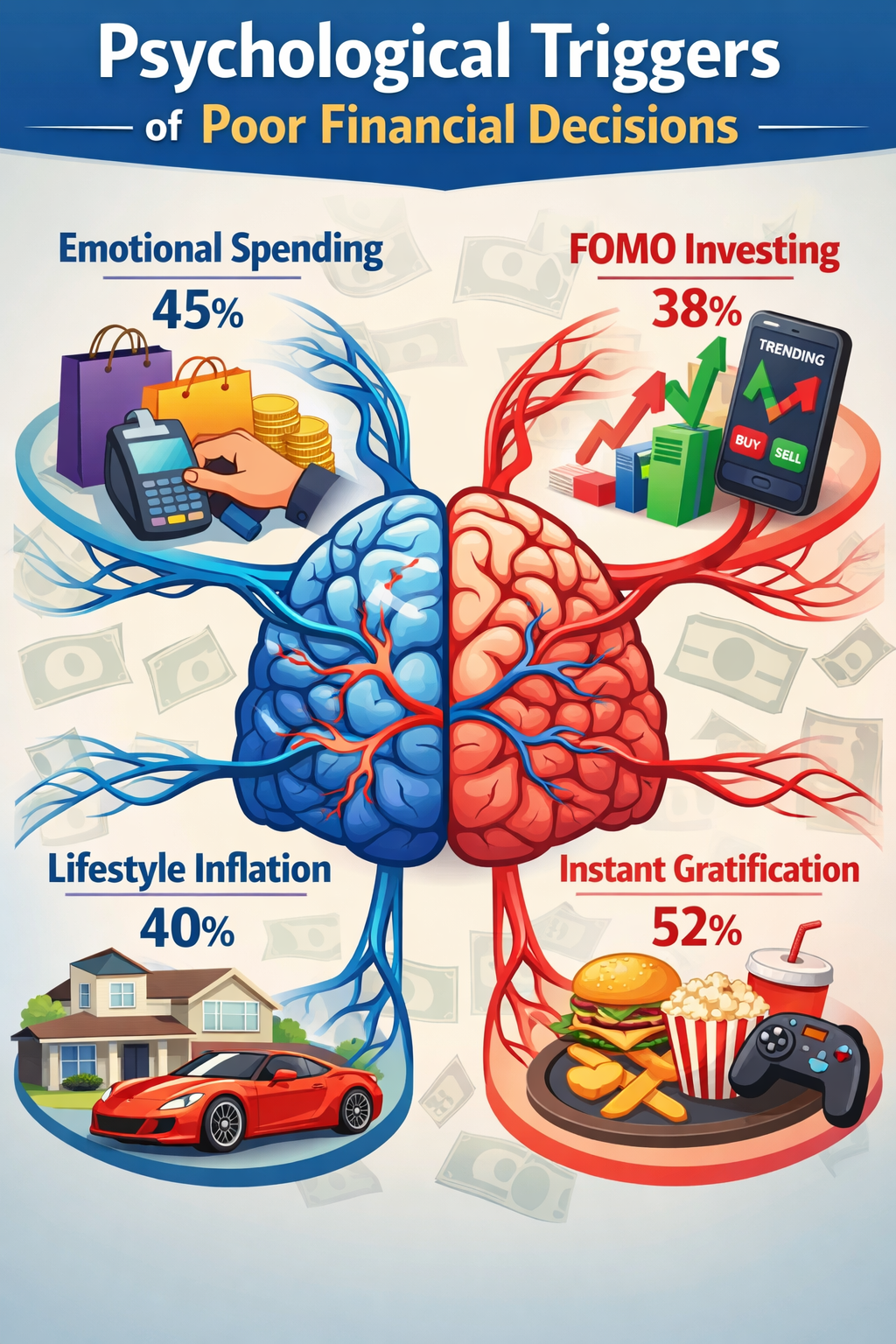

The Emotional Money Brain

Our financial choices are rarely purely logical. In fact, studies show that emotional factors drive up to 80% of our purchasing decisions[2]. When we’re stressed, we shop. When we’re celebrating, we splurge. When we’re bored, we scroll through online stores.

I’ve experienced this firsthand. After a particularly tough week at work, I found myself “treating” myself to things I didn’t need—a new gadget here, fancy coffee there. These emotional spending triggers were costing me hundreds of dollars monthly without providing any lasting satisfaction.

The four primary psychological triggers that lead to money mistakes:

- Instant Gratification Bias – We value immediate rewards over future benefits

- Social Comparison – Keeping up with peers drives unnecessary spending

- Loss Aversion – Fear of missing out leads to impulsive decisions

- Mental Accounting – We treat money differently based on arbitrary categories

Understanding these triggers is crucial because awareness is the first step toward change. When you can identify why you’re reaching for your wallet, you can pause and make a more intentional choice.

The 15 Critical Money Mistakes to Avoid in 2026

Let’s get into the specific mistakes that are draining your bank account—and more importantly, how to fix them.

1. Not Having a Written Budget 📊

This is the granddaddy of all financial mistakes. According to a 2025 survey, only 32% of Americans maintain a detailed monthly budget[3]. Without a budget, you’re essentially driving blindfolded.

Why it matters: A budget isn’t about restriction—it’s about permission. It tells your money where to go instead of wondering where it went.

The fix: Start with a simple framework like the 50/30/20 budget rule or try the 70/20/10 method. The key is finding a system that works for your lifestyle. I personally use a combination approach, and you can learn more about avoiding common budgeting mistakes to set yourself up for success.

2. Living Without an Emergency Fund 🚨

Here’s a sobering statistic: 60% of Americans couldn’t cover a $1,000 emergency without going into debt[4]. This single mistake creates a domino effect of financial problems.

The consequence: Without emergency savings, every unexpected expense becomes a crisis. Your car breaks down? Credit card. Medical bill? Credit card. Job loss? Financial disaster.

The solution: Start small. Even $500 can break the paycheck-to-paycheck cycle. Then work toward 3-6 months of expenses. Use automatic transfers to make saving effortless—I set up a weekly $50 transfer that I barely notice, but it adds up to $2,600 annually.

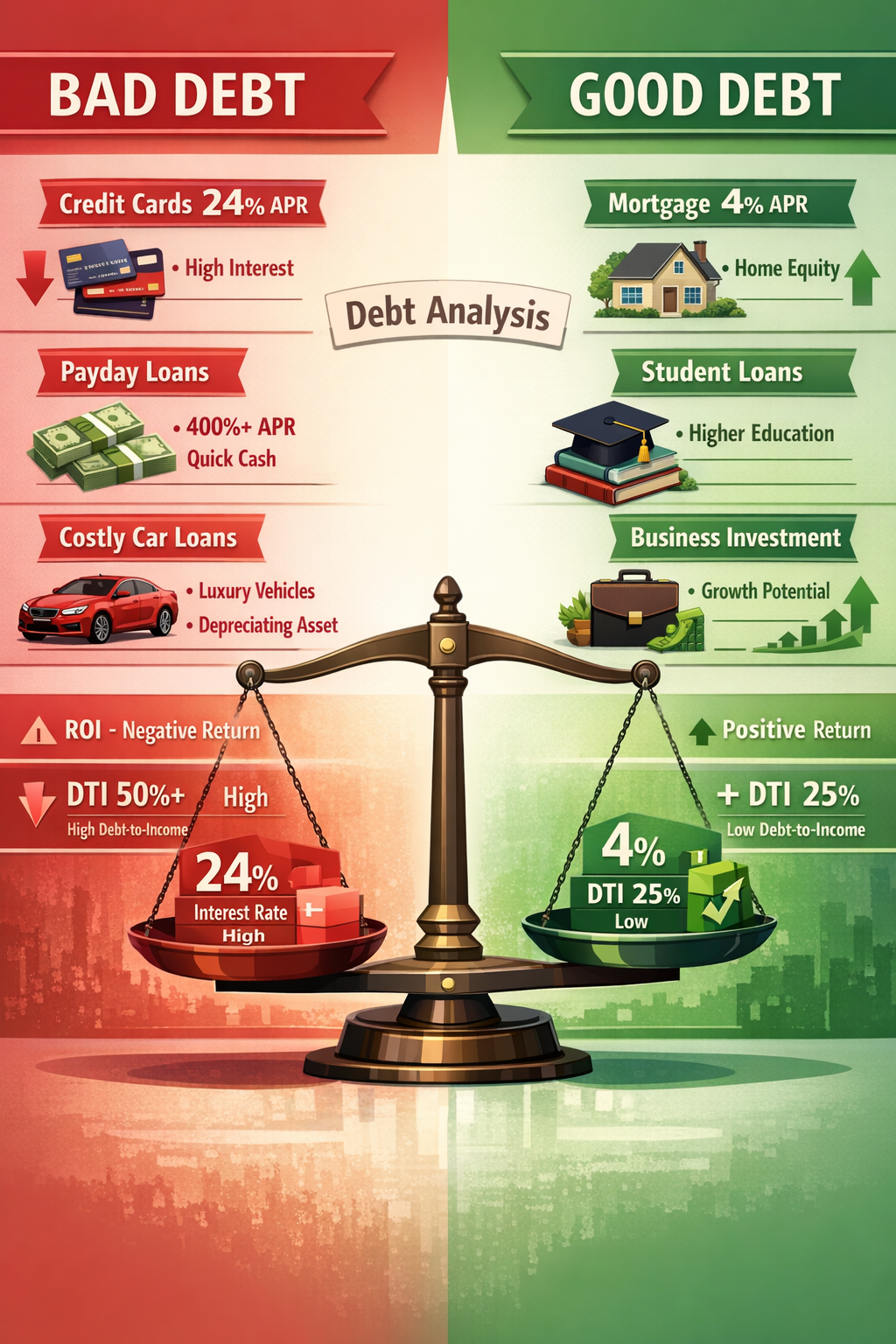

3. Paying Only Minimum Payments on Credit Cards 💳

This mistake costs Americans billions in unnecessary interest annually. If you have a $5,000 balance at 18% APR and only pay minimums, you’ll pay over $4,000 in interest and take 15+ years to pay it off[5].

The trap: Credit card companies design minimum payments to maximize their profit, not your financial health.

The escape plan: Use the debt avalanche or snowball method. Focus on one card at a time while maintaining minimums on others. Check out these proven ways to pay down debt faster for specific strategies that work.

4. Ignoring Your Credit Score 📉

Your credit score impacts everything from loan approvals to insurance rates, yet many people have no idea what theirs is or how to improve it.

The hidden cost: A poor credit score can cost you tens of thousands over your lifetime through higher interest rates. The difference between a 620 and 740 credit score on a $300,000 mortgage? About $65,000 in additional interest[6].

The improvement plan: Check your score regularly (it’s free!), pay bills on time, keep credit utilization below 30%, and avoid closing old accounts. Learn about surprising things that hurt your credit score and discover ways to raise your credit score fast.

5. Lifestyle Inflation 🏠

This is the sneaky killer of wealth-building. As income increases, expenses rise to match—or exceed—the new income level.

The pattern: You get a raise, so you upgrade your apartment, lease a nicer car, and increase your dining budget. Suddenly, you’re making 20% more but saving 0% more.

The antidote: When you get a raise, immediately increase your savings rate by at least 50% of the increase. If you get a $400/month raise, boost your savings by $200 minimum. This allows you to enjoy some lifestyle improvement while still building wealth.

6. Not Tracking Small Expenses ☕

Those daily $5 lattes, $12 lunches, and $3.99 app subscriptions seem harmless individually. But they’re financial termites eating away at your foundation.

The math: $5 daily on coffee = $1,825 annually. Add lunch, subscriptions, and impulse purchases, and you’re easily losing $5,000-$10,000 yearly.

The tracking solution: Use expense tracking apps or a simple spreadsheet. I was shocked to discover I was spending $89/month on subscriptions I barely used. Canceling them felt like giving myself a raise.

7. Emotional and Impulse Spending 🛍️

We’ve all done it—added items to our cart we didn’t plan to buy, purchased something because it was “on sale,” or shopped to cope with emotions.

The trigger: Social media has amplified this problem exponentially. Instagram ads, influencer promotions, and one-click purchasing make impulse spending easier than ever.

The 48-Hour Rule: For any non-essential purchase over $50, wait 48 hours before making a purchase. This simple pause eliminates about 70% of impulse purchases in my experience. You can also try a no-spend challenge to reset your spending habits.

8. Not Investing for Retirement Early 📈

Time is your greatest asset when investing, yet many people delay starting until their 30s or 40s.

The opportunity cost: Someone who invests $200/month from age 25-35 (just 10 years, $24,000 total) and then stops will have more at retirement than someone who invests $200/month from age 35-65 (30 years, $72,000 total), assuming 7% returns[7].

The starting point: Even $50/month makes a difference. Take advantage of employer 401(k) matches (it’s free money!), and consider micro-investing options if traditional investing feels overwhelming. Learn about investing in stocks for beginners to get started.

9. Keeping Up with the Joneses 👥

Social comparison is a wealth killer. When you base your spending on what others have, you’re playing a game you can’t win.

The social media effect: In 2026, we’re constantly bombarded with curated images of others’ “perfect” lives, creating artificial pressure to spend on things we don’t need to impress people we don’t like.

The mindset shift: Remember that most “wealthy-looking” people are actually in debt. True wealth is what you save, not what you show. Focus on your own goals and values, not external validation.

10. Not Having Adequate Insurance 🛡️

Skipping insurance to save money is like removing the airbags from your car to improve gas mileage—the short-term savings aren’t worth the catastrophic risk.

The types you need:

- Health insurance (non-negotiable)

- Disability insurance (protects your income)

- Life insurance (if others depend on you)

- Adequate auto/home insurance

The balance: Don’t over-insure or under-insure. Review policies annually and shop around—I saved $800 yearly by spending 30 minutes comparing insurance quotes.

11. Paying for Unused Subscriptions 📺

The average American pays for 4-5 subscriptions they rarely or never use[8]. These “zombie subscriptions” are pure waste.

The audit: Review your bank statements for the past three months. Identify every recurring charge. Cancel anything you haven’t used in 30 days.

My personal experience: I was paying for a gym membership I hadn’t used in 6 months ($45/month), a streaming service I forgot I had ($14.99/month), and a software subscription I replaced ($9.99/month). That’s $839.88 annually I was throwing away.

12. Not Negotiating Bills and Prices 💬

Most people accept prices as fixed, but nearly everything is negotiable—especially in 2026 when companies are competing hard for customers.

What you can negotiate:

- Cable/internet bills

- Cell phone plans

- Medical bills

- Credit card interest rates

- Salary and raises

The script: “I’ve been a loyal customer for [X years], but this price is stretching my budget. What options do you have to reduce my bill?” This simple question has saved me over $1,200 annually.

13. Mixing Wants and Needs 🎯

This is a fundamental confusion that leads to chronic overspending. We convince ourselves that wants are needs.

The reality check:

- Needs: Food, shelter, basic clothing, transportation, healthcare

- Wants: Restaurant meals, bigger house, designer clothes, new car, entertainment

The practice: Before any purchase, ask: “Will I die, lose my job, or face serious consequences without this?” If not, it’s a want—which doesn’t mean don’t buy it, but be honest about what it is.

14. Not Planning for Irregular Expenses 📅

Car repairs, annual insurance premiums, holiday gifts, and home maintenance are predictable yet often treated as “emergencies.”

The problem: These expenses derail your budget and force you into debt because you didn’t plan for them.

The sinking fund solution: Calculate your annual irregular expenses and divide by 12. Set aside that amount monthly in a separate account. When the expense arrives, you’re prepared. I keep sinking funds for:

- Car maintenance ($100/month)

- Holiday gifts ($150/month)

- Home repairs ($75/month)

- Annual insurance ($125/month)

15. Not Educating Yourself About Personal Finance 📚

Financial literacy isn’t taught in most schools, yet it’s one of the most important life skills. Ignorance in this area costs people hundreds of thousands over their lifetime.

The knowledge gap: Only 57% of Americans are financially literate, according to recent studies[9]. This leads to poor decisions about debt, investing, taxes, and wealth-building.

The education plan: Commit to learning. Read books, listen to podcasts, take courses, and follow reputable financial resources like MSBudget. Even 15 minutes daily of financial education can transform your life.

The Generational Perspective: Money Mistakes Across Ages

Different generations face unique financial challenges and make distinct mistakes based on their life stage and cultural context.

Gen Z (Born 1997-2012)

Primary mistakes:

- FOMO-driven spending on experiences

- Crypto/meme stock gambling

- Underestimating compound interest benefits

- Delaying career investment

Advantage: Time is on their side for wealth-building

Millennials (Born 1981-1996)

Primary mistakes:

- Student loan mismanagement

- Delayed homebuying due to fear

- Lifestyle inflation with career advancement

- Inadequate retirement savings

Challenge: Balancing debt payoff with wealth-building

Gen X (Born 1965-1980)

Primary mistakes:

- Sacrificing retirement for children’s education

- Not maximizing peak earning years

- Carrying too much debt into pre-retirement

- Inadequate catch-up contributions

Focus: Aggressive wealth-building in remaining working years

Baby Boomers (Born 1946-1964)

Primary mistakes:

- Underestimating retirement expenses

- Taking Social Security too early

- Not adjusting investment risk appropriately

- Supporting adult children financially

Priority: Preservation and strategic withdrawal planning

Technology’s Double-Edged Sword: Digital Money Mistakes to Avoid

In 2026, technology has transformed how we manage money—for better and worse.

The Digital Spending Trap

One-click purchasing removes the psychological barrier of handing over cash or even swiping a card. Studies show people spend 12-18% more when using digital payment methods[10].

Social media shopping integrates purchasing directly into entertainment, making it harder to distinguish between browsing and buying.

Subscription creep is easier than ever—signing up takes seconds, but canceling requires effort.

The Technology Solution

Use the same technology to fight back:

- Budgeting apps like YNAB, Mint, or EveryDollar automate tracking

- Automatic savings apps like Digit or Qapital save without thinking

- Bill negotiation services like Trim or Truebill reduce expenses

- Investment apps make wealth-building accessible

I use technology strategically—apps that help me save and invest, while removing apps that tempt me to spend. Consider exploring money-making apps that can supplement your income rather than drain it.

The Mental Health and Money Connection

This is one of the most overlooked aspects of personal finance, yet it’s critically important.

Financial Stress and Mental Health

Financial problems are the #2 cause of stress in America[11]. This stress leads to:

- Anxiety and depression

- Relationship conflicts

- Physical health problems

- Reduced work performance

- Poor decision-making (creating a vicious cycle)

The Holistic Approach

Recognize the connection: Your mental state affects your financial decisions, and your financial situation affects your mental health.

Seek support: Financial stress isn’t a character flaw. Consider:

- Financial therapy or coaching

- Support groups

- Mental health counseling

- Accountability partners

Practice self-compassion: Everyone makes money mistakes. What matters is learning and moving forward, not beating yourself up over past decisions.

I struggled with financial anxiety for years before realizing that addressing both the practical and emotional aspects of money was essential. Developing good financial habits transformed not just my bank account, but my overall well-being.

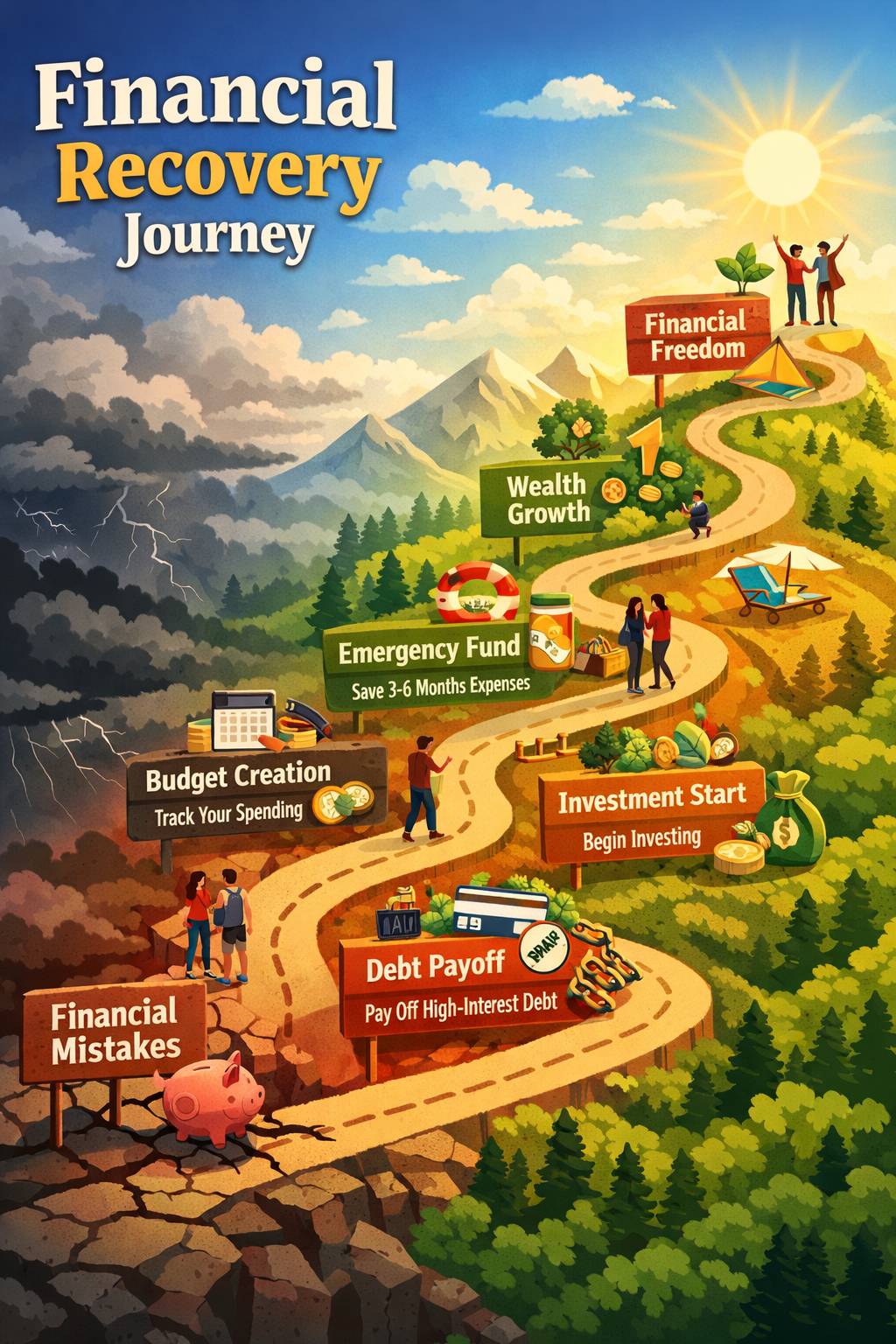

Creating Your Money Mistake Prevention System

Knowing what mistakes to avoid is only half the battle. You need a system to prevent them consistently.

The Three-Layer Defense

Layer 1: Automation

- Automatic bill payments (no late fees)

- Automatic savings transfers (pay yourself first)

- Automatic investment contributions (consistent wealth-building)

Layer 2: Accountability

- Monthly financial reviews

- Accountability partner or group

- Professional guidance when needed

- Regular goal tracking

Layer 3: Education

- Continuous learning about personal finance

- Staying current with financial strategies

- Understanding your own money psychology

- Teaching others (reinforces your knowledge)

The Weekly Money Date

I schedule a 30-minute “money date” every Sunday. During this time, I:

- Review the past week’s spending

- Adjust the upcoming week’s budget

- Check progress toward financial goals

- Celebrate wins and identify areas for improvement

This simple habit has been transformative. It keeps money top-of-mind without becoming obsessive.

Real Recovery Stories: Coming Back from Money Mistakes

The good news? Recovery is always possible. Here are real patterns I’ve seen (and experienced) in financial turnarounds.

Case Study 1: The Debt Avalanche Victory

Starting point: $47,000 in credit card and personal loan debt, minimum payments consuming 40% of income.

The strategy:

- Created strict budget with zero-based approach

- Started side hustle generating $800/month extra

- Applied debt avalanche method (highest interest first)

- Negotiated interest rates down on 3 cards

- Sold unused items for $2,400

Result: Debt-free in 3.5 years, saved $12,000 in interest

Learn how to become debt-free in 12 months or stop living paycheck to paycheck with proven strategies.

Case Study 2: The Emergency Fund Builder

Starting point: Zero savings, living paycheck to paycheck, one emergency away from financial disaster.

The strategy:

- Started with goal of $500 (achievable milestone)

- Cut three unnecessary subscriptions ($68/month)

- Implemented 30-day saving challenge

- Used cash-back apps and credit card rewards strategically

- Automated $25 weekly transfers

Result: $5,000 emergency fund in 14 months, complete peace of mind

Case Study 3: The Late-Start Investor

Starting point: Age 42, zero retirement savings, feeling hopeless about ever retiring.

The strategy:

- Started with just $100/month to employer 401(k)

- Increased contribution by 1% every 6 months

- Took advantage of employer match (instant 50% return)

- Learned about low-cost index funds

- Increased contributions with every raise

Result: $47,000 saved in 5 years, on track for comfortable retirement

Building Wealth: Beyond Avoiding Mistakes

Once you’ve plugged the leaks in your financial boat, it’s time to start sailing toward wealth.

The Wealth-Building Formula

Income – Expenses = Savings → Investments → Wealth

It’s simple but not easy. Here’s how to optimize each component:

Increase Income:

- Develop high-income skills

- Start a side business (check out home businesses you can start with no money)

- Negotiate raises strategically

- Create passive income streams (explore passive income ideas that work in 2026)

Decrease Expenses:

- Apply frugal living principles (see frugal living tips and hacks)

- Eliminate waste without sacrificing quality of life

- Optimize big expenses (housing, transportation, food)

- Practice intentional spending

Maximize Savings:

- Automate everything

- Use sinking funds for irregular expenses

- Build emergency fund to 6-12 months

- Create specific savings goals

Invest Wisely:

- Start early, even with small amounts

- Diversify appropriately

- Keep costs low (index funds)

- Stay consistent through market volatility

- Understand the 7 streams of income

Your 90-Day Money Mistake Elimination Plan

Ready to take action? Here’s your roadmap for the next three months.

Month 1: Foundation and Awareness

Week 1:

- Track every expense (no judgment, just data)

- List all debts with interest rates

- Check your credit score

- Calculate net worth

Week 2:

- Create your first budget using a simple method

- Set up automatic bill payments

- Open a separate savings account

- Cancel one unused subscription

Week 3:

- Identify your top 3 spending triggers

- Create a plan to address each trigger

- Set up automatic savings transfer ($25-100/week)

- Review and optimize one major expense

Week 4:

- Establish your first financial goal

- Find an accountability partner

- Schedule weekly money dates

- Celebrate progress (free or low-cost reward)

Month 2: Optimization and Debt Attack

Week 5-6:

- Implement debt payoff strategy

- Negotiate at least one bill or interest rate

- Increase income by $100-500 (side gig, selling items)

- Build emergency fund to $500

Week 7-8:

- Audit all subscriptions and memberships

- Create sinking funds for irregular expenses

- Learn about investing basics (15 min daily)

- Review and adjust budget based on data

Month 3: Wealth-Building and Habit Formation

Week 9-10:

- Open investment account if you haven’t

- Set up automatic investment contributions

- Increase emergency fund goal to $1,000

- Develop one high-income skill

Week 11-12:

- Review progress and celebrate wins

- Adjust strategies based on what’s working

- Set 6-month and 1-year financial goals

- Commit to ongoing financial education

Common Questions About Money Mistakes to Avoid

Q: What if I’ve already made these mistakes?

Don’t panic. Most people have made multiple money mistakes—I certainly have. What matters is recognizing them and taking corrective action now. Every day is a fresh start financially.

Q: How do I stay motivated when progress feels slow?

Focus on systems, not just outcomes. Celebrate process victories (sticking to your budget for a week) not just results (paying off a debt). Track your progress visually—charts and graphs showing improvement are powerful motivators.

Q: Should I pay off debt or save first?

Both, but prioritize a small emergency fund ($500-1,000) first, then attack high-interest debt aggressively, then build a full emergency fund (3-6 months expenses), then focus on investing. This balanced approach prevents new debt while eliminating existing debt.

Q: What if my partner has different money values?

This is common and requires honest communication. Schedule regular money meetings, focus on shared goals, compromise on methods, and consider working with a financial counselor if conflicts are significant. Money is the #1 cause of relationship stress, so addressing this proactively is crucial.

Q: How much should I have saved by my age?

A common guideline: Have 1x your annual salary saved by 30, 2x by 35, 3x by 40, 6x by 50, and 8x by 60. But don’t let these benchmarks discourage you if you’re behind—focus on your trajectory, not your current position.

The Compound Effect: Small Changes, Massive Results

Here’s the most encouraging truth about avoiding money mistakes: small changes compound dramatically over time.

The $10 Daily Difference

Let’s say you identify and eliminate just $10 in daily waste (unnecessary subscriptions, impulse purchases, expensive convenience foods):

- Monthly savings: $300

- Annual savings: $3,600

- 10-year savings (invested at 7%): $52,397

- 30-year savings (invested at 7%): $367,644

That’s over a third of a million dollars from eliminating just $10 daily in waste. This is the power of compound interest combined with consistent behavior change.

The Three-Mistake Fix

If you fix just three mistakes from this list:

- Create a budget and stick to it

- Build an emergency fund

- Start investing consistently

You’ll be ahead of 70% of Americans financially. That’s not hyperbole—that’s data[12].

Taking the First Step Today

Knowledge without action is just entertainment. Here’s what to do right now:

Your immediate action steps:

- Choose one mistake from this list that resonates most

- Take one small action today to address it (5-10 minutes max)

- Schedule your first weekly money date for this Sunday

- Tell one person about your commitment (accountability)

- Set a reminder to review this article in 30 days

Remember: You don’t need to be perfect. You just need to be better than you were yesterday. Financial transformation isn’t about dramatic overnight changes—it’s about consistent, small improvements that compound over time.

Conclusion: Your Money, Your Future, Your Choice

The money mistakes to avoid that we’ve covered aren’t just abstract concepts—they’re real behaviors that are either building or destroying your financial future right now. Every dollar you spend thoughtlessly is a dollar that can’t work for your future self. Every month you delay starting an emergency fund or investment account is a month of compound interest you’ll never get back.

But here’s the empowering truth: you have complete control over your financial trajectory starting right now. It doesn’t matter if you’re 22 or 52, whether you have $100 or $100,000 in debt, or whether you’ve made every mistake on this list. What matters is the decision you make today.

I’ve been on both sides of this equation. I’ve been the person with maxed-out credit cards, zero savings, and no plan. And I’ve been the person who wakes up without financial anxiety, who has options, who’s building wealth consistently. The difference isn’t intelligence or luck—it’s awareness and consistent action.

The 15 money mistakes we’ve covered are costing the average American hundreds of thousands of dollars over their lifetime. But now you’re armed with the knowledge to avoid them. You understand the psychology behind poor financial decisions. You have practical strategies for each mistake. You have a 90-day action plan to implement.

Your next steps:

- Review this article and identify your top 3 money mistakes

- Implement one change from each category this week

- Share this knowledge with someone who could benefit

- Commit to ongoing financial education through resources like MSBudget

- Check back in 90 days and measure your progress

Remember, becoming financially secure isn’t about deprivation or living a joyless life. It’s about making intentional choices that align with your values and goals. It’s about having the freedom to say yes to what matters and no to what doesn’t. It’s about building a life where money is a tool for creating the future you want, not a source of constant stress.

You’ve got this. Start small, stay consistent, and watch as small changes compound into life-changing results. Your future self will thank you for the decision you make today to stop wasting cash and start building wealth.